By

Australian companies have faced a difficult start to the financial year with a significant part of the east coast in lockdown since the end of June.

Not only have business operations been disrupted, but other issues have put pressure on companies looking ahead and hoping to take advantage of the release of pent-up demand when the lockdown is lifted.

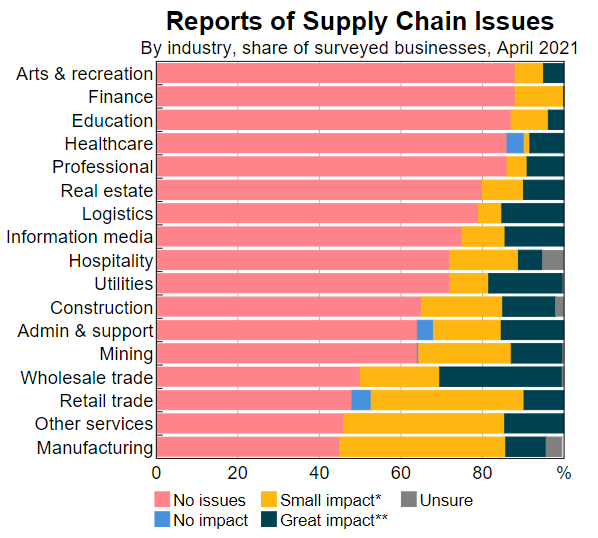

One of the biggest of these is supply chain disruption, which put simply means it has been increasingly difficult and expensive for companies to import the goods they need to supply their customers. A surge in demand for physical goods globally has contributed to the congestion and delays at the world's ports.

The instability of the global supply chain was highlighted in the RBA’s statement of monetary policy in April, with non-food retailers and manufacturers the most affected.

However, these figures were taken pre-lockdown and delays have become worse due to Delta variant disruption. This has resulted in companies seeing longer lead times and delays in shipping, with some reporting delays of up to 52 weeks.

Source: ABS, RBA

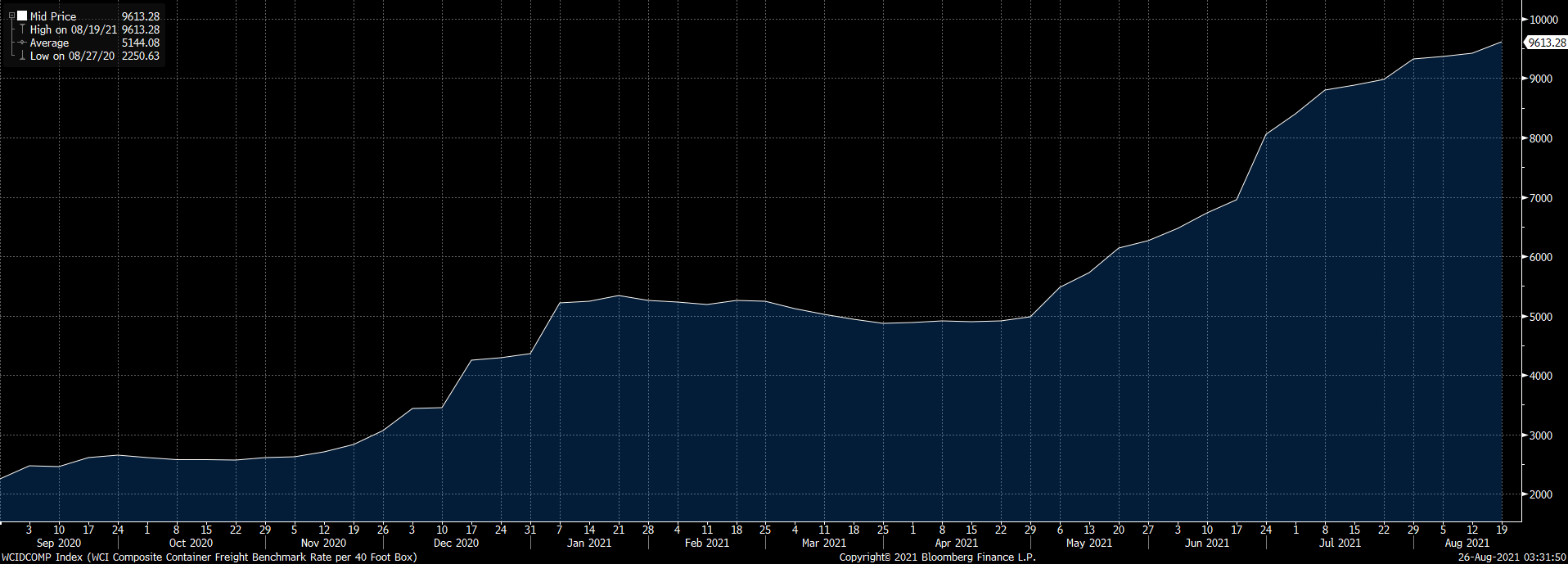

Another challenge has been the rising cost of freight, with the WCI composite index up by nearly 400% over the last 12 months.

WCI Composite Container Freight Benchmark Rate Source: Bloomberg (26/08/2021)

WCI Composite Container Freight Benchmark Rate Source: Bloomberg (26/08/2021)

In what has been a very volatile economic climate, it has been relatively easy for businesses to lose focus and not be properly positioned for an economic re-opening.

With the increasing realisation that containment of the Delta COVID variant is not possible and that the economy must be opened to avoid a double-dip recession, it is vital to be prepared for the business opportunities that will arise as a result.

NSW premier Gladys Berejiklian has ruled out lockdowns after the state reaches 80 percent double-dose vaccinations which she says could happen by the end of October. Federal support for an early end to lock downs is also strong

Using last year's economic reopening as a guide, we can expect that there will be a large amount of pent-up demand in November and December as consumers are allowed to frequent shops, suppliers and restaurants and start to make up for what they missed out on.

This was the scenario in the United Kingdom when it ditched the compulsory use of masks and social distancing and celebrated ‘Freedom Day’ in July. Consumer surveys saw a rise of 55 percent and 60 percent in hospitality and retail spending respectively compared to August 2019, before the pandemic.

One of the peculiarities of the COVID period is that household savings have increased, and we can expect to see discretionary spending increase as consumer confidence grows. In 2020, we saw consumer sentiment rise from 79.5 in August to 112 in December in a similar climate that we are seeing now.

Businesses should therefore expect a sharp up-tick in sales and demand. As this demand can ramp up quickly, this can leave businesses struggling to find the working capital to support their activity during this cash-intensive period.

From an Ebury perspective, we saw our loan book rise by 68% over the same short period last year when COVID restrictions were relaxed.

The reality is that after the prolonged hard lockdown in Victoria and New South Wales fewer small and medium enterprises have the funding right now or access to further funds to support themselves during this demand spike.

These companies need to act proactively and complement traditional funding options with the unsecured and fintech options available to help solve this problem. Having an unsecured finance facility is a great way to fund any gap caused by COVID disruptions.

While large companies can extend their current funding facilities easily and tend to receive more support from larger banks, small and medium-sized exporters and importers often do not have that luxury.

For this reason, we’ve seen an increasing number of these companies approach fintechs and non-bank lenders. Typically, these fintechs and non-bank lenders have a wider view of a company’s operations and consider the company’s business model and cash flow forecasts and can lend without having to take security.

For these companies fintech lenders who can increase their working capital in innovative ways are a vital pathway out of the pandemic.

With an economic reopening expected to be announced in the coming weeks, have you prepared your business for what is to come?

Patrick Idquival is a corporate dealer at Ebury Australia