By

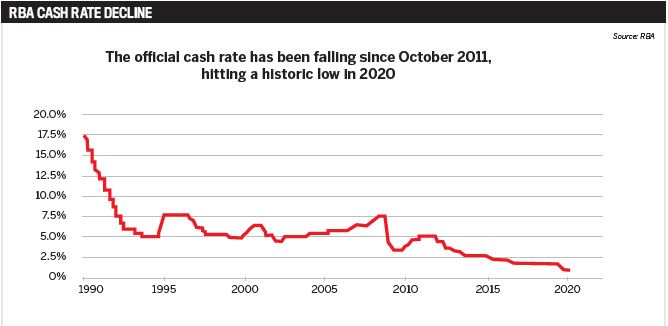

The official cash rate has been slashed to its lowest level on record – just 0.25%. Banks typically use this rate as a guide to set interest rates on their products, such as home loans and savings accounts.

In more typical circumstances, the Reserve Bank’s decision to institute the second rate cut last month would likely have infused optimism into the Aussie housing market; RBA research has revealed there is an inverse relationship between cash rate changes and property price movements.

The rapid increase in the value of residential properties from June 2019 was in large part tied to the series of cash rate cuts made over the year. However, according to CoreLogic analysis, the current situation of “extreme uncertainty and economic fragility” means housing market activity is unlikely to lift, even with the historically low cost of debt.

So, while there is no question that COVID-19 continues to wreak havoc on Australia’s economy and people’s lives, brokers and banks are facing another challenge: how to maintain the long-term loyalty of customers to their mortgages given the lower interest rate environment.

Joel Larsen, head of customer engagement and home ownership, Westpac

Joel Larsen, head of customer engagement and home ownership, Westpac

Challenges magnified in a low interest rate environment

Speaking at the Australian Mortgage Innovation Summit 2020, Joel Larsen, head of customer engagement and home ownership at Westpac, said mortgages had traditionally meant a 30-year relationship with the bank, but this was not the world we lived in any more.

He explained that relationships with clients were becoming a lot shorter, as consumers had many more options before them. This was especially true for the major banks, which he said now had to make sure they were presenting enough value to customers throughout the life of their loan.

“I think that’s going to continue to be one of the main challenges that majors face,” Larsen said.

But for ME Bank’s general manager of home lending, Andrew Bartolo, the challenges for a non-major bank are very similar.

He says, “I think two key ones are the volume of regulatory change, but also, in a low-credit, low interest rate environment, the competition is quite intense. On the regulation bit, the challenge is the change coming at us all at once and the resources that are consumed. As a smaller bank with less resources, it’s challenging consuming all that change at the same time. And now that the RBA has cut the cash rate to 0.25%, it makes it a lot harder for consumers to differentiate between lenders. We’re in a low-rate environment for a reason; obviously, that’s to stimulate economic activity. The visibility of that to consumers means customers are shopping around more.”

In such an unprecedented economic landscape, banks therefore need to think about how they can offer an experience that goes beyond price. Bartolo said this meant thinking about “how are customers interacting with us” and “how do we take friction out of the process to enhance value”.

Larsen added: “The more immediate challenge with the low-rate environment is how quickly it stimulates housing, and how quickly house prices are growing and how that changes the credit dynamic, especially in Sydney and Melbourne. With that dynamic taking place, the house price rise that we’re seeing at the moment does also put pressure on the system, because it changes consumer expectations.

“Unfortunately, sometimes it means a lot of people miss out. There’s the consequence that while consumers are now expecting a lower rate, they are able to borrow more, and they’re probably going to pay more. Managing that dynamic is equally risky.”

Byron Donovan, head of commercial management, NAB

Byron Donovan, head of commercial management, NAB

Challenges of open banking

The start of open banking this year will bring a whole host of opportunities for the industry, but it could still take some time before the full benefits are realised.

According to Byron Donovan, head of commercial management at NAB, who also spoke at the summit, there is a big trust element in opening up data to other providers.

