.jpg)

By

Bluestone's Royden D'Vaz on the growth in near prime lending

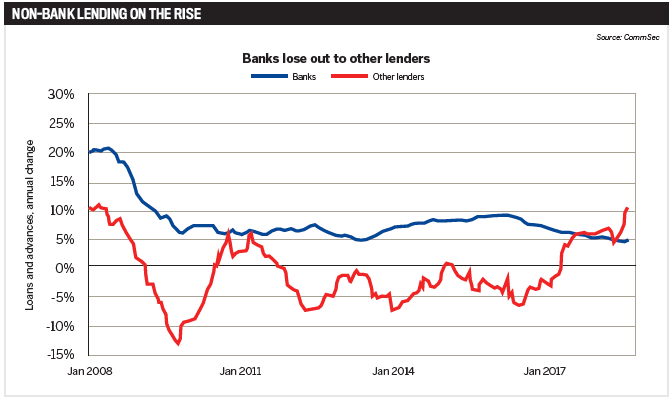

If one trend has defined residential lending in 2018, it’s that more and more applicants have been denied loans by their primary – often big four – bank. According to data from CommSec, first home buyer activity is currently near a six-year high, but overall home loans data shows a year-on-year decline of 6.2%, the largest fall in 15 months (see graph). Further, investor home loans are currently nearing a five-year low.

On the other side of the industry the non-banks are picking up the pieces. Lending to businesses and individuals with low documentation, previous defaults and blemishes in their credit history, the near prime sector is booming.

“Near prime offers these borrowers a flexible and competitively priced alternative,” says Royden D’Vaz, national head of sales and marketing at non-bank lender Bluestone.

In April, Bluestone announced its entry into the near prime residential lending space and in the first three months witnessed a 96% increase in application volume and a 153% increase in settlements in Australia. In terms of market penetration, Bluestone notched up a 55% increase in self-employed loans and a 115% increase in near prime loans for FY2017/18.

“Our introduction of near prime loans came at a time when many mainstream lenders were tightening lending criteria and making it harder for borrowers to access funding. As a result, an increasing number of borrowers were, and still are, struggling to get a new home loan or refinance an existing one,” D’Vaz says.

In addressing the needs of self-employed business owners and PAYG borrowers who are locked out of mainstream banking, Bluestone can help with debt consolidation, funding business expenses, paying ATO debts, buying investment properties, or mortgage refinancing.

By individually assessing each application instead of using credit scorecards, Bluestone builds a broader picture of a client’s ability to meet payments. This allows the lender to accept a wider variety of income sources – bonus and commission payments, most Centrelink pensions – and also meet the borrowing needs of self-employed applicants who don’t have the documentation required by major bank lenders.

“Taken together, these benefits mean that Bluestone is able to offer loans to a much wider variety of people compared to mainstream lenders who automate their assessments with scorecards and disregard the actual circumstances of borrowers,” says D’Vaz, who predicts the growth trend in near prime will continue into next year and beyond.

“The trend of increasing lending in the near prime space will continue as non-bank lenders pick up volume that was previously being written by the banks,” he adds. “As many borrowers who historically borrowed from banks find they can no longer do so, there will be an increased demand for near prime options – something brokers are in a prime position to provide.”

.jpg)

Understanding near prime

Despite the benefits for borrowers, awareness and understanding of near prime lending remains low.

According to D’Vaz, one of the most common misconceptions among brokers is that near prime deals are difficult to package, which he says is “simply not the case”. “It’s a big shame from our perspective, because these brokers are missing out on some really great opportunities,” he says.

To tackle this and other misunderstandings, Bluestone’s BDMs regularly hit the road, visiting brokers to explain how a non-bank specialising in near prime can transform their deals. Supporting the existing team, three new BDMs were appointed in June to serve NSW, Victoria and Queensland.

The credit team also received a boost and there are plans for further growth on the horizon to meet the growing demand for near prime loans. “In our experience brokers are often really surprised at how simple and rewarding it can be to help these customers.

“A lot of the time borrowers come to us after they have been rejected by other banks, and often they’re dealing with significant time pressures to get funding secured before a deadline. We go to great lengths to help them move through the process as smoothly as possible,” D’Vaz says.

Once the application is lodged, brokers have direct access to the Bluestone credit team and can directly coordinate in case of missing documents, additional details and other requirements cutting down the time between lodgement and approval.

Rate reduction

The benefits don’t end there. In March, Bluestone cut its interest rates by 75–105 basis points across the Crystal Blue product suite, which includes a range of full- and alt-doc products that provide lending solutions to established self-employed borrowers with greater than 24 months’ trading history, and PAYG borrowers with a clear credit history.

To mark the move into near prime, in April rates were cut again, this time by up to 225 basis points across the entire product suite.

“By cutting our rates we were instantly able to offer solutions to millions more Australians who can’t quite meet big bank criteria but don’t really fit the specialist profile either. It was a win-win decision for everyone at the table – the company, our brokers, and their customers,” D’Vaz explains.

The cuts followed the acquisition of Bluestone APAC by Cerberus Capital Management.

“The new funding we were able to access through this deal allowed us to pursue opportunities that would have been impossible before, and moving from specialist lending into near prime was an obvious strategic choice,” he says.

The news doesn’t end there as D’Vaz says the emphasis for Bluestone will remain on optimising systems and processes with a focus on supporting brokers.

Hinting at what could be on the horizon for 2019, D’Vaz says, “We’re also exploring several options for expanding our product offering to include more financing solutions for individuals and small businesses. We’re not quite ready to talk specifics, but I’m confident that our brokers will welcome what we have in store for 2019 with wide open arms.”