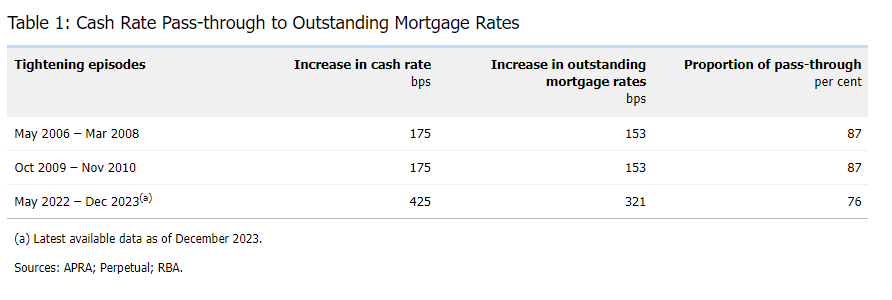

As the Reserve Bank (RBA) raised the cash rate target by 425 basis points from May 2022 to December 2023, the average outstanding mortgage rate increased by approximately 320 basis points, reflecting a 75% pass-through rate.

The lag in response compared to previous tightening cycles in 2006 and 2009, where nearly 90% of the cash rate increases were passed through, can be attributed to a high proportion of fixed-rate loans and intense mortgage lending competition, according to an RBA Bulletin.

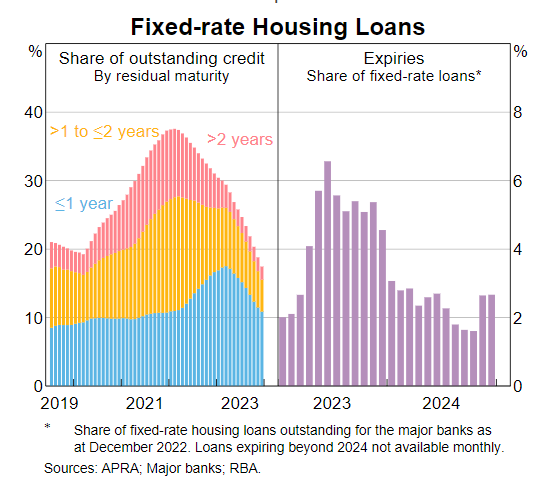

A significant factor contributing to the slower pass-through rate is the large share of fixed-rate mortgages taken during the COVID-19 pandemic at historically low rates.

“Many borrowers took advantage of the low fixed rates on offer during the COVID-19 pandemic to lock in their mortgage repayments for a period,” RBA said in the Bulletin.

As these fixed-rate periods expire, these loans are expected to reprice at higher current variable rates, which will lead to an increase in the average outstanding mortgage rate.

Another crucial element affecting the pass-through rate is the heightened competition among mortgage lenders, particularly in the latter half of 2022 and early 2023, RBA reported.

This competition has led to the average mortgage rate on outstanding variable-rate loans increasing by around 75 basis points less than the cash rate increase.

Banks and other lenders have been aggressive in retaining quality borrowers by negotiating lower rates and offering incentives such as cashback deals and rate discounts.

The remaining stock of low-rate fixed mortgages is set to expire throughout 2024, likely resulting in a more complete pass-through of cash rate hikes to mortgage rates, mirroring previous economic tightening cycles.

RBA expects the average outstanding mortgage rate to rise by an additional 35 basis points between December 2023 and December 2024, as the pace of fixed-rate loan expirations remains elevated in the first half of the year.

Despite the slower initial response, the impact of higher mortgage rates on household cash flows remains a potent channel through which monetary policy influences the broader economy.

As more fixed-rate loans adjust to higher market rates, the total scheduled household mortgage payments are projected to increase, potentially reaching around 10.5% of household disposable income by the end of 2024.

The dynamics between cash rate increases and mortgage rate adjustments highlight the complex interplay of fixed-rate loan expiries, mortgage lending competition, and monetary policy. By the end of 2024, the extent of pass-through is expected to align with historical norms, reflecting the delayed but inevitable impact of monetary tightening on mortgage borrowers, RBA said.

To read the RBA Bulletin in full, visit the RBA website.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.