The borrower demands shaping SME finance and how lenders are are rethinking their core products

While Hamlet mused over whether it is better “to be, or not to be”, Australian SMEs are currently asking whether it is better to bank or not to bank when looking to secure extra cash.

Pressed for time and expertise, most SMEs select their lender based on speed, service and flexibility of terms, rather than price or brand loyalty, and these trends are placing added pressure on all players to rapidly digitise the business lending environment.

“Customers across the board are demanding more personalised, seamless experiences – from the way they watch TV or transfer money to accessing funding,” says Prospa’s EGM of sales and business development, Matt Bauld.

“Small business owners want a fast response and funding, excellent customer experience, and a simple, frictionless application process that doesn’t require property security or a 20-page form.”

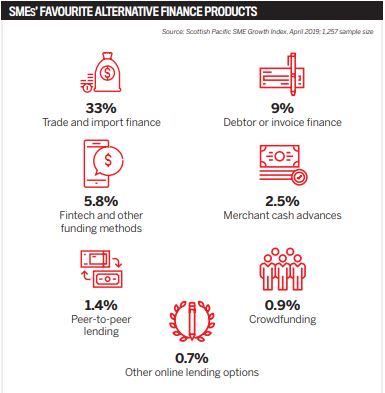

The latest Scottish Pacific SME Growth Index reports that fewer than 20% of SMEs now turn to their primary bank for funding. Further, the index calculates that 96% of SMEs are drawn to alternative lenders mainly because they believe their credit approvals are faster.

A decade ago, a similar trend emerged in the US. There, the rise in non-bank lenders was also driven by the mainstream banks’ inability to provide bespoke solutions to the business sector. The outcome was a proliferation of alternative lenders.

“The industry in Australia has been a fast follower of global best practice, and the willingness of Australia’s SMEs to embrace new technology has made this country an ideal fit for lenders such as us,” says Cameron Poolman, CEO of OnDeck Australia.

“Overlay this onto the indifferent attitude of the banks towards SMEs and it’s clear the alternative finance sector will continue to accelerate.”

Yet despite these clear and quantifiable trends, the mainstream banks continue to see growth in business loans. According to NAB’s latest financial results, business lending increased 5.3% year-on-year – a figure Thomas says is “well ahead” of other majors. Currently, NAB lends around $3bn a month to SMEs.

“Whether you are looking at banks or non-banks, what we are seeing is how much small business values quick and easy access to funds through a digital platform,” says Chris Thomas, GM for commercial broker at NAB.

NAB has seen demand spread across a variety of products, with customers in the commercial space applying for everything from small loans for single proprietors to significant funding lines for larger companies.

After speaking directly to business owners, the bank knows that speed and efficiency are key to its competitive edge, and that is dictating how it innovates this important part of its operations.

“From NAB’s perspective, we are seeing continued growth in the SME space. Over the next decade, we may see SME lending fully digitised,” says Thomas.

Covering the market

While SME owners have in the past been forced to use overdrafts and credit cards to plug funding gaps, today the banks and non-banks have unofficially divided the needs of businesses between them as the market has allowed, rolling out a series of new products in the process to meet almost any need.

For example, in recent months Prospa has increased its maximum loan amount to $300,000; launched the Small Business Loan Express for sums of up to $150,000; and announced a 48-hour turnaround for loans of between $150,000 and $300,000.

It has also introduced a line of credit for between $2,000 and $25,000 and recently joined three new aggregator panels to boost the reach of its products. Last year, NAB launched its QuickBiz for Broker platform, which allows broker SME customers to access funds within a single day, once documents are signed and returned.

Further, the bank has 400 broker-aligned business bankers across the country who are “ready and available” to provide support.

NAB is also working to meet new demand across a number of sectors.

“Business customers aligned to industries like health, professional services, government infrastructure projects and agriculture are all showing upward trends in demand. Meanwhile, retail trade and some aspects of residential property development are reflecting lower demand,” says Thomas.

Specialising in niches where the banks are absent, OnDeck now offers a dedicated Equipment Loan of up to $250,000 when aggregated with its Unsecured Loan. Typical values sit between $50,000 and $100,000, and funding is available within three business days.

“This sweet spot hasn’t happened by chance,” says Poolman.

“A lot of newer players in the market prefer to limit their exposure to loans below $50,000, and of course it isn’t economically viable for the banks to work in this space – certainly when loans are below $100,000.”

According to Poolman, the average SME customer at OnDeck has annual revenue of $1m, and the maximum leverage typically seen is 10% of annualised revenue. “Banks don’t serve this end of the market, or indeed SMEs with annual revenue between $2m and $2.5m,” he explains.

Helping brokers to promote the vast array of products currently on offer, this year the MFAA launched a digital campaign to market broker services to SME owners.

