Canstar has revealed the mortgage rate changes for the week Nov. 13-20, as well as shared some tips on how home loan borrowers can save on repayments.

Canstar’s latest Weekly Interest Rate Wrap-Up showed that 33 lenders raised 332 owner-occupier and investor variable rates by an average of 0.25%, while two lenders cut theirs by an average of 0.18%. Several fixed rates, too, had changed over the past week, with 21 lenders increasing 473 rates by 0.25%, and three others slashing nine rates by an average 0.16%.

See table below for the fixed and variable rate adjustments last week.

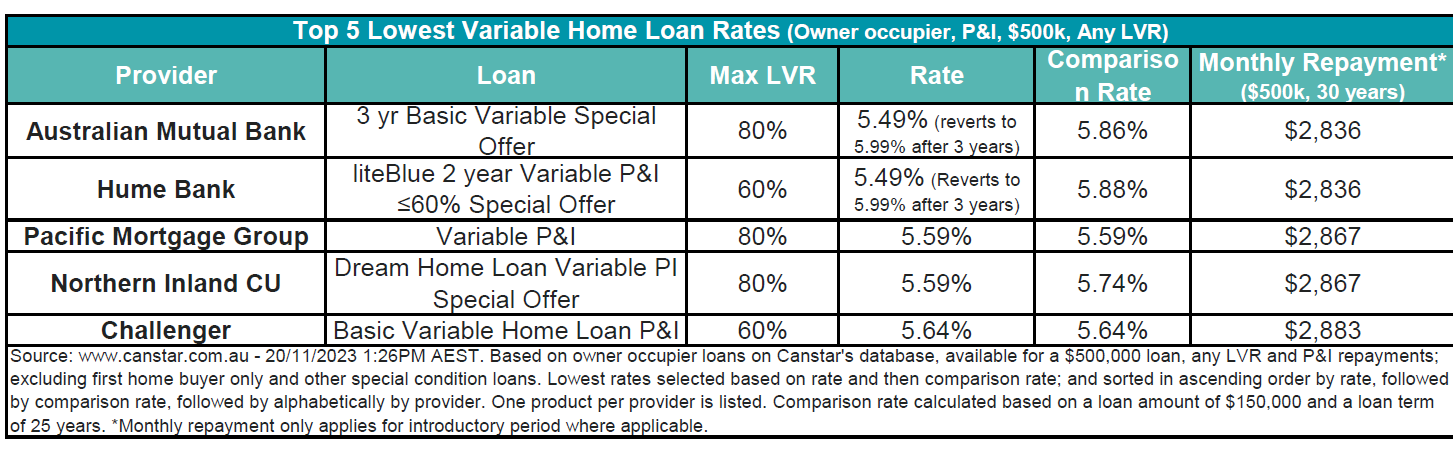

Following the changes, the average variable interest rate for owner-occupiers paying principal and interest now stands at 6.80% at 80% LVR, with Australian Mutual Bank and Hume Bank offering the lowest variable rate at 5.49% at introductory terms.

The Canstar database still has eight rates below 5.5%, consistent with the previous week. These rates were from Australian Mutual Bank, Hume Bank, LCU, and RACQ Bank.

For the top-five lowest variable home loan rates, see table below.

Effie Zahos (pictured above), Canstar’s editor-at-large and financial expert, said that with homeowners actively seeking avenues to cut costs that in the wake of 13 consecutive rate hikes, cashback site, Grow My Money, formerly known as Super Rewards, could just be the thing they need.

“Typically, cashback providers receive a commission from linked retailers each time you make a purchase via the app or website,” Zahos said. “Part of this commission is returned back to you, usually as a percentage of the purchase price you paid. Grow My Money gives you the option of getting the cashback paid into your home loan or your superannuation account.”

Canstar’s number-crunching revealed that a $40 monthly cashback can potentially slash the total interest paid by approximately $30,000 on a $600,000 home loan over a 30-year term.

Another effective method for reducing interest on a home loan involves fully utilising the offset account, by arranging for the salary to be directly deposited into the offset account and using a credit card with interest-free days for expenses.

“The idea is that you live off your credit card while keeping your pay in the offset account to work on reducing your interest bill,” Zahos said. “You then need to pay off your credit card in full before the end of the interest-free period.”

Canstar said someone with a $600,000 home loan for 30 years at an average rate of 6.95%, earning a monthly after-tax income of $6,012 with monthly expenses totalling $2,040, could potentially reduce their estimated interest bill over the loan’s lifespan from $829,807 to $789,233. This could result in a significant saving of about $40,500 and a reduction of the loan term by 10 months.

But for this strategy to be effective, Zahos urged homeowners to not overspend, carefully consider associated fees, and ensure that the home loan interest rate remains competitive when implementing these money-saving strategies.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.