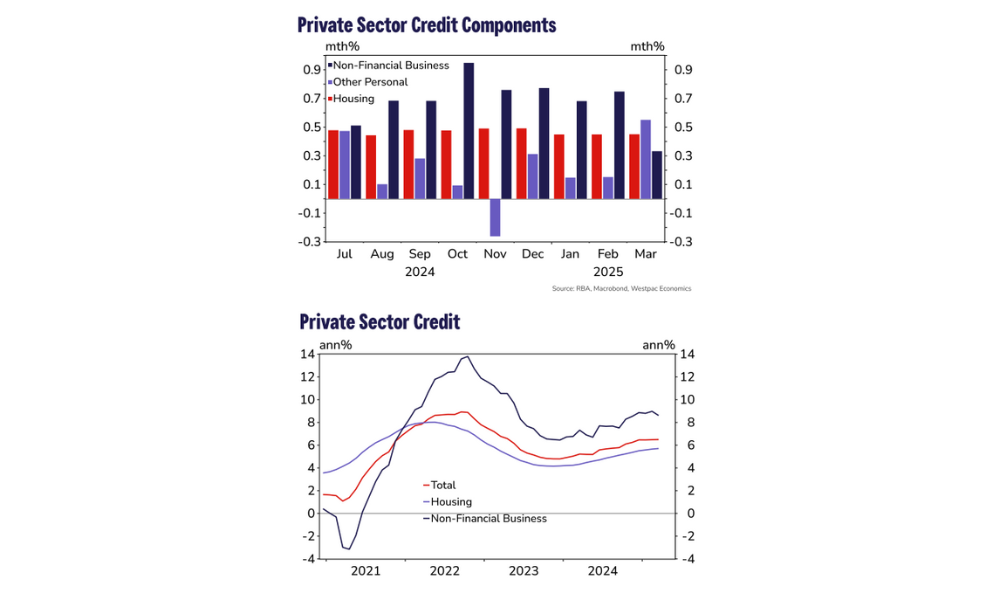

Private sector credit growth in Australia held steady in March, rising 0.5% month-on-month—matching the pace seen in January and February—as early impacts of improved borrowing conditions and the RBA’s February rate cut began filtering through.

However, Westpac warned that downside risks are emerging, particularly in business lending, amid rising global uncertainty.

Westpac senior economist Mantas Vanagas (pictured) said the latest figures are in line with the average monthly growth rate observed across 2024, though early indications of weakening momentum are now appearing.

“Annual growth was also stable, remaining at 6.5%yr for a fourth consecutive month,” Vanagas noted in Westpac’s latest Private Credit Bulletin.

Housing credit, which makes up 63% of total private credit, rose by 0.5% in March. While this appears slightly higher than the 0.4% increase in the first two months of the year, Vanagas noted the month’s underlying pace remained virtually unchanged at 0.45%.

“Both owner-occupier and investor credit achieved exactly the same increases,” he said.

Business credit, accounting for a third of private credit, recorded its weakest monthly growth since October 2023—up just 0.3%. This marks a significant slowdown from the 0.7% to 0.9% range seen in recent months.

“With the US import tariffs and global uncertainty weighing on businesses, and the forthcoming federal election providing additional layer of uncertainty domestically, we expected some moderation in this segment, but the pace was even weaker than what we had pencilled in,” Vanagas said.

Other personal credit, which comprises only 4% of the credit mix, rose by 0.6% in March—one of its largest monthly gains since the Global Financial Crisis. This increase appeared to reflect improved consumer sentiment early in the month.

“Prior to this, sentiment was at its highest level since early 2022, and the notable increase in consumer credit appears to be consistent with somewhat more optimistic mood that month,” Vanagas said. “However, the deterioration seems to have occurred immediately after ‘Liberation Day’ on April 2.”

Vanagas warned that while growth has held up, early signs suggest a shift may be coming.

“To two decimal places, the growth rate in March was close to 0.4%mth, barely rounding up from 0.45%mth, implying that the downside risks we have been highlighting might be starting to materialise,” he said.

Westpac forecasts only a gradual moderation in credit growth, with the annual rate expected to fall below 6% later in 2025. Slower house price growth is also anticipated to weigh on residential credit.

“However, it might be tempered as the RBA continues to ease monetary policy settings, attracting more demand to the housing market,” Vanagas said.

While weaker consumer sentiment could drag credit growth lower in April, Westpac’s Card Tracker data showed little immediate effect from the recent US tariff hikes.

“Consumer reaction to global economic news remains quite uncertain,” Vanagas said.

As for businesses, the outlook remains cautious.

“We doubt that firms will have gained confidence to borrow much more in April and potentially beyond that, until there is more certainty about key global trade policy parameters,” Vanagas said.