New data from the Australian Bureau of Statistics (ABS) revealed that while the number of new home loans declined in late 2024, the average loan size reached record highs, reflecting a market adjusting to sustained high interest rates and a cautious buyer sentiment.

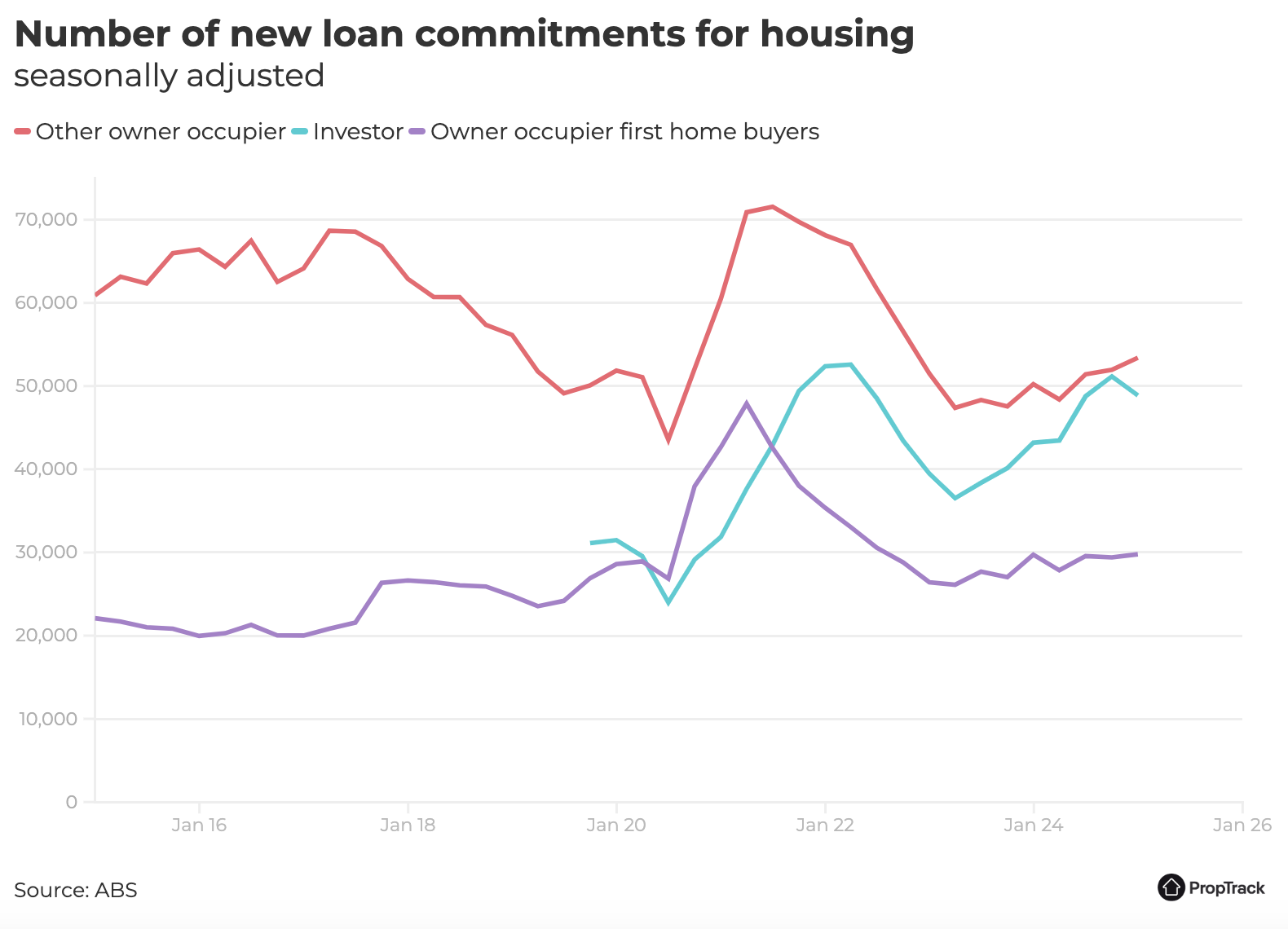

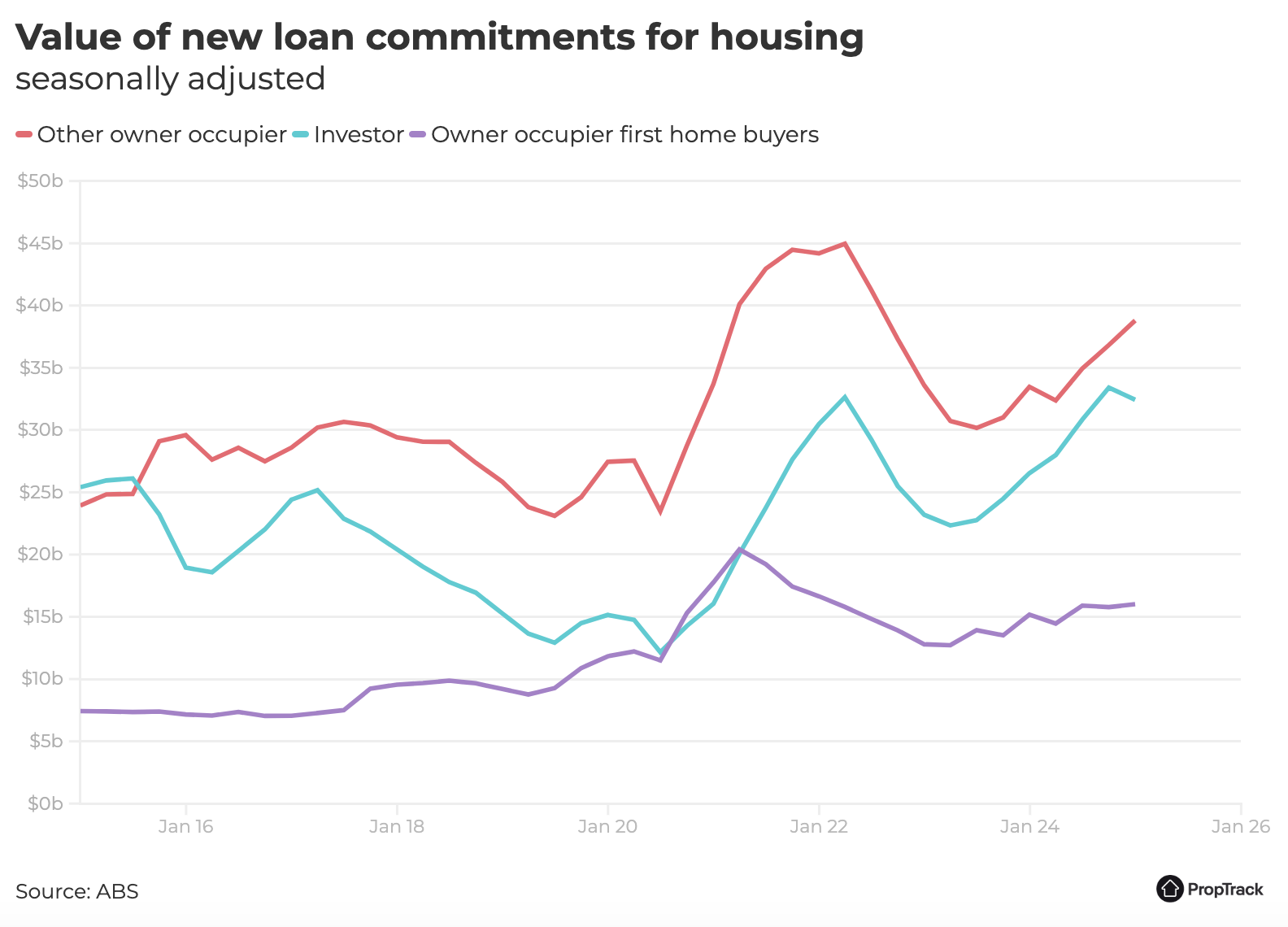

The December quarter saw a 0.4% drop in new loan commitments, yet the total value of housing loans increased by 1.4%. This trend reflects the market’s resilience to affordability pressures, even as home price growth slowed toward the end of the year.

While home prices softened in the last two months of 2024, borrowing activity remained strong on an annual basis, PropTrack reported.

Over the year to December, new loan commitments rose 7.2%, and total lending value climbed 16%, though this was down from 24.7% growth in the previous quarter.

