.png)

Personal bankruptcies increased 6.1% in 2017. Is the trend an anomaly or the start of economic Armageddon?

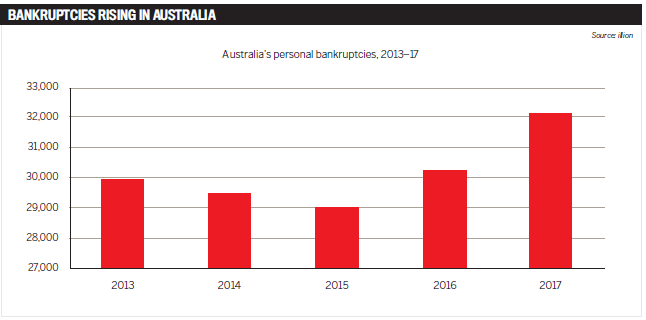

A surge in the cost of everyday essentials, coupled with weak wage growth, caused personal bankruptcies and insolvencies in Australia to rise by 6.1% in 2017, with more than 32,000 cases filed, following a year-on-year increase of 4.7% in 2016. It’s the highest rate in five years.

Not only is the rate of bankruptcy growing, but those filing for it are getting younger, with an average age of 40.9 years compared to 46.7 as recently as 2013. What’s more, representing a 57.4% share of all cases, men are more likely to go bankrupt than women.

“Consumer debt levels are rising steadily in Australia as a result of record mortgages and a surge in everyday essentials such as utilities, petrol and healthcare. These factors, combined with weak wage growth, are putting pressure on the wallets of Australians,” says Simon Bligh, CEO of illion, which published the research.

Further compounding these issues, many areas have suffered catastrophic natural and environmental disasters, straining government budgets and negatively affecting the local economy, impacting on SMEs as well as consumer confidence.

In 2016, two reports commissioned by the Australian Business Roundtable for Disaster Resilience and Safer Communities concluded the cost of social impacts following a natural disaster was 50% higher than originally calculated.

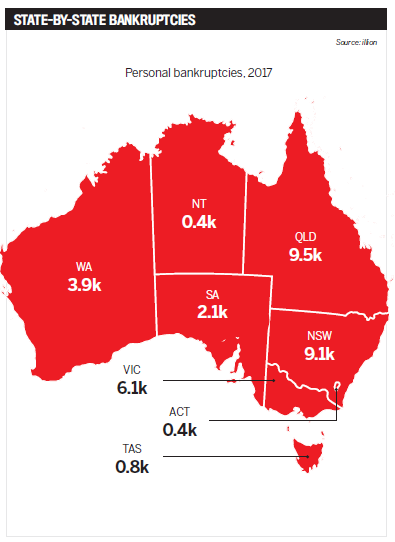

illion’s data shows that the highest concentration of bankruptcies was in Queensland, with 9,454 cases filed over the year. There, Cyclone Debbie severely affected business in the tourism and mining sectors, as well as infrastructure budgets.

The scale of the challenge

From natural disasters to low wage growth, the rising cost of living and failed business ventures, the reasons for filing are complex, and Australians aren’t alone. Other top 20 world economies with rising rates of personal bankruptcy last year included the UK, up 9.4%, and Japan, up 6.4%.

Data published in the September 2017 quarter by the Australian Financial Security Authority (AFSA) demonstrated a rise of 8% in personal insolvencies compared to a year previously, with the number of debt agreements rising to a record high of 3,885, comprising 47.4% of total personal insolvencies. However, bankruptcies increased just 0.1% during this quarter.

“Economies expand and contract at various stages. We have seen slowdowns and recessions but never a meltdown” - Greg Cook, Loan Market

“Economies expand and contract at various stages. We have seen slowdowns and recessions but never a meltdown” - Greg Cook, Loan Market “The rise in personal bankruptcies is concerning and, while no one likes to see these figures trending upwards, we need to keep in mind that they are low compared to the size of the Australian population. Over the last few years there has been phenomenal growth in lending, especially mortgages, which when combined with low wages growth, reduced working hours or loss of employment and the continual rise in the cost of living, there comes a time when something has to give,” says Peter Ellis, founder and borrowers’ advocate at Lending Mate.

A closer look at the AFSA data shows that just 16.1% of debtors declare bankruptcy for business-related reasons, with economic conditions the most cited factor for business-related cases every year since FY2007/8. They are mostly attributable to “a lack of business acumen and a failure to keep proper records”, according to the AFSA.

However, the non-business-related data show a more worrying trend. The primary cause of these insolvencies for the previous two consecutive years is “excessive use of credit”. Despite the wording, that doesn’t necessarily indicate frivolity – four in 10 credit card holders use their plastic to cover groceries and utilities.

Unemployment and loss of income, in addition to domestic discord, complete the top three.

