A wave of new property listings swept across Australian capital cities in March as homeowners looked to capitalise on improved market conditions following the Reserve Bank’s February interest rate cut, Mortgage Choice reported.

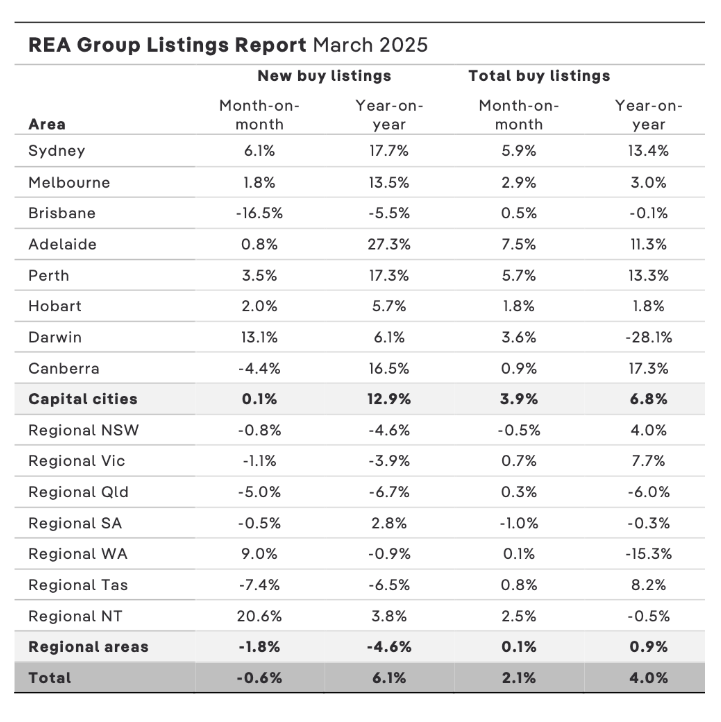

According to the latest REA Group Listings Report, new property listings were up 6.1% nationally year-on-year.

Capital cities led the rise, with significant year-on-year increases in Adelaide (up 27.3%), Sydney (up 17.7%), Perth (up 17.3%), Canberra (up 16.5%), and Melbourne (up 13.5%).

Brisbane was the only capital to see a decline, with new listings falling 5.5%, likely due to recent cyclone disruptions.

“Both Sydney and Melbourne have seen a run of strong activity in 2025 so far, suggesting continued vendor confidence amid rising home prices and falling mortgage rates,” said Angus Moore (pictured upper left), REA Group executive manager of economics.

Regional markets didn’t mirror the surge seen in capitals, with new property listings down 4.6% compared to March 2024.

“The strong growth compared to a year ago partly reflects that Easter fell in March in 2024, while it will fall in April this year,” Moore said. “This would have subdued housing market activity at the back end of March last year.”

The boost in property listings has translated into greater choice for home buyers, with total listings up 6.8% in capital cities and 4% nationally.

Canberra led the rise in total listings (up 17.3%), followed by Sydney (up 13.4%), Perth (up 13.3%), and Adelaide (up 11.3%). Listings in Melbourne rose 3%, Hobart was up 1.8%, Brisbane remained flat, and Darwin saw a sharp 28.1% year-on-year decline.

“It does help with transaction confidence in terms of people wanting to buy because rates are going to be lower not higher,” Real estate agent Dib Chidiac from Sydney's inner west told Mortgage Choice. “Those that sell assume people will pay a better price.”

Chidiac noted that while buyers have more options now than last year, April’s public holidays and the upcoming federal election have caused a short-term dip in listings.

“From May 3rd onwards we’re going to see a bit more stock, and hopefully with interest rate cuts a bit more activity,” he said.

RBA’s 25 basis point rate cut in February — the first since 2020 — brought the official cash rate down to 4.1%. The move came after inflation data showed a return to the RBA’s 2–3% target band. RBA left the cash rate steady at 4.1% during its most recent meeting, opting to wait for more data before deciding on further action.

“Rate cuts tend to support confidence, though of course the broader environment in which those rate cuts are happening matters as well,” Moore said. “But all else equal, lower rates will support home prices and housing market conditions.”

Westpac’s March consumer data showed increased home buyer sentiment, with its “time to buy a dwelling” index hitting its highest level since September 2021. However, sentiment dipped again in April due to global uncertainties, including tariff tensions and share market volatility.

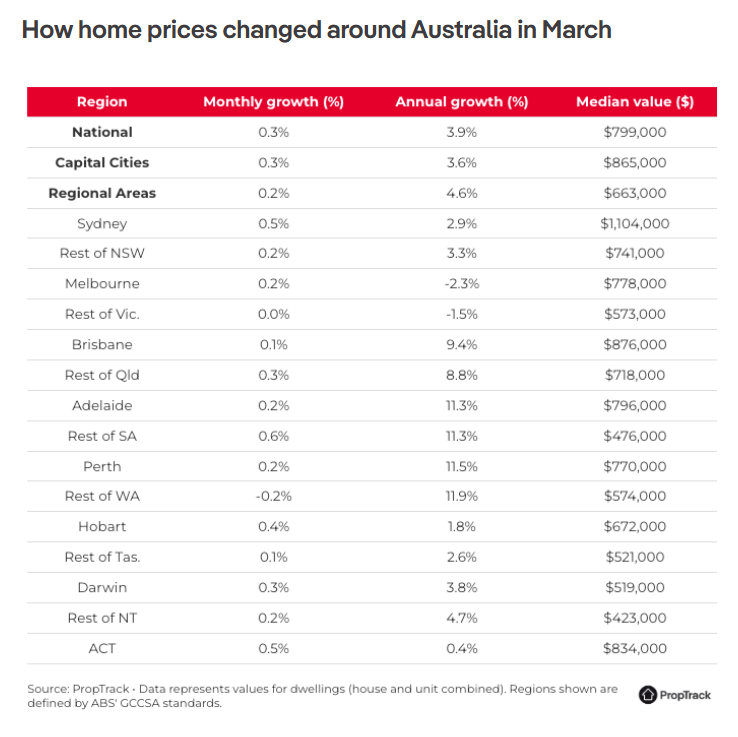

The PropTrack Home Price Index reported a 0.3% national rise in property prices in March, continuing the upward momentum from February. Sydney and Canberra led growth among capitals, both up 0.5%.

Among property types, Melbourne units recorded the largest gain at 1%, while Canberra houses rose the most at 0.7%.

“We expect prices to keep lifting over the coming months, but the rate of growth is likely to be more modest compared to recent years,” said REA Group senior economist Eleanor Creagh (pictured upper right).

Economists expect the RBA to cut rates again when it meets in May, particularly if inflation continues to slow.

“Westpac expects the deteriorating external situation, which has had a clear bearing on this month’s weaker sentiment read, and further evidence of a sustained slowing in inflation will see the board deliver a further 25 basis point rate cut at its May meeting,” said Westpac’s Matthew Hassan (pictured lower left).

All four major banks anticipate more cuts, with NAB forecasting a potential 50 basis point reduction in May. NAB and ANZ expect additional 25 basis point cuts through July, August, and November. CBA also predicts cuts in May, August, and November, while another is expected in early 2026.

RBA will have access to key inflation, wages, and employment data ahead of its May meeting, as well as updated economic forecasts and insights into global trade developments.

“We think the distribution of risks to both growth and inflation in Australia have shifted such that the central bank is required to act with some sense of urgency,” said NAB Group chief economist Sally Auld (pictured lower right).