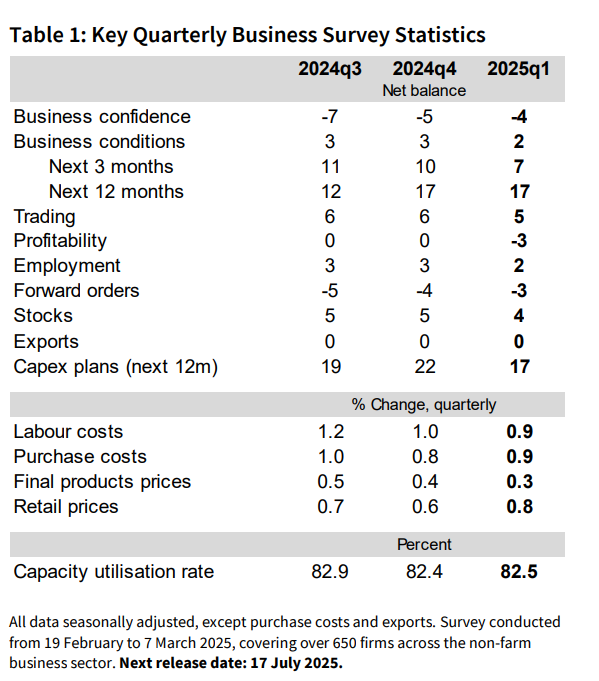

Ahead of the looming federal election, business conditions in Australia softened in the first quarter of 2025, according to the latest NAB Quarterly Business Survey, with all three sub-components — profitability, trading, and employment — experiencing modest declines.

While business confidence saw a slight uptick, it remains negative and well below the long-run average, pointing to continued caution among firms.

The survey was conducted before the April 2 tariff announcement, so the data doesn’t reflect sentiment following that development.

NAB economists Michelle Shi and Gareth Spence (pictured, left to right) reported that overall business conditions fell by one point to +2 index points, marking a broad-based easing across sectors.

“Business conditions eased slightly in the first quarter of the year and are now below average, with declines across all three sub-components,” Shi and Spence said.

The profitability index dropped two points to -3, while trading and employment conditions each fell by 1 point. Industry-specific results showed:

Nationally, business confidence improved one point to -4 index points, with the retail sector showing notable improvement and nearing positive territory. However, business confidence in the mining sector deteriorated significantly.

“Business confidence improved again but remains in negative territory and well below the long run average,” the NAB economists said.

Expectations for the months ahead showed businesses are still hesitant to invest or expand:

“Some forward-looking indicators also weakened: capex plans over the next 12m fell… as did expected business conditions over the next three months,” the NAB economists said. “This suggests that businesses have remained cautious in the first quarter of the year.”

Business conditions declined across most states, with WA down seven points, Queensland down five points, and NSW and SA the only states not to record a decline. In level terms, Victoria and SA remain the weakest performing states.

A shift in reported constraints signals changing priorities for businesses. The share of firms citing labour as a significant constraint fell from 34% to 29% — the lowest since September 2021.

“Labour as a significant constraint on output fell notably… while demand as a significant constraint continued to rise,” the NAB economists said.

Meanwhile, sales constraints increased to 24%, showing demand-side pressures are intensifying.

Quarterly cost metrics suggested slightly easing input pressure:

“Labour cost growth eased this quarter from 1.0% q/q to 0.9%, but there was an uptick in purchase costs growth and retail price growth,” the economists said.

While wage costs continue to top the list of business concerns, their reported impact has been easing over time. In contrast, margin and demand pressures have grown, NAB reported.