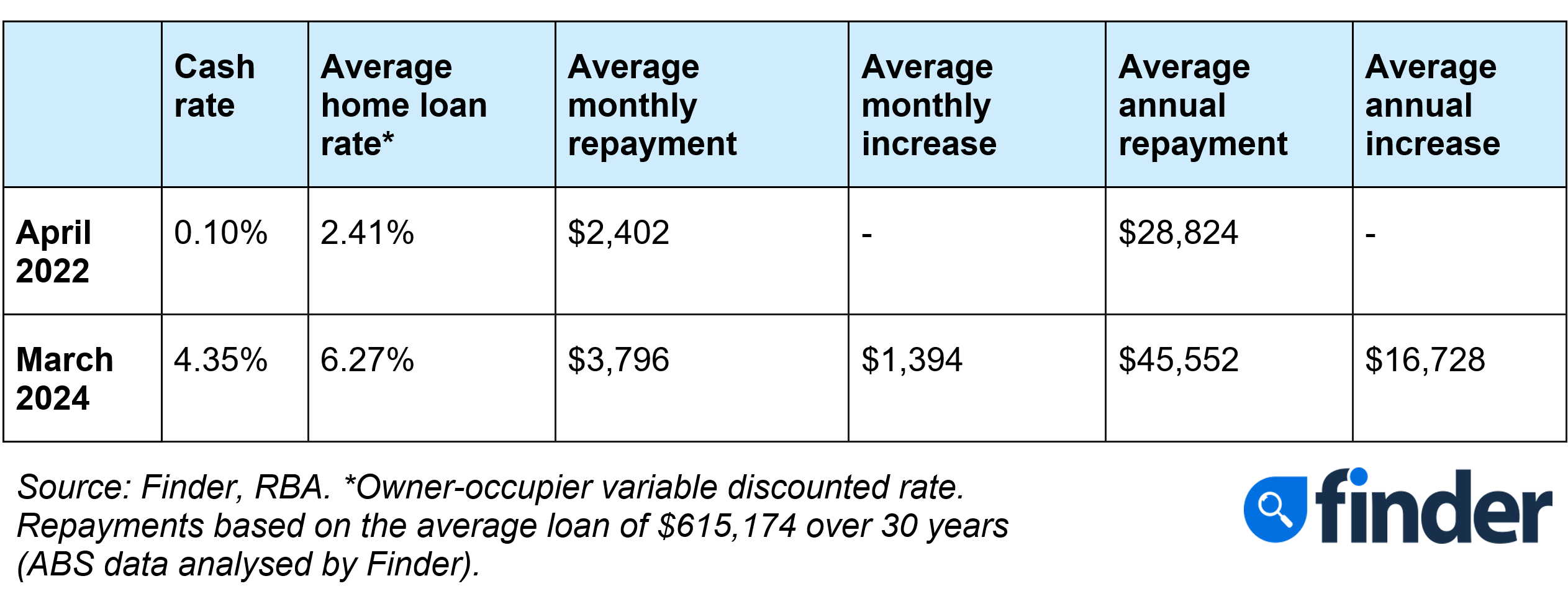

The Reserve Bank of Australia (RBA) decided to maintain the official cash rate at 4.35% at its March Board meeting. This follows a period of careful consideration amidst recent economic data.

The decision aligns with market expectations, offering stability for Australian borrowers on variable interest rate loans after a period of rapid rate rises.

While inflation remains above the target band of 2% to 3%, rising 3.4% in the 12 months to January, this holding pattern allows the RBA to assess the ongoing impact of previous rate hikes.

The RBA board said it remains "resolute" in getting inflation back to the target bank and recent information suggests that inflation has continues to moderate.

"The headline monthly CPI indicator was steady at 3.4% over the year to January, with momentum easing over recent months, driven by moderating goods inflation. Services inflation remains elevated, and is moderating at a more gradual pace. The data are consistent with continuing excess demand in the economy and strong domestic cost pressures, both for labour and non-labour inputs," the board said.

"The Board needs to be confident that inflation is moving sustainably towards the target range. To date, medium-term inflation expectations have been consistent with the inflation target and it is important that this remains the case."

The RBA’s decision to hold rates steady has elicited mixed reactions among brokers. While many expected the unchanged rate, three mortgage experts have offered insights into how it might impact borrowers, consumer sentiment, and the mortgage industry.

For borrowers, the wait-and-see approach offers a chance to breathe.

Veronica Vojnikovic (pictured above centre), director of Vevo Financial Services, sees the RBA’s decision as an opportunity for borrowers to "review their options with time and ease" without the pressure of rising rates.

