While most mortgage borrowers are managing to pay down their debts, a small but rising minority are experiencing financial stress as they grapple with the pressures of the turbulent economy.

Overall, the Reserve Bank of Australia’s half yearly Financial Stability Review released on Friday showed Australia’s financial system remained strong enough to tackle the challenging economic conditions such as inflation and cost-of-living pressures.

However, borrowers with low incomes, large loans, and low savings are still at higher risk of mortgage stress and arrears.

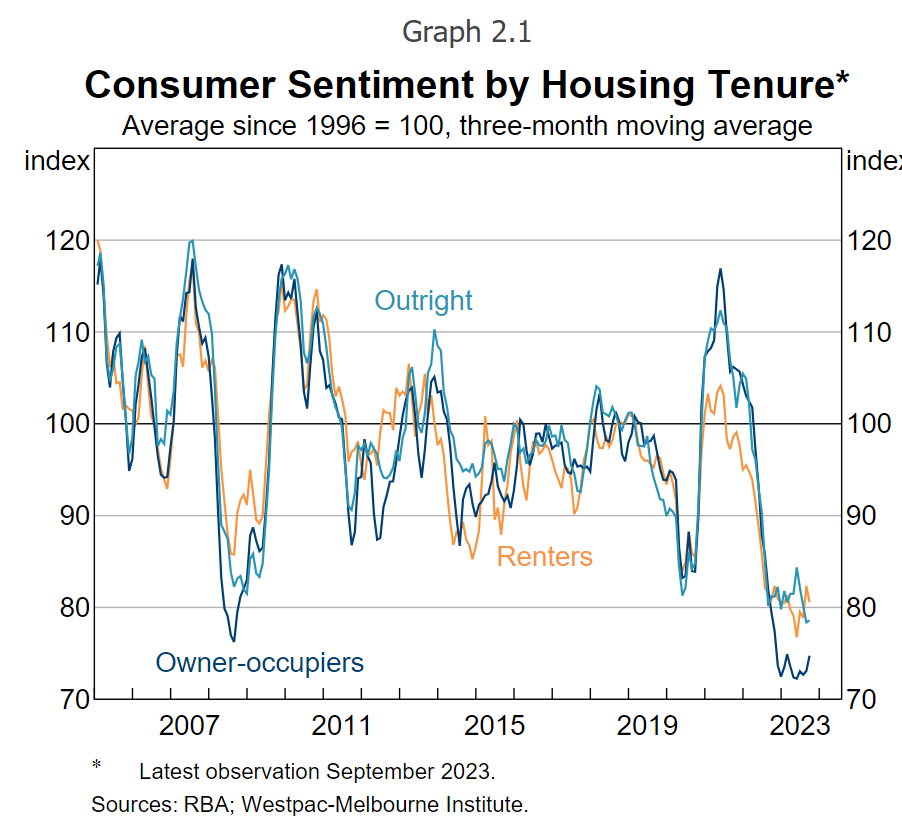

Where Australians once had savings buoyed by the pandemic-era lockdowns and government stimulus, the review indicated higher interest rates and inflation had reduced the spare cash flow of most households.

Many households were adjusting their expenditure, as evidenced by slowing consumption growth and sentiment of their current or future financial health had declined sharply since early 2022.

By using the baseline household expenditure measure (HEM), the RBA found that 5% of Australian homeowners cannot cover essential expenses, up from 1% last year. These households are expected to have little capacity to cut back on spending, the Financial Stability Review found.

However, the number jumps when looked at more broadly through a HEM measure that includes items that are classed as discretionary spending but can be difficult to adjust, such as private health insurance and private school fees.

By this measure, the share of variable-rate owner-occupiers whose expenses and mortgage costs exceeded their income in July 2023 is estimated to be around 13%, up from around 3% in April 2022.

These borrowers, however, are likely to have some capacity to reduce spending over time.

While this may be concerning, these borrowers are not necessarily in mortgage stress yet as they may be dipping into savings or refinancing their loans. There is also little evidence that Australians are turning to credit cards or personal loans to cover their expenses.

Most borrowers are also expected to be well placed in the event of a further increase in interest rates.

