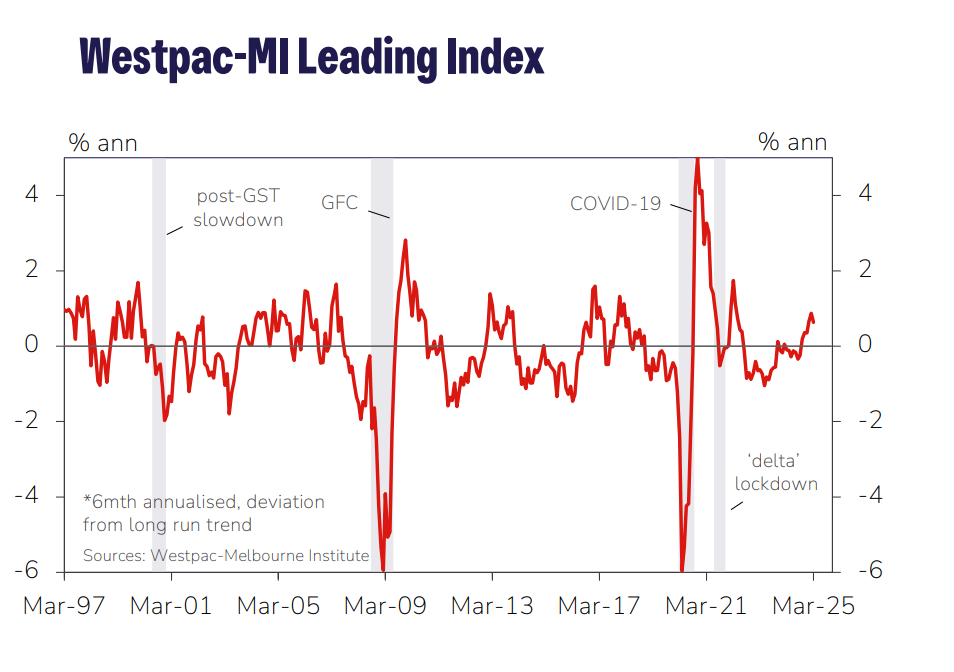

Australia’s near-term economic prospects are beginning to show strain, with the Westpac–Melbourne Institute Leading Index slowing to an annualised growth rate of 0.6% in March, down from 0.9% in February.

The index, which forecasts economic activity over a three to nine-month horizon, still signals above-trend momentum—but the latest data marks a clear deceleration.

“The index is only just starting to capture the effects from the trade policy disruptions that escalated sharply following US President Trump’s ‘reciprocal’ tariff announcement on April 2,” said Matthew Hassan (pictured), head of Australian macro-forecasting at Westpac.

“The situation is uncertain and there are other factors at play but some further softening in the growth pulse looks likely in the months ahead.”

On April 2, Trump announced sweeping reciprocal tariffs of up to 25% on key imports from several major trading partners, sparking swift retaliatory measures and renewed global trade tensions.

Just a week later, he paused all tariffs (except the 10% base) for 90 days, excluding China, which now faces a 145% tariff. US exports to China face 125% in return. Electronics like smartphones and semiconductors were later exempted, underscoring the policy’s unpredictability.

Despite the March reading being positive, it represents the first visible signs of pressure stemming from global tariff developments.

According to Westpac, the impact on the Australian economy remains “relatively small and manageable” for now, though the bank has revised its 2025 growth forecast down to 1.9%, from 2.2% previously.

“Risks are to the downside,” Hassan said.

The modest slowdown so far has been largely attributed to shifts in financial markets and confidence.

Since September last year, the index has risen from –0.24% to +0.63%, with commodity prices and a widening yield spread accounting for the bulk of the gain.

Improvements in US industrial production and Australian job sentiment also contributed positively.

Commodity price strength has come mostly from the falling Australian dollar, which dropped 6.5¢ against the US dollar between September and March.

Although the dollar has since rebounded slightly, “remarkably, despite being down another 3.5¢ at one stage, the Australian dollar is now slightly above its March-end level.”

Equity markets and consumer sentiment have recently turned negative, dragging the Index down. The S&P/ASX200 has subtracted 0.18 percentage points, while weakening job sentiment has chipped off another 0.1ppt since September.

The outlook remains fragile. The post-tariff-announcement market plunge has not fully reversed, and consumer sentiment has taken a hit, especially during the survey week that captured responses in the wake of the tariff shock.

With inflation cooling and external risks rising, Westpac anticipates action from the Reserve Bank.

“Westpac expects the deteriorating external situation, signs that this is starting to weigh on sentiment locally and more evidence of a sustained slowing in inflation will see the board deliver a further 25bp rate cut at its May meeting,” Hassan said.

“Indeed, given the scale of the tariff shock unfolding abroad the board is likely to signal a clearer shift in focus away from lingering questions about inflation to downside risks to growth.”

This sets the stage for further policy easing in the latter half of 2025.