“That’s going to be critical from day one. How you build that trust with consumers that they’re able to hand over access to their data and trust it’ll be used appropriately. A big part of that will be transparency around how it’s used, how it’s consumed, and ensuring you’re using it appropriately,” Donovan said.

“Customers are increasingly expecting that from all their service providers around how you can trace and track and understand where you are at and what people are doing with what you’re investing.”

“Whether it’s face-to-face or over the phone, humans still crave a human connection, particularly in the context of the home buying process” Byron Donovan, head of commercial management, NAB

Indeed, the element of transparency, protection and trust will become critical for brokers and their clients to unlock the full potential of what that data can reveal.

But does more data just create additional complexity, especially given how many players are involved in the mortgage process, such as brokers, real estate agents and solicitors – and how can they all work together to use the data effectively?

Andrew Bartolo, general manager of home lending, ME Bank

Andrew Bartolo, general manager of home lending, ME Bank

Bartolo admitted that brokers’ and lenders’ systems wasted a lot of time and were not as effective as they could be.

“You think about things like income expense verification or fraud checks. We’ve got some broker groups and aggregator groups doing those sorts of checks for meeting their own obligations, and then the lenders are doing the same thing on their side,” he explained.

“That creates duplication of cost and everything in the system. I’m not sure what the solution is right now, but I do think there is something for us to think about as an industry around how to streamline that data capture so that we can remove the waste and redeem value.”

But can data alone replace the value that stems from having a conversation with a customer, which is critical to responsible lending today in order to understand the customer’s situation?

Donovan said, “The data tells a part of the story, but it doesn’t tell the whole story, or talk about what their lifestyle will look like post taking out the loan, versus what it is today. You can use it to help inform the conversation, but I don’t think it should dictate the entire conversation.”

Similarly, Bartolo said, “Whether it’s face-to-face or over the phone, I think humans still crave a human connection. Particularly in the context of the homebuying process, there are situations where some circumstances are more simple than others.

“I think the data and the technology will be there to help inform and take friction out and make quicker decisions. But I also think there’s a level of judgment we’re going to have to still apply, and that customers are thinking about that guidance and advice as well.”

He added that the industry had to work together to ensure technology and data were actually working alongside the human interface.

Changing role of the broker

Regardless of the changes that were already here and those that were still coming, Larson suggested that there was still going to be a valuable role for bankers and brokers.

“The way they interact with customers will change. It will be digitally dominated. Most of them will start online. A portion will do the whole thing online. We know the majority still need help somewhere in the process, especially when you’re buying a property,” Larson said.

“It’s different when you’re refinancing, but when you’re buying a property, it’s time-bound, it’s emotional and it’s stressful, and having an expert in there, whether they be virtual or your local broker or the branch down the road, is going to be critical.”

So a business that has a large branch network like Westpac will need to think about whether having a banker and a branch is still the right way to do business with a customer.

“The broker industry, especially the large broker firms, would have one very firm eye on their digital capability and how they can get in front of customers before they go directly to their lenders,” Larsen said.

“I think brokers will be looking at how they can innovate their offering and make it simpler for a big group of customers, and being accessible online is the most obvious way to do that.”

Donovan added: “The amount of customers we lose purely due to price is actually quite small. Being able to solve their problems in a seamless manner is critical to keeping them happy.”

Head to head with fintechs

According to Donovan, when it comes to competition between traditional lenders and fintechs, the latter have the advantage and the beauty of starting with a blank slate, so it was easier to digitise everything from day one.

He explained, “[Instead] we’ve got big legacy systems and processes that we’re working through. For us, it is around how we remove as much paper out of the process all the way through, starting with customers.

“The old days of having to fund a home loan book are changing and evolving, so you have the likes of Athena coming in, who are able to isolate and target a segment of the market and do that very well.

“As more and more competitors come in and try to compete in that space, the days of big banks being able to be everything to everyone, that offering gets harder when parts of the market are being picked off and serviced in a different way. He adds, “For us, it’s how we face that threat, but equally, being conscious of staying true to our strategy and what we think is going to keep us on the right path.”