by Antony Field, Australian Broker

The NSW government wants to make homeownership more achievable by giving buyers the option to pay an annual property tax instead of stamp duty. We asked brokers and real estate experts for their thoughts.

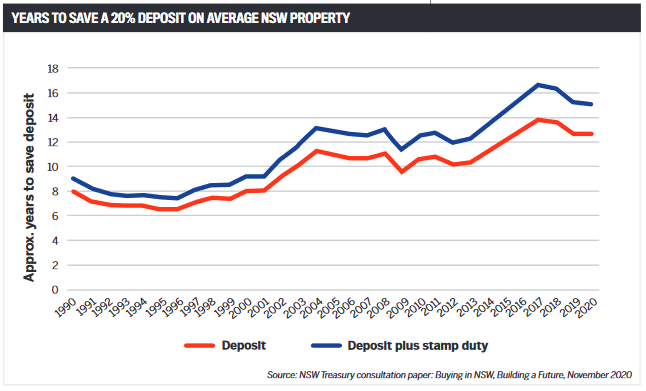

There's no doubt that stamp duty is a big financial barrier to homeownership. According to the NSW Treasury, it can take 2.5 years for an average worker to save up enough money to cover stamp duty, adding $34,000 to the cost of buying an average home.

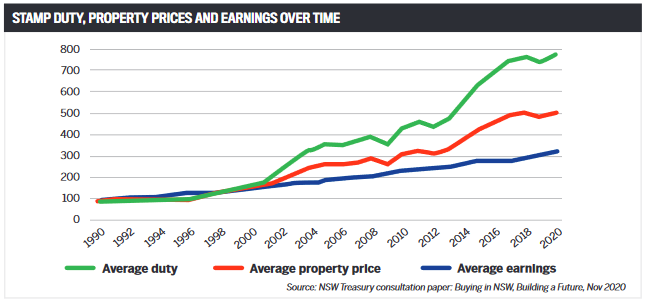

NSW Treasury statistics also reveal that, since 1990, while average earnings in NSW have trebled and average house prices have increased five times, average stamp duty on dwellings has increased more than seven times.

After many years of debate and numerous reports calling for change, the NSW government, led by Treasurer Dominic Perrottet, has decided to act, proposing an annual property tax as an alternative to upfront stamp duty.

Property buyers will be given a choice: pay an annual property tax instead of stamp duty (and land tax where applicable), or pay one-off stamp duty. The annual property tax would be based on land value – a fixed amount plus a rate applied to the unimproved land value of an individual property, similar to council rates. Stamp duty concessions for first home buyers could be replaced with a grant of up to $25,000.

The government has released a consultation paper and is seeking public feedback by 15 March.

Australian Broker sought comment on the reforms from Katrina Rowlands, managing director of Wollongong-based Mortgage Success; Trent Lee, CEO and founder of Mates Rates Mortgage Brokers in Gosford; well-known real estate commentator and trainer Tom Panos, and Real Estate Institute of Australia CEO Anna Neelagama.

Rowlands says the proposed changes to stamp duty would be a huge reform and would raise a lot of questions as to the benefits.

“Any tax reform has pros and cons – always,” she says. “I don’t know that it really will have a huge impact as either way you will still pay for stamp duty – it’s not abolished.

“Short-term holding will benefit from it as it alleviates an upfront cost, but it doesn’t negate the cost.”

Rowlands says a longer delay in paying stamp duty will lead to a more expensive duty being paid if it goes the full length of a long-term ownership.

“I see it as a flawed system as it still isn’t clear how it would end up if multiple buyers continue to defer the payment. I don’t have a firm yes or no opinion made up as yet.”

There are also questions about debt recovery.

“How will they manage debt recovery if people just can’t afford it year-on-year? How will it be charged and debited? What penalties would apply if they can’t then pay it annually?” Rowland says.

Lee says it will remove the need for buyers to pay stamp duty upfront, which averages about $34,000 in NSW – and “that is a lot of money to raise for first-time buyers in particular, so this would be removing a barrier for them to enter the property market”.

He says the reform could also help stimulate the market overall by encouraging those looking to upgrade or downsize to another property to do so, as they won’t have to factor in the cost of stamp duty.

Panos says upfront stamp duty is a major prohibitor because it stops some potential first home buyers from purchasing or delays them from entering the market.

“Anything’s that going to take away that friction point is going to be a very positive move for the whole industry, and that industry is real estate agents, mortgage brokers and all the associated services involved when people buy and sell property,” he says.

“Quite often I’m auctioning properties on the weekend and people are saying to me, ‘I still have to pay $150,000 for the stamp duty’, so it’s a sizeable amount,” Panos says.

“It doesn’t matter how affluent you are or how much disposable income you have, $150,000 after paying tax – you’ve got to earn a big salary to pay that.”

Neelagama says efforts to reform stamp duty are welcomed, but any net benefits won’t occur unless they are applied across the entire country.

“Taxes are one of the factors that determine investment in housing and thus housing supply and housing affordability,” she says.