Using LinkedIn, the association is targeting 510,000 business owners, operators and finance professionals throughout April, May and June.

The MFAA then plans to analyse the insights and customer feedback to formulate future campaigns.

“This is an excellent initiative that comes at a good time. There is every reason to expect the share of broker-introduced SME finance to increase significantly from what is a comparatively low base now at less than 20%, and the non-banks will likely see a greater proportional share of that uplift,” says Thinktank CEO Jonathan Street, who notes that non-banks are “genuinely committed” to innovation.

“This in turn will feed more investment by the non-banks in further improving products, range, policy flexibility, pricing and technology. In short, the non-banks will continue to grow in size, capability and importance relative to ADIs,” he adds.

Over the past year, Thinktank has seen commercial and residential SMSF finance for business owners account for around 20% of overall flow. Not only has it been the largest individual product stream but Street reports that it has also been the best performing part of the loan book, with zero arrears or losses to date.

Rising demands

At Bluestone, self-employed borrowers are a core segment of the business, accounting for 61% of all customers.

While Royden D’Vaz, Bluestone’s head of sales and marketing, says the royal commission and housing downturn have certainly made the market tougher for borrowers of all types, the demands of business owners are drastically reshaping how lenders operate.

“In recent years, consumers have started to become increasingly discerning in the service levels they are willing to accept, and with growing technological literacy they are becoming more comfortable in researching and accessing lenders and financial products that are not necessarily available via a branch network,” says D’Vaz.

Last year, Bluestone moved into low-rate near prime lending for self-employed as well as other borrowers.

This increased uptake of the non-bank’s clear credit products by 85% over the year, whereas interest in other products catering to varying levels of credit impairment decreased.

The average loan size sits at around $520,000.

“[Changes have] created a more even playing field for lenders and translate into more competition. This results in a wider range of innovative solutions for more borrowers and, ultimately, in better outcomes for our customers,” D’Vaz says.

Finance is rarely a one-off requirement. Mindful that repeat business is key to their proposition, business lenders are designing their service proposition with client retention at the core.

Thomas explains, “A key trend we are seeing across the board is that many business customers have requirements that go beyond just a single asset or transaction. Therefore, business customers are looking to create strong relationships both with their commercial broker as well as the bank the broker chooses for them.”

Supporting this, NAB provides access to specialist business bankers across a broad range of industries, and brokers benefit from having dedicated relationship and credit teams.

As well as boosting business for Australia’s two million small and mid-sized enterprises, SME lending is good for broker businesses too.

“Diversifying into small business lending is non-negotiable for brokers who want to increase revenue.

Prospa has been helping our partners take this next step for years, providing the tools and resources to spot a prospect using their existing client database and to strengthen those relationships,” says Bauld.

New approach

Political promises and legislative changes have also redrawn the dynamics of business lending. In the 2019 federal budget, the Coalition government pledged tax cuts for SMEs and an extension of the instant asset write-off.

These measures came only weeks after the announcement of a $2bn SME securitisation fund expected to increase the availability of credit and lower borrowing costs for business owners.

While the new initiatives were welcomed by SMEs, Street says there are other ways that government can boost private sector funding lines.

“We are of the opinion that the government doesn’t necessarily need to be providing direct financial support to SMEs to be of assistance. Instead, it could do a better job of making it less onerous for bank and non-bank lenders to offer a wide range of suitable SME finance products, which are less costly to fund,” he says.

According to Street, the cost and availability of SME finance is adversely impacted by direct and indirect regulatory overlays and the “significant amount of capital lenders must commit”.

He adds, “Essentially there is a disincentive to be active at scale in this area. Finance should always be priced according to risk, yet Australian businesses are additionally paying the price one way or another for an overly conservative, unsympathetic and largely indifferent stance by regulators whose approach has barely changed in decades.

“In real terms, we’ve been going backwards.” Regardless of what Australia’s new government sees as the most pressing issues for SME finance, the lenders – and the brokers who support their businesses – are fully aware that SME owners are driving a new approach from all those involved.

No longer are business owners wooed by brand loyalty; they value speed, service, efficiency, assessment criteria and credit policy, and they assess their experience on a transaction-to transaction basis.

This means that while some SMEs still turn to their primary banks as the default option, that number is shrinking as more and more depend on their brokers to present suitable alternatives.

Crucially, in this fickle and turbulent market it is these factors that are driving the development of the SME finance space, meaning brokers – as well as banks – need to be aware of the changing demands of discerning entrepreneurs.

“The shift away from traditional lenders means the role of brokers as trusted advisers is more important than ever. There has never been a better time for brokers to partner with alternative lenders, and we’re here to support them with the tools and resources to grow their business,” says Bauld.