With its prime loans now outperforming its core product suite, Pepper Money is poised to dominate a new sector of the non-bank mortgage space. Aaron Milburn, director of sales and distribution, tells Australian Broker what this means for the market

Many established market dynamics have been turned on their head in recent months. Interest rates are at new lows, bank accounts can be opened with a smartphone, and non-banks are outperforming established lenders.

Pepper Money has become the latest non-bank lender to be ushered by the market in a direction it didn’t entirely expect. In 2012, Pepper Money stepped into the near prime space, a move it tactically executed to complement its then existing suite of non-conforming products. The following year, identifying another gap in the market, Pepper Money started to do prime mortgages differently by returning to what Australian CEO Mario Rehayem calls “old-school underwriting”.

The move paid off. Although popular from the start, Pepper Money’s prime loans really gained momentum last year. In 2018, the non-bank lender originated more prime than near prime or specialist loans; prime loans made up 54% of its total loan book for the calendar year, compared to 11% for specialist loans and 35% for near prime loans. Brokers originated 95% of the prime loan book over the course of the calendar year.

“Put simply, we look at borrowers through a real-life lens, rather than as a number or another application,” says Aaron Milburn, Pepper Money’s director of sales and distribution.

“With the environment proving difficult for most home buyers, the increased certainty of an outcome using Pepper’s proven approach has been incredibly popular with brokers and, in turn, their customers.”

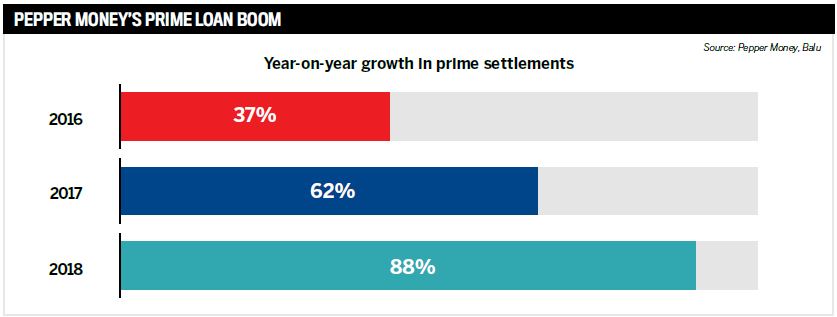

While the royal commission and tightened lending criteria at the banks no doubt contributed to the trend, it has been building for years (see the graph below).

“What has happened is that traditional banks have become more risk averse, while we continue to operate under a risk-based pricing model, and it’s that consistency and certainty in our credit appetite that has helped us excel in an uncertain marketplace,” Milburn says.

“So, while someone might be considered too high a risk from a traditional lender’s perspective, we are often willing to take on that risk because we’ve made the effort to really understand the individual’s circumstances. We take great care to offer the borrower a solution that is suited to their situation.”

Behind the scenes, Pepper has devised a new solution to address the increased demand for prime loans. In addition to its nonconforming securitisation offering (PRS), in 2017 Pepper created I-Prime, a new platform that allowed the lender to broaden its customer offering and provide prime loans to investors who have a greater appetite for this style of product.

Earlier this month, in reaction to the RBA’s historic rate cut, Pepper adopted lower promotional rates – originally offered temporarily across several Pepper home loans – as the standard variable rate, starting at 3.12% for P&I and interest-only loans across various LVR bands. Pepper also lowered its interest rate floor from 7.25% to 5.85% and increased its interest rate buffer from 2% to 2.5%.

Points of difference

That a specialist lender’s prime loans are outperforming its core products is one story. However, that brokers are responsible for 95% of that business is also newsworthy.

According to Milburn, not only has the trend continued year-todate in 2019, but there are several reasons for this. When an application is lodged with Pepper, it is assessed under three credit policies: prime, near prime and specialist.

“That policy, combined with our faster turnaround times and the fact that we allow debt consolidation and cash out on a prime loan, meant brokers were able to get their customers the loan they needed, faster,” Milburn says.

Backed with such tools as the Pepper Product Selector, this all but eliminates the heavy lifting for the broker in terms of credit policy knowledge.

Brokers also received a helping hand in 2018 when Pepper launched its consumer-facing Real Life campaign, highlighting its focus on people and their individual circumstances rather than products and type of lending.

Brokers also received a helping hand in 2018 when Pepper launched its consumer-facing Real Life campaign, highlighting its focus on people and their individual circumstances rather than products and type of lending.

“Consistency in credit is important for brokers, as it allows them to confidently recommend a particular lender to their customer, knowing they will get a suitable outcome,” Milburn says.

“That’s the beauty of Pepper’s cascading credit policy – whether the customer is expecting a prime loan or not, it’s an approval nonetheless, and in today’s environment, that’s the outcome many are seeking.”

The power of alternative

Over the last two years, property developers, businesses and consumers alike have turned to the non-banks in droves. In fact, in the first nine months of last year, loans and advances by non-bank financial intermediaries rose by 11.4%. It was the strongest annual growth in 11 years, and according to Milburn, it’s mostly down to brokers.

“The valuable guidance an experienced and diversified broker can provide is vital and ensures borrowers get the best outcome from an array of credible and reliable lenders, like Pepper Money,” he says.

“Now that brokers have experienced the Pepper difference – our turnaround times, the flexibility in our product range and the technologies we provide to help them get their customers a solution – we’ve seen a greater willingness from brokers to keep recommending Pepper for prime.”

Assuming current trends continue and non-banks keep outperforming traditional competitors on everything from product range to service, the future could see even more drastic changes for borrowers – not to mention the wider finance ecosystem.

“Whilst many borrowers have likely never needed to consider an alternative lender in the past, the changing lending landscape throughout 2018 and 2019 has exposed them to other lenders in the market that offer a genuine alternative and who can help them succeed. This is all due to the efforts of mortgage brokers,” Milburn says.

The majors won’t relinquish their market share without a fight, but the ability to bring their A game to the ring is somewhat limited, and clumsy legacy IT systems are just the tip of the iceberg.

For Pepper, such market factors are merely background noise. Its focus moving forward will remain on offering borrowers a diversified and flexible product suite backed by real-life decisionmaking. For brokers, the focus will be on education and empowerment.

“For us, it’s really about helping a wider range of people by always looking at the bigger picture,” Milburn says.

“We take their individual circumstances into account, and in many cases, we can accept situations that some traditional lenders will decline.”