By

Small business lender Prospa has captured a huge swathe of the SME market, but there are still two million more looking for finance.

If you go for a meeting at the Prospa headquarters, you may get an invitation to convene at the pet shop, the salon or the diner. At the small business lender’s newly renovated space in Sydney, each glass-walled boardroom is named after common small businesses it provides funding to, making each meeting a friendly reminder of who the company serves.

Prospa has been in the online small business lending world for six years now, so while it still looks and feels like a youthful, energetic start-up, it has settled down and established itself in the industry.

“The biggest change for Prospa is we’ve grown up,” says Matt Bauld, general manager of sales and business development.

“We were five or six people with a massive goal to change the way small business lending was done back then, and now we’re 150 people. We run a big organisation.”

Prospa has lent half a billion dollars in loans to 12,000 businesses since it was founded in 2012. Over the past 12 months it has doubled the size of its loan book, and the size of its team has increased from 90 to 150 people.

With a trove of customer data, a savvy online presence and a 5,000-strong intermediary network, Prospa has developed a thorough understanding of the small business market and has used this knowledge and data to better serve clients and the brokers who bring them in.

“We’ve been able to validate decisioning over years now and really understand how we can say yes more often to a small business that’s coming to us looking for a specific cash flow requirement,” Bauld says.

Its intermediary partners, most of whom are brokers, have played a significant part in getting Prospa’s name out there and connecting the small business community to credit.

Before Prospa was established, small business owners could not access capital unless they had an asset to put up as security. They often turned to the ‘Bank of Family’ or mainstream lenders, but the options were limited, Bauld says.

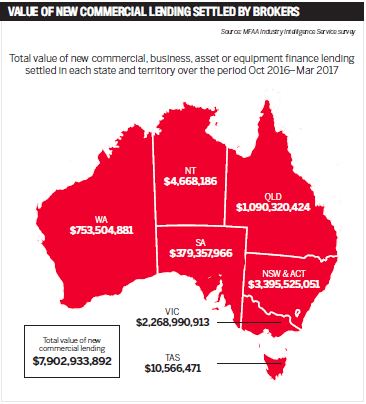

That’s changing as a result of lenders like Prospa, and because more mortgage brokers are feeling comfortable about writing commercial loans for the SME market. According to the MFAA’s latest data, 2,650 brokers wrote a commercial loan between October 2016 and March 2017, an increase of 11.5% from the six months prior.

That’s changing as a result of lenders like Prospa, and because more mortgage brokers are feeling comfortable about writing commercial loans for the SME market. According to the MFAA’s latest data, 2,650 brokers wrote a commercial loan between October 2016 and March 2017, an increase of 11.5% from the six months prior.

But there’s still a huge gap that needs to be filled.

“There are 2.1 million SMEs in Australia. We believe that 40% of those are looking for finance every year,” Bauld says.

“There’s so much to do … the opportunity for brokers is so big that we want to work with them, we want to train them, we want to get them out marketing, making sure they utilise the right tools, that they’re online and realise this opportunity with us,” he says.

Mhairi MacLeod, owner of Astute Ability Finance Group, is one broker who has seized on this opportunity and has educated her SME borrowers about Prospa’s service offering.

“This space is growing rapidly, and there are so many SMEs out there; if they only knew this product was available they could grow and expand,” she says.

What makes Prospa stand out is its staff’s “willingness to think beyond just the standard deal, and their understanding of the SME market, their understanding of small start-up businesses and cash flow”, she says.

Prospa offers business loans of between $5,000 and $250,000, with terms from three to 24 months, and repayments can be made daily or weekly.

It uses a smart proprietary technology platform to assess the health of a business and determine its creditworthiness. It accesses information from various feeds, including banking and transaction data and public social media and review forums, to get a more holistic view of the business. In many cases, this means customers don’t have to submit a single physical piece of data. Applications can therefore take just 10 minutes to complete, and clients can get an approval in as little as 13 seconds, with funding possible within 24 hours.

“And that’s what small business operators want. They don’t want to wait 10 days or a month for a bank to come back and give them a slow no. They want a fast yes,” MacLeod says.

Making it easy

Prospa is committed to nurturing and growing its intermediary partner channel. After all, 75% of its loans are originated by them.

“We want to build our brand, but our channel business always supersedes our direct aspirations,” Bauld says.

Prospa’s done this by establishing strong relationships with aggregators like AFG, Connective, Finsure, eChoice and LoanKit, among others, and has a new aggregator partnership in the works.

After working with a pilot group of about 25 brokers, Prospa launched a new version of its loan portal incorporating their feedback, which now tracks conversion rates and shows the progress of every transaction from end to end, keeping brokers in the loop.

Bauld says he has a team of 22 people on the ground across the country who are dedicated to helping brokers retain and service their small business customers. This includes a team of four people who are solely responsible for onboarding new brokers and setting them up for success.

“We’re about making broker firms more sustainable, and we’re really passionate about that,” Bauld says.

Prospa provides partners with a lead capture tool that they can embed on their websites to capture enquiries from any business owners who may be surfing for funding opportunities at midnight – a common practice among time-poor business operators, Bauld says.

It also offers partners a suite of marketing strategies and material, including web banners and EDM articles that they can use to educate and inform their customers.

Prospa’s support structures and robust set of tools seem to be working. In the last financial year, 400 specialist mortgage brokers were able to diversify by completing and monetising a commercial SME loan with Prospa, Bauld says.

As he points out, brokers are in a unique position to talk to SMEs about Prospa’s products.

“They can relate to the product based on the fact that they are a small business, which makes it easier for them to go, ‘There is a real opportunity. I have it; I’ve seen it in my business’, and then to be able to at least start and initiate conversations with a customer,” he says.

For Paul Stone, joint CEO of HomeSec Business Finance – a funder of one- to six-month business loans that require real estate security – partnering with Prospa has meant his business can refer clients it can’t help itself to a like-minded company it trusts. Prospa and HomeSec don’t compete for clients; instead they complement one another’s offerings, Stone says.

When a successful bakery business in Ballarat came to Stone with a desperate need for an $80,000 loan that he couldn’t assist with, he referred it to Prospa.

“We gave them the loan scenario and one of their team jumped on it right away,” he says.

“They were very open with every stage of the process. They met the client’s expectations and they got the loan funding to them the very next day. We were super impressed. That single thing really clinched the deal for us. Finally we found a company that works alongside the same principles that we do, and that gives you a ton of confidence.”

Mhairi MacLeod, principal broker, Astute Ability Finance Group ; Paul Stone, joint CEO, HomeSec Business Finance

A tipping point

As a pioneer in the online small business lending space, Prospa has helped raise the profile of fintech, and its broker partners have assisted with this.

“The broker market has helped the evolution of fintech by basically starting to talk to more and more customers about its validation points, where it actually assists the customer and how they can use this new change to their advantage,” Bauld says.

Fintech used to be something of a “scary word” a few years ago, with many banks and large businesses dismissing it, he says.

Now it’s reached a tipping point, with those same companies now scrambling to partner with the latest fintech or create their own.

“I think everyone is embracing it; everyone is trying to work out their play. … Most big businesses, as well as small, are really going, ‘How do I get involved?’” he says.

For brokers, that answer should be easy: just ask Prospa.