“I think it’s important to continue having valuable discussions with clients wanting to improve their financial situation,” Vojnikovic said. “We are actively monitoring lenders proactively making changes to support borrowers following the aftermath of the rate tsunami.”

This aligns with mortgage broker James Brett’s observation of increased competition among lenders, potentially leading to "discounting even without immediate RBA-delivered relief." This could benefit borrowers with strong financial standing.

“Some of our clients remain in disbelief at their borrowing power reductions over the last two years and will be delighted to see an increase from what they feel is a current constraint,” said Brett (pictured above left), principal mortgage broker and finance specialist at Truly Finance.

However, Vojnikovic also highlighted the impact of rising costs on Australian households, with some resorting to credit cards and seeing a decline in the value of new and refinanced home loans. This suggests the current rate may need to hold for some time.

Consumer sentiment appears cautiously optimistic. Aaron Bell (pictured above right), director of Home Loan Village, expects confidence to rise gradually if rates remain stable. This could lead to a more sustained positive outlook for the year.

For the financial services industry, the impact seems muted. Bell expects minimal effect on his business, while brokers like Brett advise clients to seek rate reviews for better deals.

“To be honest, I think most people will still be getting used to the RBA meetings being every six weeks or so as opposed to the first Tuesday of the month, and so this announcement itself mid-month will likely be far more of a surprise to most than the unchanged rate,” Bell said.

While some borrowers may be disappointed by the lack of immediate relief, the hold could signal a gradual decrease in rates later in the year, fostering a more confident economic environment.

Vojnikovic said the slowdown of inflation and continued mixed readings will most likely see the RBA keeping the rate on hold until June or even as far as September until inflation moves progressively towards its target range.

“I certainly think a pause will be the new normal this year until the RBA gain some more confidence,” Vojnikovic said.

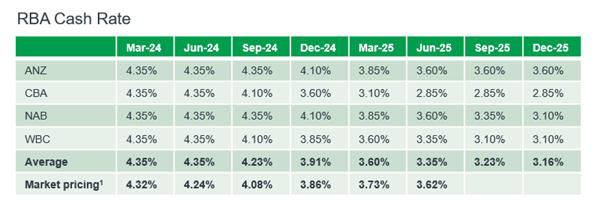

Bell agreed, predicting one or two rate cuts this calendar year and possibly another couple in 2025. However, he acknowledged the RBA's potential caution in ensuring inflation is controlled.

“I’ve been seeing quite a few salaries that have had relatively substantial jumps in their take home pay packet over the last six months or so…,” said Bell, referencing the recent wage increases for teachers and aged care workers.

“While these are very well deserved of course, sustained increases in wages will put pressure on inflation which could potentially come under a little more pressure as the year progresses,” Bell said.

Brett’s forecast aligns with the big four banks' economists, predicting two rate cuts by year-end.

He justified this outlook based on controlled inflation, rising unemployment, and recent data suggesting that the upcoming Stage 3 tax cuts shouldn't fuel inflation. However, he also was concerned about the potential consequences.

“Somewhat concerning about these forecast decreases, is that some borrowers may push their borrowing power to newer higher limits, which may increase demand for homes and their prices of dwellings will continue to climb,” Brett said.

“This is concerning for those who are saving to buy, particularly first home buyers.”

With the market adapting to interest rates moving past its peak, Vojnikovic said she has started to see lenders reduce variable rates and offer competitive fixed rates in anticipation for the upcoming RBA rate cuts.

“We will continue to see fixed rate offers come into play for clients wanting stability,” Vojnikovic said.

“We don’t know how many rate cuts are expected this year, which may deter clients from fixing for the time being. We may start to see lender policies and servicing ease up as the economy recovers.”

Bell said the property market has continued to be resilient despite sustained high rates driven by limited supply and strong demand.

On the supply side, there's a general lack of available housing and land, coupled with high construction costs. This restricts the number of houses available for purchase.

Meanwhile, wealthy immigrants continue to enter the market, and government programs are actively stimulating demand.

“There is also the fact that the housing market will have a lag effect once monetary policy is implemented- and sustaining higher interest rates is still implementation of monetary policy,” Bell said.

Brett said some in the market have been “white knuckling” and are still coming to terms with the rapid-fire increases of the recent tightening cycle.

“They would be very keen to see the forecast rate reductions as soon as possible,” Brett said.

“Some in the market are not borrowers, so they’ll be less keen to see the rate peak in their rearview mirror, as it will impact their returns on cash holdings.”

What do you think of the RBA’s decision to hold the cash rate? Comment below.