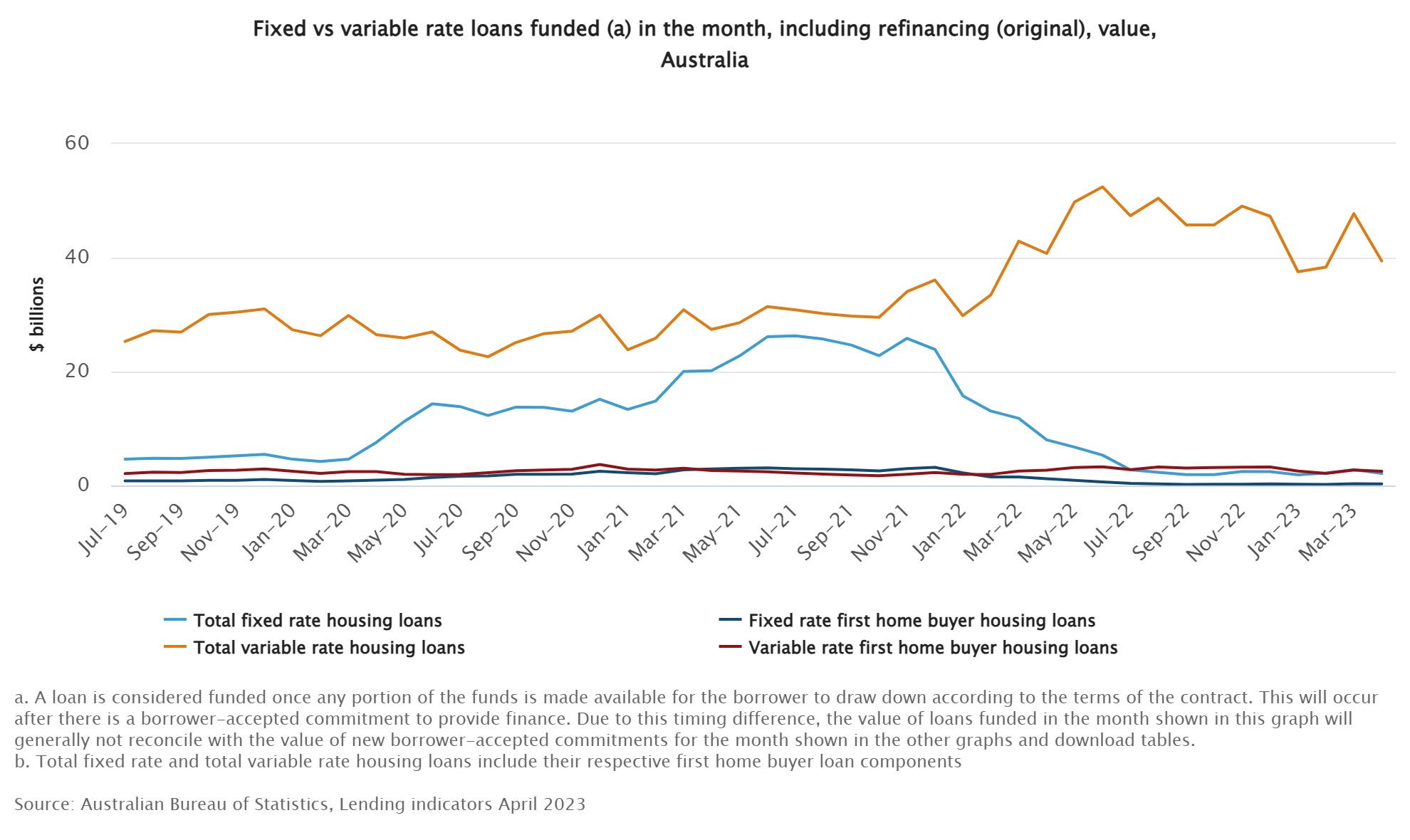

The vast majority of homebuyers are currently choosing variable-rate loans over fixed-rate loans, according to the latest data from the Australian Bureau of Statistics (ABS).

Two brokers shared what they are seeing on the ground floor in both regional and metropolitan Australia.

The data showed that in April, only 5.1% of new and refinanced loans were fixed, while 94.9% were variable.

This is a remarkable difference from the height of the pandemic, when fixed rates climbed as high as 46% in July and August 2021.

Christian Stevens (pictured above left), a Sydney-based senior credit adviser at Shore Financial, said the variable-rate dominance is largely due to them offering more flexibility and potential for when interest rates decrease next year.

“Throughout the pandemic when we saw record low interest rates, many clients were opting for fixed – especially first-home buyers. Now that we are at the peak of the rate cycle, it makes sense that most borrowers are choosing variable,” he said.

Larissa Barton (pictured above right), principal mortgage broker for Mortgage Choice Peregian Beach, agreed saying she is seeing the same thing in regional Queensland.

“We probably fixed about two clients in April out of our entire settlements, and we do fairly significant settlement volume,” she said.

Barton said that some mortgage holders, rolling off low rates fixed during the peak of the pandemic, were still initially considering fixing again but they ultimately nearly always go with the variable option.

“I tell them what the current fix rates are and they come to a grinding halt. There's such a difference between what they were fixed at and what the fix rates are today,” she said.

With the RBA lifting the cash rate in June for the 12th time since May 2022, many economists have forecast that the market is nearing its peak in the coming months.

Stevens agreed, saying based on the current economic indicators it appears that interest rates will remain on hold for the remainder of this year after this, followed by a number of rate cuts in 2024.

“These rate cuts are already priced into the market and should provide households with some relief next year,” he said.

However, Barton is not so sure.

“As a broker, it's very hard to tell our clients exactly what to do other than have the conversation and whether certainty of repayments with fixing the rate is more important to them for peace of mind," she said.

"No one knows with certainty what will happen with rates, and when. One week the media and economists were saying that’s the end of rate rises … two weeks later, the same industry commentators are discussing two more rate increases.”

Barton said that considering the RBA itself once infamously predicted it would not lift the cash rate until 2024, there should be some uncertainty that rates would actually drop. Still, she understands the reasoning behind the swing to variable rates.

“Clients are hoping it's nearly the end. They are thinking, ‘why would I fix my rate the same as my variable rate or a little bit higher even, when we might be at the top of the market? If I fix the two years and rates could drop in 6-12 months, am I going to be left high and dry?”

While nearly all loans in April were variable, there were still around 5% of the market – or $2.39 billion – written for fixed loans.

The question, then, would be why would these borrowers fix in these conditions?

Stevens said the popularity of fixed rates reached parity with variable rates due to the uncertainty caused by the global pandemic.

“Borrowers sought the stability and certainty offered by fixed rates during uncertain economic times,” he said.

Barton said for some borrowers in regional areas where mortgages are not as high, it’s still about stability – where the cost of staying fixed amongst an environment where rates are lowering is outweighed by the benefit of certainty.

“I’ve had some clients who have recently fixed because it was absolutely imperative that they did not have any more rate increases happen to them,” she said.

“I had a young couple that brought up in Gympie. They fixed for three years because they wanted to start a family at some stage in the next 12 to 24 months. For them, it was just about knowing that their home loan would be $500.00 a week for the next three years and that they don't have to think about it.”