Forty per cent seems to be the magic number. For some reason, it’s the percentage that is thrown around most frequently when doom and gloom predictions are reported by the media: it was widely reported during the GFC that Australian property prices could slump by 40%, and that forecast gained traction again this year during the COVID-19 pandemic.

It really picked up steam when the Reserve Bank issued a report modelling potential ‘worst-case scenarios’ and outlined what would happen to Australian households if property prices did plunge. (Spoiler alert: it wasn’t good.)

With CBA foreshadowing a potential 32% plunge back in May, it’s been hard to avoid the doom and gloom reports about our most treasured and highest-value assets: our homes.

Now, more than seven months into the economic impact of the pandemic, many industry experts are winding back their negative predictions. And it’s not just the experts who have growing confi dence in Australia’s economy; consumer confi dence has also increased in recent weeks (see boxout at right).

Why the swift change?

“Most economists are risk averse by nature,” explains property researcher and buyer’s agent Simon Pressley.

“They have a default negative bias, and they always compute the worse scenario. They often have a belief that property markets respond rapidly, because shares can do that, but they fail to understand that property asset values don’t change at all unless there’s a transaction. It’s a big decision and a lengthy process to sell a property asset, whereas a share sale takes one minute. Their beliefs about the biggest infl uences on real estate value are far too simplistic, along with implying that people are homogeneous, that everyone’s income is the same, that everyone’s expenses are the same, and that all properties are the same.”

“Beliefs about the biggest influences on real estate value are far too simplistic, along with implying that people are homogeneous ... and that all properties are the same” Simon Pressley, property researcher and buyer’s agent

Experts widely predicted that COVID-19 would cause a downturn in property prices of between 15% and 40%, and this is because “they responded rapidly to the expectation that overseas migration, or population growth, would be zero and that the national unemployment rate would push past 10%”, Pressley explains.

Simon Pressley, property researcher and buyer’s agent

Simon Pressley, property researcher and buyer’s agent

“They completely underestimated that housing is shelter – it’s the last thing that a person will give up. They didn’t appreciate how incredibly tight the supply side already was and that low interest rates are a form of safety shield. While everyone correctly expected that sales volumes would sink, few appreciated that record-low supply, including resale stock, rental stock and new construction, meant that there didn’t need to be much activity for pressure to still occur,” he says.

“And, as always happens, they didn’t factor in the vastly different economic profiles and growth drivers in each location, particularly capitals and non-capitals. The reality is that property markets aren’t simple at all. There are multiple influencing factors, and it’s the sum of all factors, not one factor, which triggers the action of a dominant critical mass that always dictates market performance for a chosen location.”

Many think that property markets are a simple formula of supply and demand, with ‘supply’ being the volume of extra dwellings constructed over the last year and ‘demand’ being the volume of population growth over the same period.

But property fundamentals and drivers of growth aren’t anywhere near this simplistic, Pressley argues.

“These people haven’t studied Australian real estate history to the nth degree. I have – every location. The only way to truly understand the complexities of property markets is to look at what every location has done over history, what happened in each location to cause the ups and downs, and identify the common denominators,” he says.

“The real estate generalists quickly jump to an often-negative price fluctuation conclusion as soon as there’s a major announcement such as unemployment projection, migration policy change, or building construction change. Instead, people need to draw a more informed conclusion from the sum of all parts of a very big puzzle.”

Raj Sarin, head of investment finance at InSynergy Property Wealth Advisory, agrees with the view that we need to focus on the macroeconomic conditions and fundamentals of each specific market, rather than taking too much of a generalist view.

“As a country, we entered COVID-19 with very strong fundamentals and a great balance sheet. Furthermore, the macro fundamentals of markets like SA, Southeast Queensland, the ACT and WA were strong, and it’s no surprise who will be the winners in the next cycle,” he says.

“As a country, we entered COVID-19 with very strong fundamentals and ... the macro fundamentals of markets like SA, Southeast Queensland, the ACT and WA were strong” Raj Sarin, head of investment nance, InSynergy Property Wealth Advisory

Raj Sarin, head of investment finance, InSynergy Property Wealth Advisory

Raj Sarin, head of investment finance, InSynergy Property Wealth Advisory

“Personally, I wouldn’t invest in Sydney property or Melbourne property as they have the most risk, having just doubled [in value] with terrible net yields and the lowest affordability – and yes, a home is an investment too, possibly your biggest one.”

