Yesterday, 20 February, ASIC released the draft guidance clarifying how the new best interests duty (BID) for mortgage brokers should work.

The regulator has aimed to provide “high-level guidance” on its expectations for what mortgage brokers may need to do to meet BID when: gathering information about the consumer, making an individual assessment of what is in the consumer’s best interests and presenting information and recommendations.

While the guidance covers a wide range of topics, ASIC made sure to address specific concerns which have arisen since the release of the draft bill, including:

The draft regulatory guide was crafted to “strike a balance” between providing useful guidance and accurately reflecting the principles-based nature of BID.

1. The interaction of BID and responsible lending obligations

BID obligations operate alongside other laws that affect how credit assistance is provided to consumers. While information gathered for the purpose of complying with responsible lending obligations may help brokers comply with BID, they are distinct obligations and brokers must comply with both; generally speaking, BID demands more of brokers than the responsible lending guidelines, according to ASIC.

2. Range of credit products and providers

Brokers must be satisfied the range of products they can access and recommend is sufficient to allow them to act in consumers’ best interests. Further, ASIC expects brokers to maintain a general awareness of the other products and features available on the market.

Consumers should be informed about which credit providers the broker has access to and which they do not, as some may be unaware their broker can only offer the products on the aggregator’s panel, or that the broker may not have access to all the brands listed on their aggregator’s promotional material.

ASIC clarified they are not proposing mortgage brokers be required to recommend a specific product outside their panel, especially as some credit providers may choose not to deal with certain brokers. However, there is an expectation that mortgage brokers can satisfy themselves that recommending from within their panel is in the consumer’s best interests.

Source: ASIC

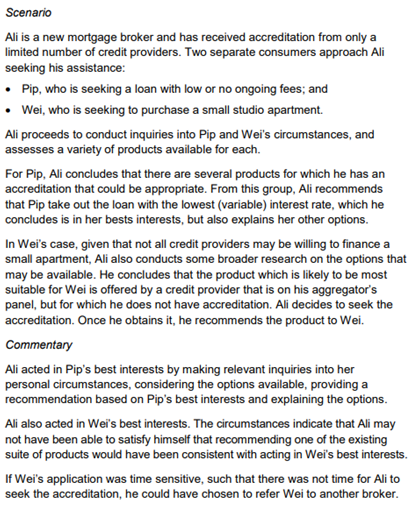

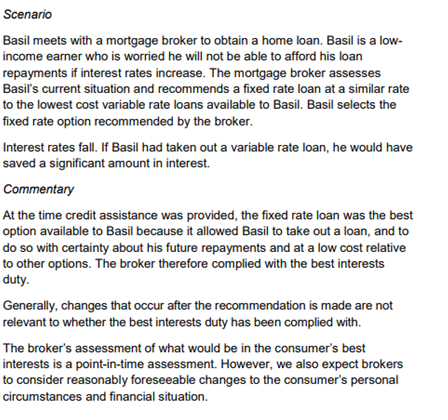

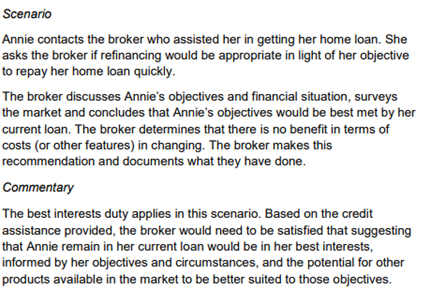

3. When the duty applies

BID applies any time a broker provides credit assistance to a consumer, based on the information available at the time.

The consumer’s individual circumstances, and the price or availability of credit products, may change between the time the consumer first contacts the broker and when the broker provides credit assistance. In these instances, brokers may need to reassess what is in the consumer’s best interests before providing credit assistance.

However, they cannot be held retroactively responsible for a change in circumstances that occurred after the initial interaction has concluded.

While BID doesn’t require brokers to conduct periodic reviews or to provide credit assistance to the consumer in the future, the regulator feels it is “good practice” for brokers to review the consumer’s circumstances from time to time.

If a broker chooses to do this, the BID only applies to any credit assistance given at that time. ASIC provided the below examples to illustrate which scenarios would fall under BID and which would not:

Source: ASIC

Source: ASIC

Source: ASIC

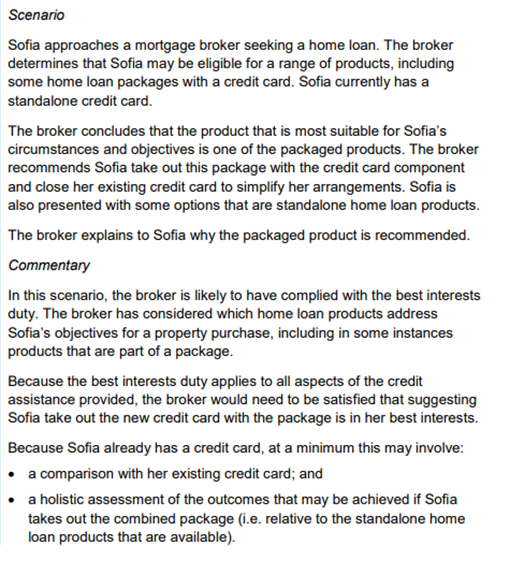

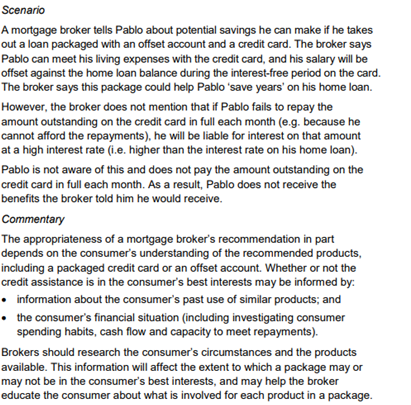

4. Packaged products or matters outside the mortgage broker’s expertise

Following the release of the draft bill, many questions centred on what BID means in instances involving a package of products and/or if there are matters that arise in the home loan process that are outside of a mortgage broker’s expertise.

ASIC has proposed that recommendations on packages should be based on a holistic assessment of the package and involve a process of comparison with other available products, both other packages or standalone home loans.

BID-compliant recommendations need to identify and consider how each product within the package would meet the consumer’s needs, objectives, priorities and preferences, before deciding whether, and why, taking out that product would be in the consumer’s best interests.

Also, while mortgage brokers should be able to give guidance about the suitability and value of product features for each consumer, including a basic understanding of tax implications, ASIC does not expect mortgage brokers to advise on matters outside their expertise.

Where tax implications go beyond a broker’s competence, the application of the BID means it would be more appropriate to refer consumers to a registered tax agent.

Source: ASIC

Source: ASIC

So, who’s at risk?

As articulated by ASIC, the brokers at risk of non-compliance are those whose processes typically lead to a “one-size-fits-all” outcome for consumers.

Brokers need to consider the individual circumstances of the consumer and their needs, goals and financial situation to comply with BID obligations.

More to come in the following days