As the July 1 deadline for the government's controversial Stage 3 tax cuts approaches, experts have weighed in on how these changes to tax brackets will likely impact the borrowing capacity of some homebuyers.

While concerns about fairness surround the Stage 3 tax cuts, the changes could act as a lever for homeownership for mid-range earners, with some potentially unlocking an extra $100,000 in borrowing power.

“For brokers, it’s an absolute opportunity, particularly with existing clients who may have been with their mortgage provider for over two years and now may be on an uncompetitive interest rate,” said tax expert Ryan Watson (pictured above centre), director of Tribeca Financial.

“The greater flexibility around borrowing capacity will give them the ability to shop the home loan around in the market and potentially save thousands of dollars per annum in home loan interest.”

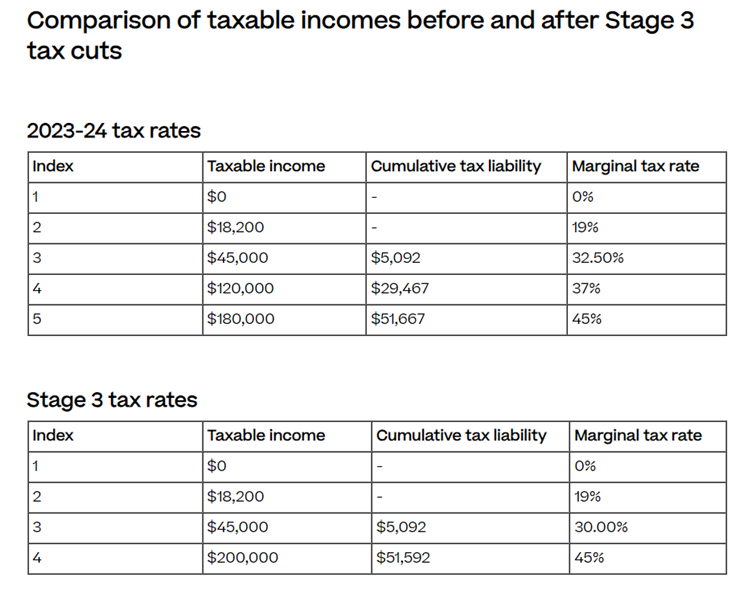

The Stage 3 tax cuts are the final part of a three-phased tax reform plan legislated in 2019 and are set to come into effect for the 2024/25 income year.

It involves changes to personal income tax brackets, primarily affecting earners between $45,000 and $200,000.

There will be two key changes:

Source: The Tax Institute

On January 15, Prime Minister Anthony Albanese said the Stage 3 tax cuts were here to stay despite Labor’s consistent reservations, according to the Australian Associated Press.

Since then, the conversation has swirled about the fairness of the Stage 3 tax cuts, which is set to cost the government $313 billion over 10 years.

By January 22, one media outlet had claimed that the tax cuts were not going ahead as planned – although at the time of writing, there has been no changes to the Stage 3 tax cuts.

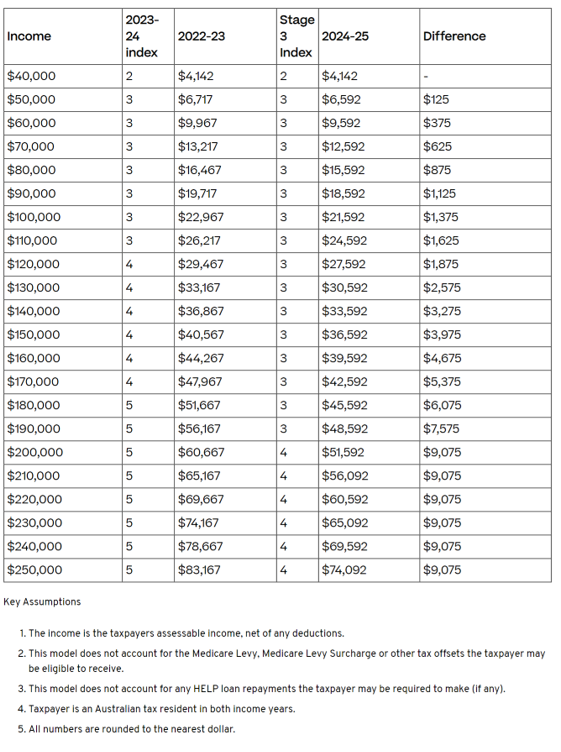

With the $1,500 tax offset ending this financial year, many workers that earn under the Australian average annual salary of $90,000 will be worse off in net terms despite the tax break.

In a cost-of-living crisis, the fact that someone earning $200,000 receives a $9,075 tax break while someone earning $40,000 gets no immediate benefit can feel unfair.

Others have made the case that the tax overhaul could save $130 billion off the total bill if it were reweighted towards lower income earners.

However, the reason Australia's middle- and higher-income earners are set to receive the major tax breaks is because they bear the larger share of the tax burden, according to property expert Ben Kingsley (pictured above left).

“And so they should, but how much is too much?” said Kingsley, founder and director of Empower Wealth, which was recently named Liberty Australian Brokerage of the Year at the 2023 Australian Mortgage Awards.

“Squaring up the ledger a bit whilst also addressing bracket creep is a fairer outcome.”