The direct effect of a hypothetical 50 basis point increase in the cash rate to 4.6% increases the estimated share of variable-rate owner-occupier borrowers who are unable to cover their expenses (using the baseline HEM) from around 5% to around 7%.

Of these borrowers, about 30% are at risk of depleting their buffers within six months, which is equivalent to 2% of all variable-rate owner-occupier borrowers.

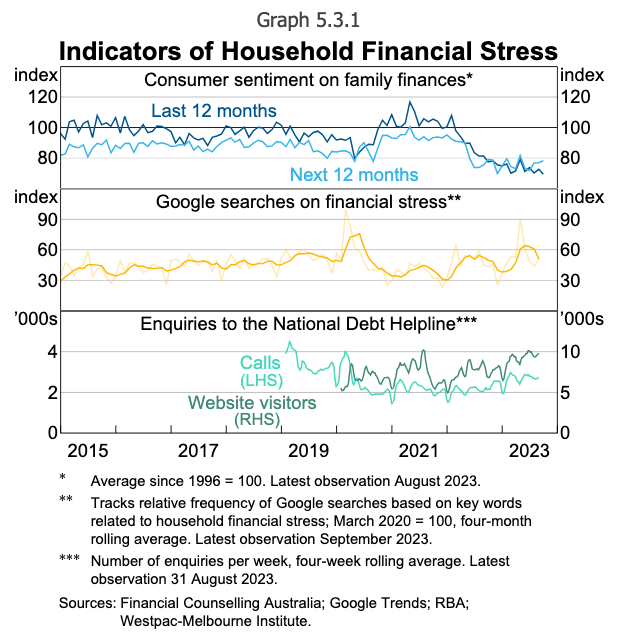

Yet the signs are clear that financial stress has entered the collective minds of Australians, with the frequency of Google searches of terms related to household financial stress increased earlier this year to its highest level since the start of the COVID-19 pandemic in early 2020.

Financial counselling services such as the National Debt Helpline has seen a 28% increase in the number of calls compared to last year, which prompted ASIC to warn lenders about their financial obligations in August.

This is further corroborated by recent research from debtors, which had seen a 60% rise in debt files year-on-year and financial hardship cases jump 25% over the quarter.

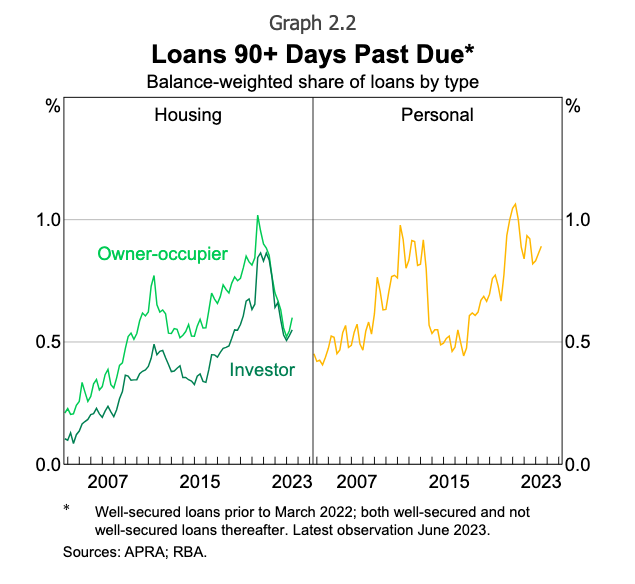

On the other end of the mortgage stress spectrum, personal insolvencies and arrears have remained low despite a recent uptick. Hovering around 0.6% and 0.9% respectively, most households continue to pay their debts.

Lenders have reported that borrowers have been more resilient than expected in their ability to service their debt, given the sharp rise in interest rates. While arrears rates are likely to increase, they are expected to remain very low.

About 1.5% of borrowers are estimated to have their essential expenses and mortgage costs exceed their income and be at high risk of depleting any available buffers.

Even if the unemployment rate were to increase by 2% – around twice as sharply as projected in the by the RBA in August – the share of existing borrowers at risk of running out of buffers over the next year or so would likely remain at low single-digit levels.

Similarly, the RBA said most borrowers would be well placed to service their housing loans if interest rates were to increase further.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.