Sarin says it’s still important to buy the right type of property, as cookie-cutter, investor-grade properties will “likely see poor to no growth”, and they always have lower appeal to owner-occupiers, who really drive the market.

However, he is encouraged by the latest reports and predictions coming out of the major banks, which indicate a more positive outlook.

“Westpac have released their revised forecast for the various capital cities, and unsurprisingly there are no 20–30% drops any more, as some other economists were implying as fiscal policy was deployed,” he says.

“No doomsday, and no 1 October 2020 cliffs to fall off either. That said, investing in property – like any asset class – with or without leverage is not without risk. My strong recommendation is for people to speak to professionals who can help them strategise and minimise the various risks involved.”

So, what exactly has Westpac predicted?

Essentially, the bank has revised its near-term house price forecasts, citing a more substantial boost due to lower interest rates and a milder-than-expected recession as reasons for the adjustment.

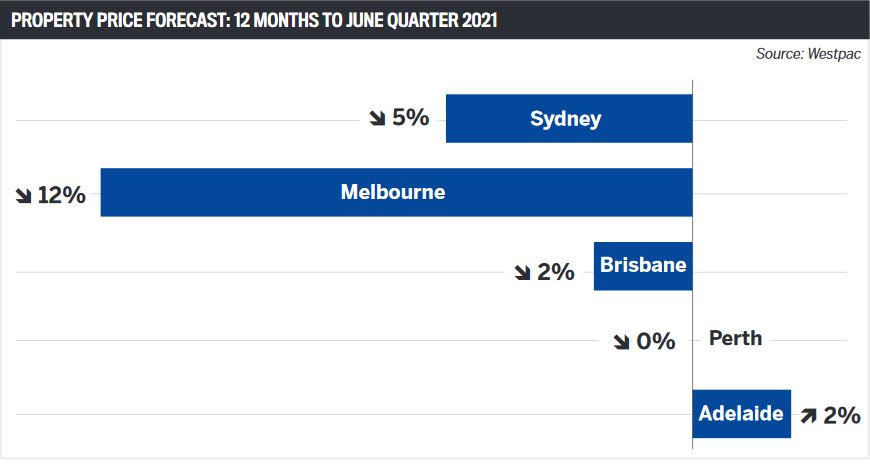

Many may recall that, at the onset of the pandemic, Westpac was one of the first to predict widespread price falls. It forecast a 10% fall in real estate prices nationally from the peak in April to June 2021, with an increase of around 4% per annum over the following two years.

Westpac expected Melbourne prices to be hit the worst, falling by 12%, Sydney values to drop by 10%, and prices in Brisbane and Adelaide to decline by 8%. But now, with national real estate markets appearing to be weathering the COVID-19 storm, the big four bank has dramatically changed its tune.

According to Westpac senior economist Bill Evans, the bank expects a 5% dwelling price correction through to late 2021 – followed by a 15% surge over the next two years.

“To date, our view has been for a 10% fall in prices nationally from the peak in April 2020 through to June next year,” says Evans. “From that point we expected increases of around 4% per annum over the following two years.

“We now expect many capital city markets to be more resilient, with a national fall of 5% between April and June next year, distributed between Melbourne (-12%), Sydney (-5%), Brisbane (-2%), Perth (flat), and Adelaide (2%). Of most importance is that we are much more optimistic about the pace of price appreciation over the following two years, with a total expected increase of around 15%.”

According to Evans, the recovery will be “supported by sustained low rates, which are likely to be even lower than current levels; ongoing support from regulators; substantially improved affordability; sustained fiscal support from both federal and state governments; and a strengthening economic recovery”.

Evans adds that he sees the house price profile unfolding in “four distinct stages”.