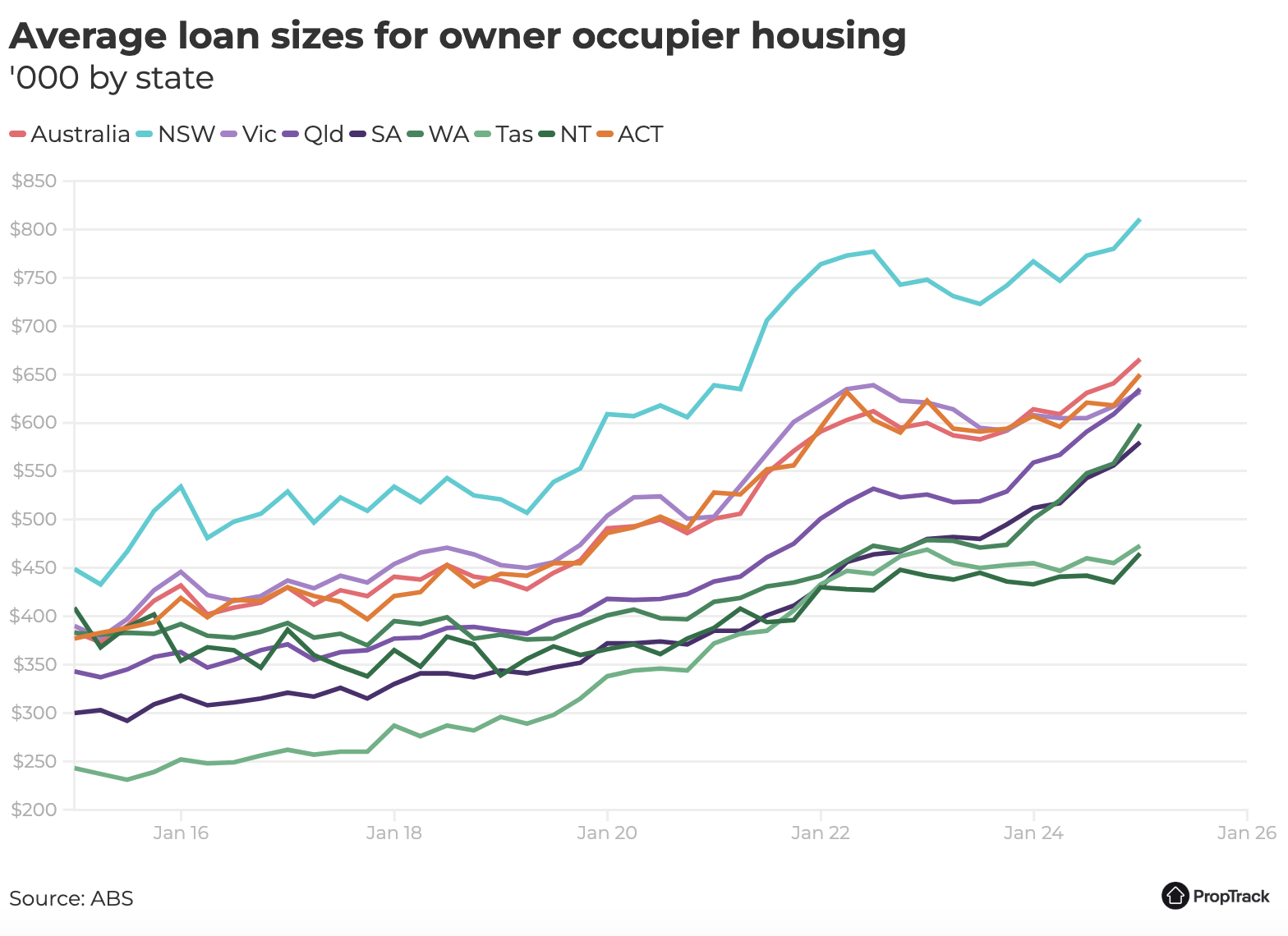

Despite fewer loan approvals, the average mortgage size continued to rise, contributing to the overall increase in lending value.

“More than half of the growth in the value of new lending over the year to December 2024 stemmed from higher average loan sizes,” PropTrack’s Eleanor Creagh (pictured) said.

For the first time in nearly two years, investor lending declined in the December quarter:

Despite this, the average investor loan size reached an all-time high of $674,000, rising $25,000 over the quarter and $49,000 year-on-year.

“The lift in investor activity seen through 2024 has driven this rise, with strong growth in rents and increasing property prices having attracted investors back to the market,” Creagh said.

Even with the quarterly slowdown, investor lending remains 22% higher year-on-year, reflecting strong overall demand in 2024.

The housing market slowdown in late 2024 was influenced by poor affordability, a weaker economy, and persistently high interest rates. However, lower interest rates are now beginning to shift buyer sentiment.

Westpac’s latest consumer sentiment survey showed a 6.5% increase in house price expectations in February, marking the first rise since October.

Auction clearance rates strengthened in every capital city in February, reinforcing signs of renewed confidence among buyers.

“The prospect of rate cuts had already boosted sentiment,” Creagh said.

While buyer confidence is improving, housing affordability remains at its worst level in 30 years, meaning the pace of home price growth may remain muted.

This rate-cutting cycle is expected to be more gradual than in previous years, limiting the speed of home price increases compared to past market recoveries.

“This rate-cutting cycle is expected to be shallow, resulting in the pace of home price growth trailing the strong performance of recent years,” Creagh said.

Despite strong demand, the extent of price recovery in 2025 will depend on economic conditions and affordability constraints.