“The changes to tax on stamp duty will bring economic and social benefits, including assisting affordability by reducing the initial transaction cost of a property and allowing those who need it most to opt for a smaller annual tax.

“While providing the option to spread out the tax is welcomed, the taxes themselves remain high.”

Lee says an increase in property prices is a potential outcome of the reform, but house prices have already been rising during the COVID-19 pandemic.

“Any changes the government makes, whether it be an exemption, bonus or in this case a deferral or deferment of stamp duty, will provide an additional catalyst to price increases,” he says.

“There could also be an impact on the rental market as more tenants are able to purchase their homes rather than rent, which could see a negative impact on rental income.”

Panos says people will move more frequently because they will have a lower barrier to selling and buying, but it is not clear if the property tax will affect house prices because there are so many variables.

“Property tax is not the biggest driver – the biggest driving factor is interest rates.”

He adds that property listings and volumes are way down, and this has caused price growth.

Rowlands says the property tax is just a different way of paying stamp duty.

“I don’t see this as a real game changer in values, to be honest, as you will still need to factor putting that amount aside weekly or monthly to cover the annual cost. It may factor more in the first home buyer range of property than the second or third ... those that have entered the market for a second or third time may be in more of a position to pay it upfront and be done with it.”

First home buyers may be incentivised to enter the market if the tax is an annual small payment and they benefit from a proposed grant of $25,000, Rowlands says.

Neelagama says the latest REIA Housing Affordability Report found that Australia recorded a 10-year high in affordability for first home buyers due to low interest rates and government stimulus, but spreading the tax out should further incentivise the market.

“The data shows that providing fairer options works to keep the housing market stable rather than causing prices to inflate heavily.”

Panos says the tax will bring about a more fluid property market.

“It’s another barrier which is slightly removed which is going to allow people to make decisions to move,” he says. “You might find people instead of doing renovations saying let’s not renovate, let’s just actually upgrade.”

Panos says his biggest issue with the property tax is getting clarity as to when it will come in and what exactly it will entail. “Because a lot of people often procrastinate. They’ll hold off and say, I’ll wait to when the legislation goes in. The anticipation of it actually stops people making decisions.”

Lee says there is still a good supply of new housing coming onto the market thanks to stimulus measures such as HomeBuilder.

“I don’t think downsizing decisions are driven by the cost of stamp duty,” he says.

Neelagama believes the property tax will benefit first-time owner-occupiers, who can delay an upfront payment while also stimulating the market, particularly those wanting to downsize but who have been discouraged by large stamp duty taxes.

But Rowlands is not so convinced the tax will lead to more downsizing, because she says people in that situation usually have a reason to lessen their financial burden and have planned on the equity to buy the home outright or at a lower lending end amount.

“So to then create another annual fee for the stamp duty rather than complete the payment at the changeover seems to contradict why most people downsize,” she says. “They downsize to remove financial commitment as a rule.”

Brokers, says Lee, will always benefit from more property sales, and making it easier to purchase property will likely increase sales.

“The ongoing property tax will need to be factored into the loan servicing, which the brokers should be taking into consideration when assisting their clients.”

The reforms may assist the first home buyer to engage sooner in the market and therefore boost the housing market, Rowlands says.

“New buyers enter and second home buyers move on and out to new areas or up in price. This also will always then help brokers as the market expands. It may encourage shorter-term holds as it lessens the burden of moving in some ways and, as such, transaction numbers may increase for the broker industry.”

It sounds fantastic when you hear it, says Panos.

“That’s like saying, let’s get rid of tax. But there’s a model behind it. Where would you get the money to make up for it? There’s a whole ecosystem – people pay a tax for other services around the country.”

Rowlands questions how the NSW government could remove stamp duty when it has a $16bn deficit.

“And if they do, they will just replace it with another ... it’s idealistic to think that, after the year we have had and the government spend to help us all survive, that now they can cut taxes.”

Lee says the removal of stamp duty is unlikely, given the COVID-induced economic challenges at state and national levels.

“They still require the revenue to pay for infrastructure, public transport and schools, etc,” he says.

Offering the option of stamp duty or property tax would give buyers a choice, Lee says.

“They may feel they have more financial freedom long-term by paying upfront stamp duty. But the property tax option gives those struggling to save for a deposit a pathway into the property market.”

Neelagama says housing is one of the most heavily taxed sectors of the Australian economy, so national reforms remain much-needed.

“On a national level, stamp duty on conveyances is inconsistent with the needs of a modern tax system and should be replaced with a more efficient way to raise revenue,” she says. “Property transactions across the board would no doubt improve with the removal of inefficient housing taxes.”

Rowlands says her initial answer is no – each state needs to set its own recovery plan and identify the areas that need the most attention.

“This is a larger question that covers one policy of tax reform.”

Lee believes there is no one-size-fits-all option.

“All the states and territories have vastly different property markets, and whilst state governments rely upon stamp duty as revenue to fund infrastructure projects, the need to regulate their revenue streams to do that will need to remain a local decision,” he says.