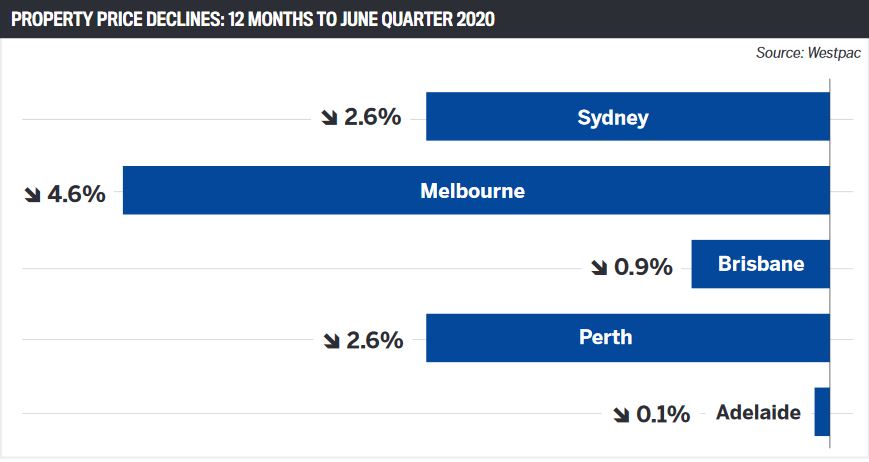

“The first, which has now largely passed, is the initial impact on prices from the collapse in economic activity in the June quarter. That has seen broad-based declines in Sydney (-2.6%), Brisbane (-0.9%), Perth (-2.6%), Adelaide (-0.1%), and a more severe fall in Melbourne (-4.6%). However, the pace of deterioration outside of Melbourne has been milder than we expected back in March,” he says.

“The second stage, which will cover the December and March quarters, will be a period of relatively stable prices, possibly with some modest increases, although Melbourne will be at least one quarter behind the other states and will still be experiencing falls in prices in the December quarter.” According to Evans, the third stage will see some limited resumption of downward pressure on prices through 2021 as we see an increase in ‘urgent’ or distressed sales relating to borrowers struggling or unable to resume mortgage repayments, and “again, more adjustment is likely in Melbourne than the other cities”.

“Australia has dealt with [COVID-19] better than some other countries ... with the length and severity of the lockdown not as strong, which partly explains its stable performance” Michelle Ciesielski, head of residential research – Australia, Knight Frank

“The fourth phase will come once this selling pressure has worked through the system and prices lift again,” he says.

His sentiments are echoed in new research from Knight Frank, which suggests that Australia’s housing market has been among the top performers globally in terms of price growth over the first six months of 2020.

Australia moved up 37 places in the global rankings from last year, claiming the 19th spot in Knight Frank’s Global House Price Index over the second quarter of 2020.

House prices across Australian markets grew by 6.1% over the year to June. It is essential to note, however, that in the first six months of 2020 prices fell by 0.4%.

While annual price growth in Australia fell slightly from the first quarter of the year, it was still higher than the average price gain of 4.7% across 56 other countries and territories tracked in the index over the quarter, says Michelle Ciesielski, head of residential research for Australia at Knight Frank.

“Australia has dealt with the COVID-19 pandemic better than some other countries and territories around the world, with the length and severity of the lockdown not as strong, which partly explains its stable performance,” she says.

Ciesielski said the stable growth across Australia’s housing markets could also be attributed to the conditions prior to the COVID-19 outbreak. Heading into 2020, Australia was already experiencing high demand and low stock levels, and this has continued amid the pandemic as homebuyers remain interested in property while sellers take a wait-and-see approach.

Michelle Ciesielski, head of residential research – Australia, Knight Frank

Michelle Ciesielski, head of residential research – Australia, Knight Frank

In Sydney, for instance, the severe shortage of properties for sale through auctions and private treaty is keeping prices stable, says Shayne Harris, national head of residential research at Knight Frank.

“Whilst in the past eight weeks the difficulties around obtaining finance have seen the number of registered bidders thin out at auction, the clearance rate remains stable, as do prices across the inner and middle rings of metropolitan Sydney,” he says.

Brisbane is also holding up well, Harris says, and the city appears to be recording a quicker-than-expected recovery, particularly due to its tight apartment supply line. It is therefore poised to emerge in a “very good position” for 2021 and beyond, Harris says.

“Coming off an extended period of low price growth,” he adds, “Brisbane’s affordability is the best capital city side by side with Perth in the short to medium term.”