With inflation dipping below expectations in November, talk of rate hikes has evaporated, replaced by speculation about when rates might actually fall.

While one-third (six out of 19) of the panellists in this month's Finder RBA Cash Rate Survey predict a rate cut by August, a key question remains: would such a cut alleviate the current cost-of-living pressures or risk reigniting inflation?

One mortgage expert said the government’s stage 3 tax cuts, due to occur in July this year, may be the answer to avoiding possibly inflationary cash rate cuts while still easing cost-of-living pressures.

In Finder’s survey, where 19 experts and economists weighed in on future cash rate moves and the economy, almost all (89%, 17 out of 19) believed the RBA would hold the cash rate at 4.35% in February.

Graham Cooke (pictured above left), head of consumer research at Finder, said many Australians were in urgent need of reprieve.

“Homeowners are still reeling from 13 rate hikes in the last two years. Our data shows a staggering 40% struggled to pay their mortgage in December,” Cooke said.

While the survey found 40% of experts don’t expect the RBA to start cutting rates until December 2024 or later, one third of them do.

Peter Boehm (pictured above centre) from Pathfinder Consulting was one of these experts, citing inflation, which clocked in at 4.3% for November, as the primary reason for a cut.

“Inflation’s heading in the right direction,” Boehm said. “In Australia, I expect there will be little change [to the cash rate] during the first half of the year (subject to any inflation shocks).”

“By mid-year, we should see rates come down by at least 50 basis points over the second half of 2024, as inflation heads towards the target range.”

If Boehm’s forecast were to eventuate, lower rates would certainly provide some relief for the many borrowers on high variable interest rates who are struggling to pay their mortgages.

