A financial adviser has argued that paying lenders mortgage insurance (LMI) can be a strategic move for generating wealth through property investment, but only in specific situations.

Billy Norman (pictured above) from financial advisory firm Link Wealth Group said he had used this strategy a couple of times recently for his property investor clients, however, he admitted it was “only appropriate in certain situations”.

“Paying LMI can sometimes be a wise choice, yet many people struggle to see why,” Norman said.

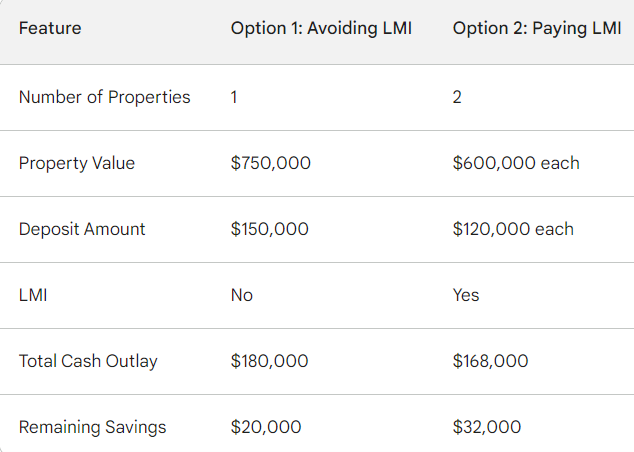

Norman explored this scenario by using the example of Luke, a 43-year-old investor earning $220,000 with $200,000 in savings.

Here’s a clearer breakdown of the key differences:

Of course, this approach has its drawbacks. The LMI, which could total $26,000 for each property, would be added to the loan balance.

Norman said that this approach would also only generally work for clients that had significant savings capacity each month, and who had cash in the bank to fund deposits.

“This is so they can handle debt on multiple properties and have the ability to rebuild their cash buffer relatively fast,” Norman said.

However, given that houses (5.1%) and units (2.7%) have increased year-on-year over the September quarter, according to Domain, the opportunity to have two vehicles for growth rather than one would accelerate portfolio growth if this were to continue.

While 2023 will be remembered for the RBA’s rapid rise in interest rates, there is still keen interest on the property investor front.

The value of new loan commitments for investor housing rose 5.0% to $ 9.5bn and was 12.1% higher compared to a year ago, according to the latest ABS data.

This came after a solid September quarter that saw investor activity carry the lending market.

Norman said most clients were still keen to invest in property, “if they can afford it”.

“I've seen a growing trend towards using a buyer's agent to buy interstate. This is because the outlook for investors in Victoria isn't as favourable as elsewhere in Australia,” Norman said. “Also, the average price in Melbourne is too high for most investors who are seeking existing house and land.”

However, Norman said there were some clients who said they were nervous about the cost of being a landlord, and about property prices, so certainly some people were put off investing in property altogether at the moment.

“Increasingly I'm coming across people who previously invested in property and were put off due to having a bad experience,” he said.

“This is usually because they bought apartments off-the-plan and have not seen any growth.”

Financial advisers and mortgage brokers play distinct but complementary roles in the financial journey of property investors.

Together, Norman said, brokers and advisers could work together to guide clients towards achieving their financial goals through different areas of expertise.

“I will always work with mortgage brokers for clients,” Norman said. “I discourage them from going directly to the bank, as they will get a much better outcome or deal, from a broker who can compare a big range of lenders and select the best option for that particular client.”

“A good broker can also run scenarios and assess borrowing capacity, to give us confidence around the strategy.”

Norman said while financial advisers guided clients' overall investment strategy, brokers navigated the loan application process with banks, ensuring optimal outcomes.

“This is where the broker is critical,” Norman said. “We have a great broker here at Link Wealth Group, his name is Eddie Malaeb. For every new client, I ask if they already deal with a good broker, if they say no, I will always introduce them to Eddie.”

What do you think about Norman’s investment strategy? Comment below