Capital city home prices are forecast to end 2026 essentially unchanged from where they started, before returning to growth in 2027, according to the realestate.com.au Property Market Outlook.

The REA Group economics team attributes the flat outlook to the compounding effect of three consecutive RBA rate hikes, the federal budget's changes to negative gearing and capital gains tax, and housing affordability that was already strained before rates began rising again this year.

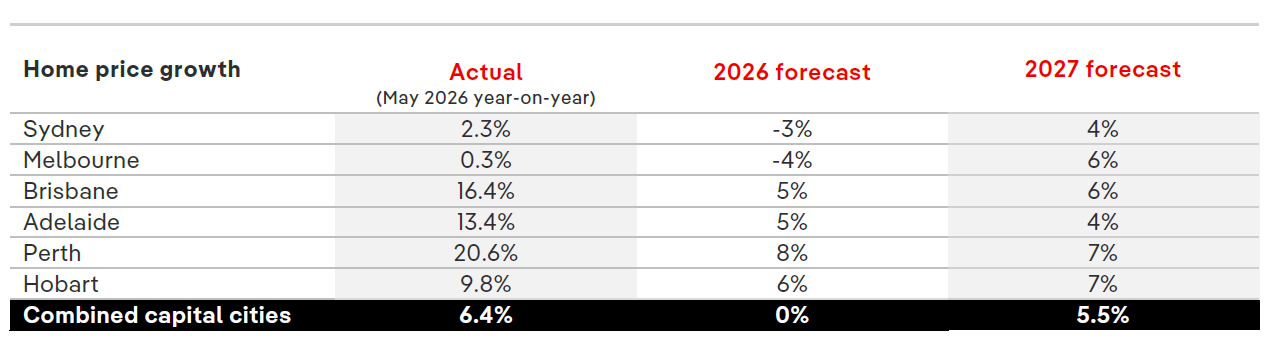

"Home price growth has clearly slowed, and market conditions cooled, following the three consecutive rate hikes from the RBA," the report states. "Home prices in Sydney and Melbourne have declined for three consecutive months, and home prices nationally have stalled."

Softness across the combined capitals is expected to persist through much of 2026 as the effect of higher rates flows through and tax changes weigh on investor demand, before a turning point emerges late in the year and into 2027. With the combined capitals forecast at 0% for the year, the margin for error on valuation-based lending decisions is narrower than it has been in recent years.

The city-by-city picture is where the detail matters most for brokers. The full forecast is set out below.

The two largest capitals are expected to finish 2026 in negative territory — Sydney down 3% from its January level, Melbourne down 4%. Both cities recorded new listing volumes up 6–7% annually over the first five months of 2026, giving buyers more choice and contributing to softer clearance rates. Neither city is expected to recover strongly in 2027, with Sydney forecast at 4% and Melbourne at 6% — both below the typical annual average of around 7%, reflecting the ongoing drag from high interest rates and stretched affordability.

Those conditions are concentrated in Sydney and Melbourne — elsewhere, the picture looks markedly different.

Perth is tipped to be the standout performer, finishing 2026 up 8% and 2027 up a further 7%, underpinned by strong wages growth from mining activity and ongoing population inflows.

Hobart is forecast to gain 6% in 2026 and 7% in 2027, supported by first-home buyer activity and a constrained supply pipeline. Brisbane and Adelaide are both expected to grow 5% in 2026, with Brisbane carrying stronger momentum into 2027 at 6% — backed by the second-largest gap between housing supply and population growth among Australia's five largest cities.

Adelaide's 2027 forecast is more modest at 4%, as affordability constraints — the state is now the second-least-affordable in the country — begin to slow the pace of growth.

The RBA's June decision supports the baseline assumption of broadly stable rates through the second half of 2026. The RBA held the cash rate at 4.35% at its June meeting — unanimously, with no rate cut discussed — noting financial conditions have tightened and the economy is slowing. Further hikes remain possible if inflation persists, with market pricing implying roughly a fifty-fifty chance of one more move by December.

Roy Morgan data projects 29.8% of mortgage holders — around 1,552,000 people — are now at risk of mortgage stress in May, following the RBA's third consecutive hike.

Beyond rates, the federal budget adds a further layer of uncertainty for investor clients.

"Tax changes in the federal budget will weigh on investor demand, which has been a significant factor affecting housing markets in recent years," the report notes. "While estimates suggest the effect on home prices from these changes will probably be modest in the long run, the short-run effect is to reduce price growth by a couple [sic] percentage points in 2026 and 2027."

Population growth, rising incomes, and the expanded 5% deposit guarantee are all cited as demand-side supports.

On the supply side, however, new housing completions remain well below what rising approvals and commencement figures might suggest — and with rates at their highest level since 2011, new commencements may slow further, tightening supply precisely when affordability is already under pressure. That constrained pipeline is expected to place a floor under prices nationally even through the softer phase of the cycle.

Get the hottest and freshest property and mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.