Brett Halliwell, GM of white-label pioneer Advantedge reveals the plans to increase digital capability and keep brokers ahead of the game

It comes as little surpise that quality products at a competitive rate are enormously popular. What can come as a surprise is just how popular they are. According to the benchmark study by Canstar Blue, 65% of consumers select white-label grocery products over big-name brands, and 76% of consumers rate white-label products as good quality.

White label is even tipped to be the driving force behind Amazon's next wave of growth. As the recently launched Amazon Basics does well Down Under, in the US the online retail giant projects sales of $700m on white-label Amazon groceries following its acquisition of Whole Foods. In the UK in 2011, more white-label products were launched by the major supermarkets than branded alternatives.

When it comes to white-lable lending, the products is a true made-in-Australia concept.

Introduced by NAB subsidiary Advantedge Financial Services, white-label loans today enjoy a growing product footprint and, with a migration of customers away from the majors, Advantedge is in high demand.

According to Advantedge's own white paper on the subject, the popularity is driven by three factors: the pursuit of customer satisfaction, the business benefits to brokers, and the added reach for aggregators.

"When translated to mortgages, consumers easily grasp the concept of what a white-label product is. They can see the benefit of acquiring a mortgage white label so, all in all, I think that will continue to be a growing trend in Australian mortgages, just as it is in the supermarkets,” Brett Halliwell, Advantedge general manager, says.

For Halliwell, the defining trend in the space is growth – something that goes hand in hand with popularity. That directly translates into increased business for Advantedge – the leading white-label lender in Australia – and its partners, as well as better deals for the customer.

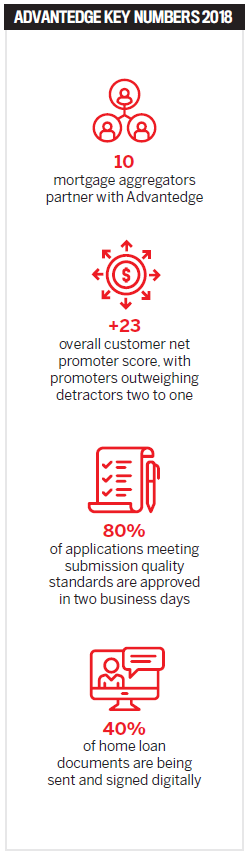

In 2014, only 35% of brokers in the market had access to Advantedge white-label products, today that figure is 85%.

“White-label lending is now a well accepted and well entrenched proposition within the Australian broking market. It has developed a strong and well-known reputation accompanied by a strong market share,” Halliwell adds.

That said, he won’t be taking his foot off the pedal any time soon, adding, “We never take it for granted that we will win business other than by meeting broker, lender and customer needs. That is our ongoing commitment.”

However, keeping ahead of the current game isn’t enough – Advantedge must also position to adapt to the next wave of changes.

Digital leader

A natural pioneer, Advantedge is now building on its leading work to implement digital solutions across application, assessment and approval. For Halliwell, it is the key to improving the mechanics of the industry.

“If we look at the digitisation of the sector, which has been led by Advantedge, it makes it more convenient and efficient for the consumer to have their information provided to the lender, but also review and sign their contract at the end of the process.”

Answering the consumer’s call, in 2017 Advantedge introduced digital document signing and digital identify verification through the apps IDme and ZipID, supplied by DocuSign, MSA National and Equifax. Citing recent applications, Halliwell reports it’s now possible to lodge on day one, receive approval within two days and return the customer documents within three.

“That’s absolutely unparalleled in terms of both benefits for the customer and the broker,” he says, confirming approximately 40% of all documents are now signed digitally.

This innovation was part of a suite of new apps introduced to improve broker efficiency and customer service. In the coming 12 months, Advantedge will prioritise the “ongoing uptake of digital capabilities by brokers” in the name of improved satisfaction.

Naturally, customers will turn to their brokers for guidance until the new technology becomes familiar, meaning brokers have a key role to play.

“Digitisation and the guidance provided by brokers can sit hand in hand. For example, in signing up to digital documents the broker is very much able to sit alongside the customer and walk them through, just like on paper. The difference is, when processed digitally, you don’t have to suffer the time delays imposed by post,” Halliwell explains.

Driven by satisfaction, price and product, feedback from customers has been consistently positive, as confirmed in the lender’s recent end-customer NPS of +38, up from an already high NPS of +23 in August 2017

Brokers who helped clients take out an Advantedge loan received an overall NPS of +78, up from +70 in August 2017, according to 476 brokers, along with 765 residential home loan customers.

The brokers are happy, too. According to the Advantedge half-yearly broker satisfaction survey, which ran in February 2018, Advantedge achieved a consistently strong Net Promoter Score (NPS) of +45.

Business booster

Advantedge’s portfolio of white-label products is constantly evolving.

In 2015 alone, six bespoke white-label partnerships were announced, with leading aggregators Astute Financial, AFG, Connective, Loan Market, LJ Hooker Home Loans and Smartline. Quantifying the pros from the partner perspective, the AFG pilot program initially generated $50m in application volumes. Once partnered with Advantage that figure increased by a further $150m in the pre-launch to a spike of $350m within a month of launch.

In February 2018, Advantedge rolled out special variable rates for new owner-occupier and investor borrowers. For a limited time, Advantage’s founding brands for NAB-owned aggregators – PLANLend, ChoiceLend and FASTLend – will offer new owner-occupier P&I interest variable rate lending at 3.69% pa compared to 3.83%. New residential investor interest only variable rate lending will be offered at 4.49% pa, compared to 4.63%.

Advantedge continues to offer its existing 3.99% pa special variable rate for residential investor P&I borrowers.

Helping brokers to keep one step ahead of the latest developments, online tools are available to understand each product, supported by POS literature. However, new products and digital solutions aren’t the only developments brokers need to keep ahead of in 2018.

Because the market is built on trust as much as anything, it will be a truly industry-wide effort to buoy customer confidence throughout the investigations and hearings ahead. Halliwell welcomes the greater clarity he expects to emerge as a result and he – and Advantedge – are fully prepared to step up in a more competitive marketplace.

“Over recent times we have seen an increased share of mortgage flows going to the big four and [from that] we can dictate a level of competition. We plan to maintain and grow our share by offering brokers and customers services that can exceed those provided by our competition,” he says, concluding, “There is no magic bullet.”

Halliwell predicts mortgages – as a portion of the total loan market – will increase from a 53.6% share currently to 60% “in future years”. Proving he’s likely to be right, brokers settled $200bn in residential loans last year. Halliwell also remains upbeat about future growth prospects in white-label and digital innovations, as customers seek ever better deals.

He adds, “I think customers will increasingly look towards the entire experience rather than the raw commodity of the product. That means they will look to the service, the products, the price but also the process that is used to make the acquisition of a home loan better.”