“If we are to better understand the drivers of this rise, then one needs to be able to drill down into the data and see what is causing this to occur. While we do not see much impaired lending – less than 1% – I do see that we drive people to buy now and pay later with long terms of no interest,” says Greg Cook, senior credit adviser, Loan Market.

The rest of the world may have been shocked out of its credit coma in 2008, but Australia has continued to spend, and today the country’s total credit card debt stands at $47bn and counting. Australia has the fourth-highest level of personal debt in the world, and mortgages comprise less than 60% of it.

“Car loans and personal loans are far too easy to get or have special low rates to drive sales. All this credit is designed to drive and fuel personal spending, a factor the RBA keeps mentioning is a driver of the economy,” Cook says.

As recently as November, a statement from the IMF predicted Australia’s low-interest environment would “probably persist for years”, providing stability for the foreseeable future. In February of this year the line changed somewhat, with the IMF advising the RBA to publish US Federal Reserve-style “dot plots” of various probable rate-increase scenarios, to help households prepare before the higher rates hit.

The likely scenario is a 2 percentage point rise within four years, taking the overall rate to 7.1% by 2022. Exactly when the process will begin is still anybody’s guess, with no significant increase in GDP, inflation or wage growth on the horizon.

To some, the current state of personal finances across Australia is the canary in the coal mine – a warning of an impending “economic Armageddon”, as the media has been quick to predict. To others, it’s merely an anomaly.

“A confluence of issues has created a perfect storm for many households. For some this leads to bankruptcy, which is a lagging indicator of financial stress. Our measurement of mortgage stress suggests more pain ahead. So this is not a blip,” says Martin North, principal at Digital Finance Analytics.

While that may be the case within the housing market, economically speaking, some say it’s only part of the story.

“The economy rolls on. It is made up of many moving parts that make up the whole – they are never all doing bad or all doing well at the same time,” Cook says.

As he observes, it’s a fact of life in a free-market economy that a certain level of bankruptcies will occur, but this too fluctuates. He continues: “Granted some [parts] might be slow compared to a previous time – or they may all be sluggish at times – however, economies expand and contract at various stages. We have seen slowdowns and recessions but never a meltdown, and I feel things are too well managed by the regulators, the banks, the RBA and the government to ever see that.”

From left: Peter Ellis, founder and borrowers’ advocate at Lending Mate; Greg Cook, senior credit advise r, Loan Market; Martin North, principal at Digital Finance Analytics

Creative solutions

While Queensland recorded the highest number of bankruptcies by state, the suburb of Berwick in Victoria demonstrated the biggest year-on-year change, with rates rising 121.9% to a total of 71 cases.

The semi-rural suburb of Baldivis, Perth, took the title for highest concentration of personal insolvencies in a single suburb with 103 cases, followed by Victoria’s Pakenham and Craigieburn with 93 and 88 cases respectively. Pimpama, in Queensland filed 88 cases.

The bottom line for brokers is that the typical client profile is changing.

“Clients who find themselves in hard times may in the future need specialist help with finance products. Lending policies are changing, sometimes weekly, and as such brokers are going to have to adapt their businesses and work with clients who don’t fit the box,” says Ellis.

“There has always been a tendency in broking to see these clients as hard to help, too much work and not as quick to settle. But the so-called vanilla-type clients are changing. There has to be more consideration given to the second-tier, non-bank lenders that can accommodate the client’s needs, rather than the majors that seem to get the majority of loans. As the economy changes, gone are the days of everyone fitting nicely into a set criteria.”

How many of these clients exist is still a matter of debate. RBA assistant governor Michele Bullock maintains that financial distress is “not acute at the moment”, playing down the possibility of a further rise in bankruptcies in 2018, and predicting wages and consumer spending will improve in the short to mid term.

In the latest HILDA survey, the median housing debt-to-income ratio stood at 250%; however, the median ratio of mortgage repayments to income during the same period remained stable at around 20%.

On the other hand, data published by Digital Finance Analytics shows that 921,000 Australian households, equivalent to 29.7%, were estimated to be under mortgage stress in December 2017, up from the previous month’s 913,000. Regional analysis confirms that the highest concentration was in NSW, up from 251,576 in November to 258,572 in December.

“What’s ahead depends on future income growth and interest rates. Private sector income growth is below the cost of living and under pressure from rising power costs, childcare and school fees, plus council rates,” North explains.

“Despite low mortgage rates, the average loan size, especially in the eastern states, has grown in line with rising home prices, so debt levels are as high as ever. For those renting, more are finding it difficult to find an affordable place to live.”

What can be said with some certainty is that nothing lasts forever and, as always, failure to prepare is preparation to fail.

North adds, “Future rate rises will hit home and, unless income growth recovers quickly, we will see more financial stress ahead.”