For example, Kingsley said someone earning $70,000, currently paid $13,217 in taxes. Now double their income to $140,000. Their tax bill jumps to $36,867 – that’s 179% more than the lower earner, not just double.

With the new Stage 3 cuts, that number falls to 166% higher – ($12,592 compared to $33,592).

Watson agreed, “I think for most Australians, the tax cuts have been enacted to provide improved equality for everyday Australians, particularly for ‘middle Australia’ who do a lot of our country’s heavy lifting.”

Source: The Tax Institute

Another crucial question concerns the overall economic impact of the Stage 3 tax cuts. While hindsight allows for perfect clarity, Australia's economy has faced unique challenges in the six years since the tax cuts were conceived.

With the economy slowing up thanks to Reserve Bank of Australia’s (RBA) hawkish approach to curb inflation, which resulted in 13 hikes to the cash rate in two years, Kingsley said the tax cuts would “give a boost to spending”.

“This is good for business and employment,” Kingsley said. “That said, it does put upward pressure of rates staying higher for longer if we haven’t seen a further slowdown in the economy before they arrive.”

This upwards pressure could get worse, according to economist Chris Richardson, if inflation ticks back up.

Richardson said the Stage 3 tax cuts could be the equivalent of a cash rate cut between 0.50% t0 0.75% – which could delay any further rate relief from the RBA.

“If inflation proves more of a challenge than expected, then the Reserve Bank would have to scramble to make up lost ground,” Richardson said in the LinkedIn post shown below.

“I don’t forecast that will happen. But it could: inflation could turn out to be stronger and stickier than the RBA expects.”

Watson agreed.

“By decreasing our rate of tax payable, it will invariably put more money into the economy. Whether that be through everyday spending, to the purchasing of new family homes,” Watson said. “It will certainly create a stimulus in the Australian economy.”

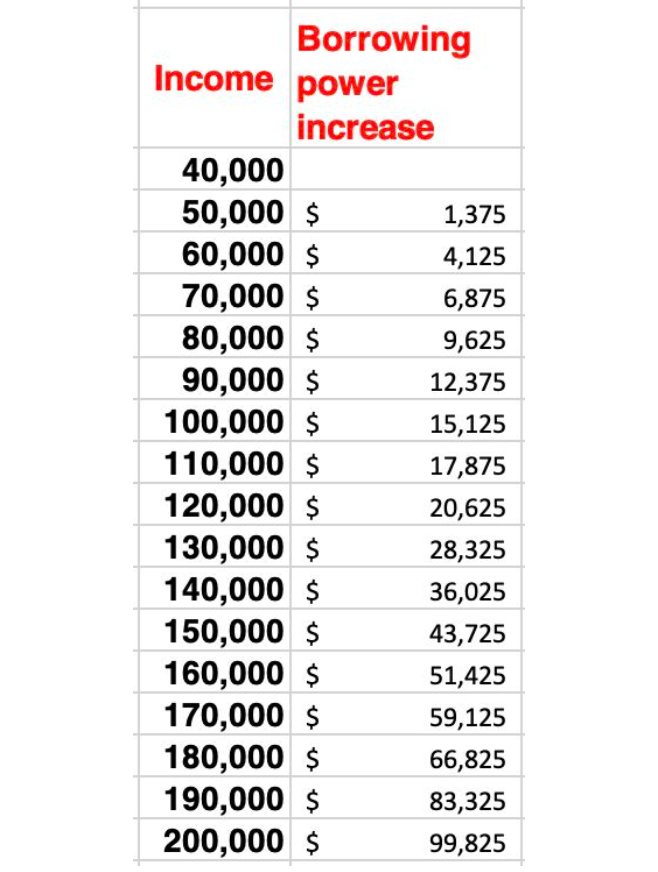

In terms of borrowing capacity, prospective homebuyers will likely be the ones to benefit the most.

Borrowing power could increase by $15,000 for someone with $100,000 annual income and around $100,000 for someone on a $200,000 income – and that’s assuming APRA still leaves the buffer rate at 3% on lending servicing.

For mortgage broker Redom Syed (pictured above right), director of Confidence Finance, the tax cuts are exciting news, as high-income households could increase their borrowing power by up to $200,000.

“Borrowing powers are based on your net income,” Syed said. “Banks subtract your expenses, and then lend to you based on your leftover income available. These tax cuts directly increase the leftover income. The higher your income, the larger the boost to your borrowing power is.”

“For the rare households with two income earners above $200,000, there's potentially a $200,000 increase coming your way.”

So how should mortgage brokers approach the tax cuts with their clients? No different than usual, according to Kingsley.

“They should be doing as a professional advisor with an obligation to responsible lending. So even if there is a spike in borrowing power, each customer should still be treated on their merits,” Kingsley said. “They should borrow what they feel comfortable in being able to repay today, but also tomorrow if circumstance change.”

“For those professional brokers who build real relationships with their clients, they should be talking to them about trying to be saving this extra money to either park in the offset or pay down their principal mortgage.”

For borrowers, Syed said there are two quick tips they might want to follow when thinking about rates:

“Quick tip: Multiply your yearly tax cut benefit by 10 for a quick estimate of your borrowing power boost,” Syed said. “And if you’re struggling to refinance or buy today, ask your broker the question - what does it all look like in July?”