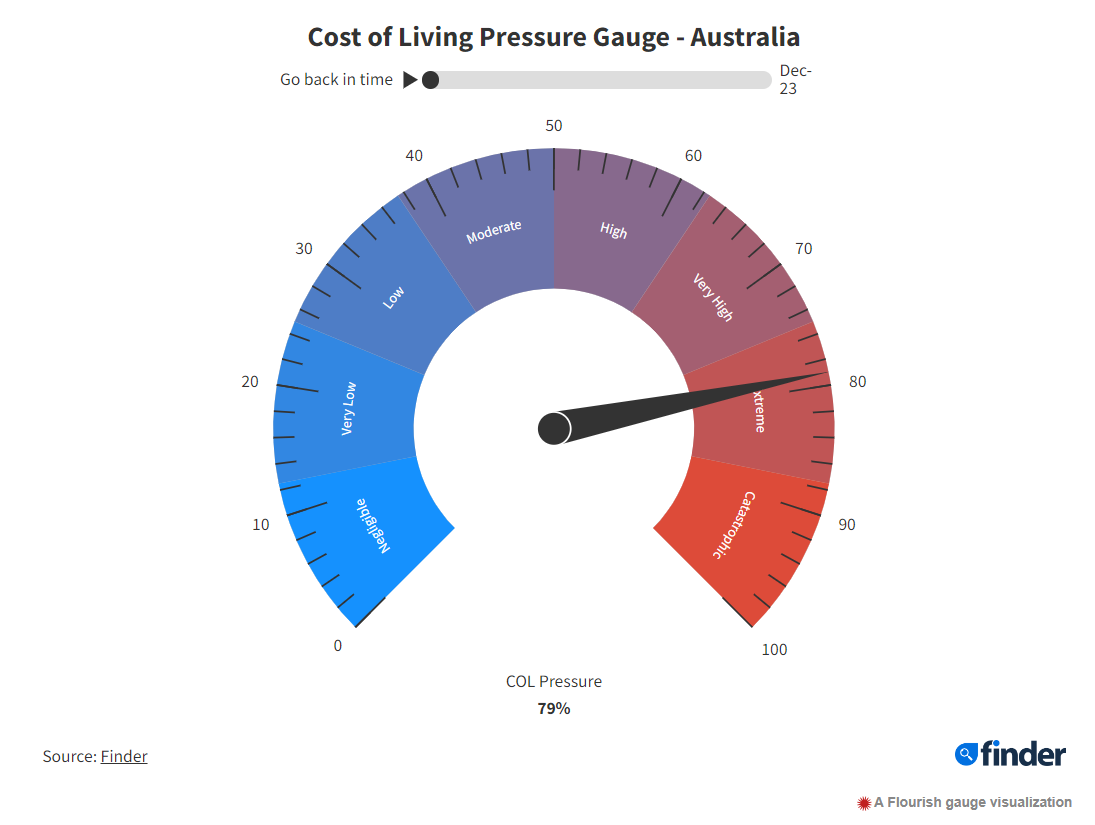

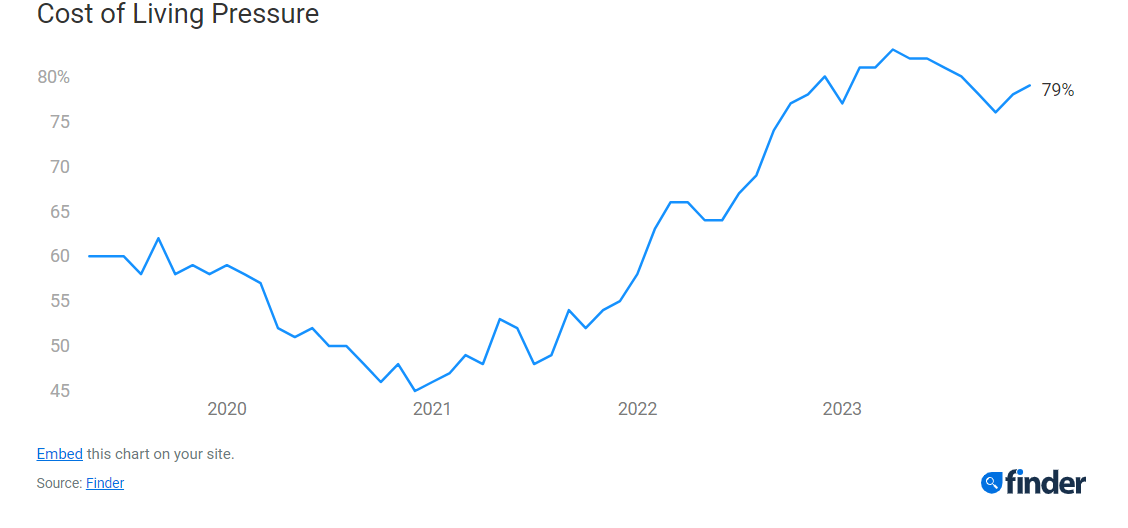

Finder's Cost of Living Pressure Gauge, which blends data from its consumer sentiment tracker and the RBA, revealed a December reading of 79% – an extreme level and a one-point increase from November, indicating continued economic strain on Australian households. For many the situation is dire.

Savings have plummeted by $3,000 in a month, and 78% of Australians feel extremely or somewhat stressed about their finances.

Some 56% of homeowners and 63% of renters report housing costs are causing financial stress, and Australian credit card spending reached a record high at $34.6 billion.

“Any reduction in the cash rate would ease this pressure somewhat and be a very welcome change and beneficial to the Australian consumer,” Cooke said.

However, things are expected to get better – even without slashing rates.

The majority of experts who weighed in (71%, 10 out of 14) expected the cost-of-living crisis to ease eventually in 2024.

“While the gauge remains in the extreme range, it’s likely that this will be where the cost-of-living pressure peaks,” Cooke said. “We expect to see some relief on the horizon, and with a little luck the pressure will reduce slowly over many months.”

While the prospect of an August rate cut might sound sweet to borrowers, some experts such as Todd Sarris (pictured above right), mortgage advisor for Spartan Partners, warned it might be a fleeting fix.

Instead, he suggested the upcoming Stage 3 tax cuts scheduled for July may offer many Australians a similar respite from the cost-of-living crisis without cutting rates.

“Some economists have estimated that the implementation would be equivalent to 0.5% to 0.75% of a rate cut,” Sarris said. “So, it would thus be incredibly touch and go for the RBA to cut rates at the same time that the economy is getting stimulated with Stage 3.”

“The absolute worst RBA outcome (from a credibility perspective) is to undertake yo-yo monetary policy. Reduce interest rates, realise they have re-energised inflation, then raise interest rates back up. There is nothing that kills business and bank confidence more than yo-yo monetary policy.”

Cooke agreed that the RBA “needs to be careful” in ensuring that a cash rate cut doesn’t reverse the downward-trending inflation figures.

“For this reason, we are unlikely to see a cash rate cut any time soon – with most economists pointing to Q4 2024 or even 2025 for the next cut,” Cooke said.

“In reality, a cash rate cut would indicate the economy is turning a corner and we are emerging from the cost-of-living crisis, but its timing is important.”