.jpg)

By

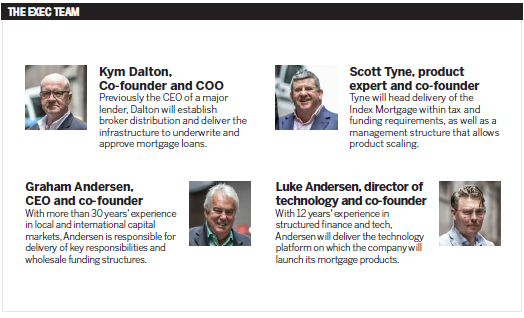

Kym Dalton, COO of Australian Mortgage Marketplace explains how the lender will shake up borrowing, funding and rates

The year is 1992. Securitisation is the new financing mechanism on the block and the banks are riding the wave, generating super profits on home loans. Seeing an opportunity to change how things are done, a non-bank sector emerges and quickly gains pace by challenging the incumbents with promises of better rates and better customer service.

What ensued from there has brought the market full circle. This year, the royal commission revealed that unethical conduct and a customer-comes-last attitude remains among the major bank lenders. While it could be said that history is repeating itself, this time one challenger has a tech-savvy edge.

“Incumbent lenders have been treating customers poorly, whilst marginally meeting the requirements of responsible lending conduct. Right now, the market is broken. Existing lenders have breached the covenant of trust,” says Kym Dalton, COO of Australian Mortgage Marketplace.

“We recognise there is an opportunity here and we plan to overhaul the mortgage market by taking advantage of the latest technology available.”

Along with a cohort of fellow industry veterans (see box), Dalton has established a 100% wholesale, broker-focused neo-lender with a remit to shake up the way loans are assessed, originated and funded.

Personalised mortgages

Launching in March 2019, Australian Mortgage Marketplace will be the first lender to offer rapid approvals on a truly personalised mortgage product tailored to the individual’s objectives and credit score.

There will not just be one standard loan on offer; instead an Intelligent Credit Engine will take into account more than 100 data points, then design an exact profile for the borrower and price the mortgage accordingly, using complex mortgage funding data and proprietary algorithms.

“Current lending credit assessment procedures are antiquated, resulting in a lack of consistency and lengthy times to approval. Products and procedures have not kept pace with fundamental changes to Australia’s work and life patterns, nor have the opportunities presented by advances in technology been embraced,” says Dalton.

For couples and joint investors, the individual credit profiles will be merged to create a single rate. This approach to detailed profiling means better rates and products for everyone. Even complex applications from the self-employed can be quickly assessed to meet prime criteria.

“We are living in an age where we can obtain borrower information rapidly and then use that information to customise and tailor an outcome more suitable to the borrower. What we are doing is revolutionary,” Dalton says.

The Intelligent Credit Engine is a future-proofed tool developed by the lender in-house and designed for use by brokers under their own branding. The broker will input customer information – most of which can be preloaded through their CRM – while behind the scenes the borrower’s situation, including income, expenses and credit profile, will be electronically verified to confirm they are a prime candidate.

This “scientific, risk-based pricing”, as Dalton describes it, delivers personalised interest rates and genuine approval, which the firm promises will carry more weight than the standard pre-approval.

As comprehensive credit reporting is rolled out, naturally the Intelligent Credit Engine and its benefits will multiply, Dalton says.

“Our Intelligent Credit Engine takes a holistic view of home loan applications, assessing scenarios on merit, rather than against broad eligibility rules. The credit-decision algorithms process applicant information, verified by third party sources, to provide immediate feedback to the broker and customer,” he explains.

The final piece of the puzzle is demonstrating a customer’s financial literacy regarding the loan they are entering into. “We’ve designed a new approach that explains the specific loan and its terms to the borrower, rather than providing generic information, and then we confirm the customer is entering into the loan in a responsible manner,” says Dalton.

.jpg)

Making a change

The revolution doesn’t end there. Historically, securitisation is opaque and analogue: it is dependent on spreadsheets and – as happened in the last decade – it has the potential to upend entire economies.

“Securitisation really hasn’t changed in structural style or format since 1992, so on the funding side there has been very little innovation in the way RMBS are made and sold. We are determined to change that as well,” Dalton says.

This will happen through the use of distributed ledger technology (DLT) – the tech behind blockchain – to enhance transparency for the superfunds and other institutional investors backing the company. The result is that loans will be funded on what the lender terms Australia’s first mortgage securitisation blockchain.

“Our revolutionary smart securitisation platform, Carbon, leverages DLT to deliver the benefits of increased transparency, security and automation to superannuation funds and institutional investors like nothing the industry has ever seen. Carbon offers operating efficiencies that will create lower-pricing benefits for Australian borrowers.”

However, Dalton is keen to explain that the implementation of DLT does Daltonnot make Australian Mortgage Marketplace a fintech – and it certainly doesn’t mean crypto mortgages are about to be added to the product suite. The final proposition is about giving back to the broker network through what Dalton terms an “industry equity participation”.

Funding the next source of capital, brokers have the chance to make a modest investment in the company, capped at $10,000.

“We are giving the broker industry the opportunity to invest in us and be part of the revolution,” Dalton says.

Problem-solving

Australian Mortgage Marketplace has emerged from the culmination of almost 30 years of observing issues in the current financial system: the inefficiencies in funding and customer contact; the credit data points used in lending; and the systems and processes that should remain native.

The next innovation therefore focuses on providing brokers with more information than ever before, through company’s Broker Plus portal.

“More than 53% of Australians seek credit advice from a mortgage broker, and that’s why we will empower brokers to service customers more efficiently using our Broker Plus portal. Australian Mortgage Marketplace is a genuine wholesale lender that won’t compete with a broker for the customer’s relationship,” Dalton says.

The 100% broker distribution model will also see Australian Mortgage Marketplace join forces with select broker groups.

Australian Mortgage Marketplace’s proposition is designed to provide a fix for the existing lack of transparency, consistency and, occasionally, compliance. It also has the potential to cascade throughout the wider financial system, lifting standards and changing how things are done.

“Our team has a history of disrupting mortgage markets, and what we are launching will be extraordinary, and we want the broker industry to join the revolution,” says Dalton.