Australian lenders are adjusting home loan rates ahead of a widely expected official cash rate drop.

According to Canstar, a growing number of banks are adjusting both fixed and variable rates as competition for mortgage customers heats up.

The moves come as property prices are forecast to rise further amid strong company earnings and a rebound in mortgage growth.

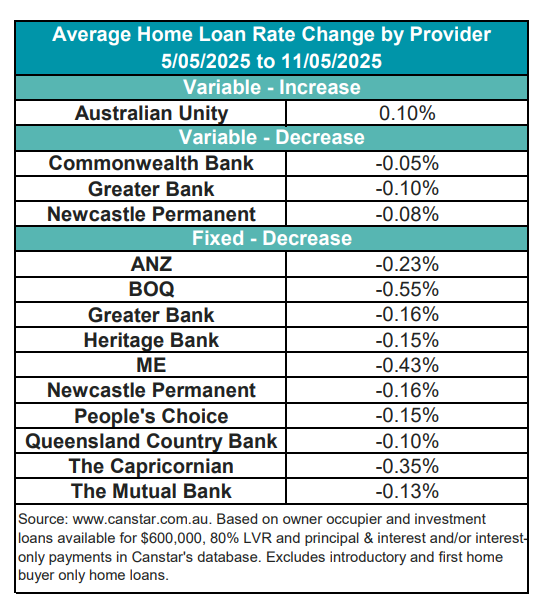

In a sign of what's to come, multiple lenders made notable changes to home loan rates last week.

“Ten lenders have cut fixed rates in the last week as banks continue to price in the possibility of a rate cut as soon as next Tuesday,” said Sally Tindall (pictured), Canstar insights director.

The list includes ANZ, which last Friday dropped its lowest fixed rates down to a relatively competitive 5.39%.

ANZ now offers the lowest one- and two-year fixed rates among the major banks, although Tindall noted that smaller lenders like BOQ and Police Bank have already introduced fixed rates starting with a “4,” undercutting the majors and intensifying the competition.

While fixed rates often shift first, some variable rates are also beginning to drop. Canstar reported that three lenders cut 12 variable rates last week by an average of 0.08%, while Australian Unity increased one rate by 0.1%.

“What is perhaps more interesting is the fact that some variable rates are now also coming down,” Tindall said.

“While there’s a wide range of factors that influence both fixed and variable rates, both the expectation of a falling cash rate and feisty competition between lenders appear to be dominant right now.”

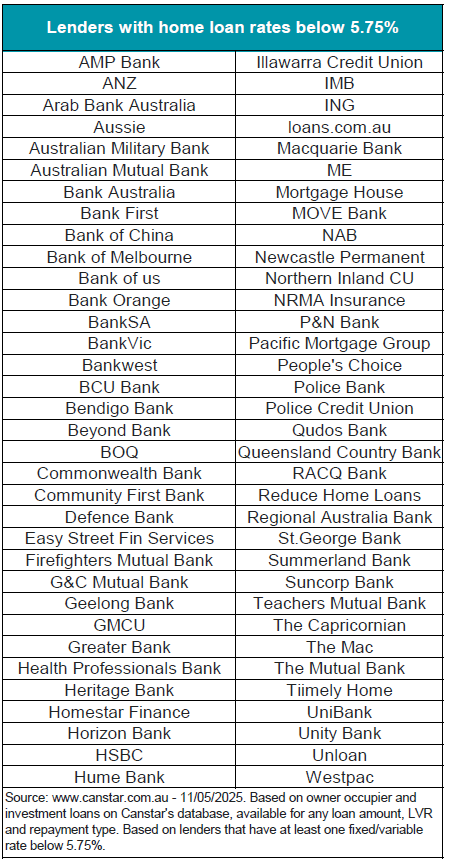

Canstar’s database now shows 773 home loan rates below 5.75%, up from 654 just a week earlier—evidence that lender competition is accelerating. See the table below for a list of lenders offering these rates.

EMBED IMAGE: 05 13 Lenders with rates below 5.75%

To compare with the previous week’s rate changes, check out this link.

Last week, CBA cut its lowest advertised variable rate to 5.84%, bringing it in line with Westpac and ANZ.

“Last Wednesday, CBA cut its lowest advertised variable rate down to 5.84% in a sign the bank is strategically finding its place on the start line for when the RBA fires off the next cash rate cut,” Tindall said.

“There’s little coincidence CBA’s variable rate now matches Westpac and ANZ’s. The big banks are fierce competitors when it comes to the fight for market share.”

With competition growing and rate cuts anticipated, borrowers may have more negotiating power than they realise.

“All of this rate movement is fantastic for consumers but only if they use this competition to their advantage,” Tindall said.

“Borrowers should use the next week to take stock of their interest rate and work out where it sits in the pack before a potential cash rate cut, and if need be, pick up the phone and haggle with their bank for a lower rate.”

While most banks are expected to pass on a full rate cut when the RBA moves, Tindall said that “the reductions we’ve seen outside of the central bank’s decisions are typically only reserved for new customers or those prepared to lock in their rate.”

Tindall encourages borrowers to act now rather than wait for official changes.

“Yes, borrowers could well be getting rate relief in a matter of weeks, but why not secure a cut now, and another one if and when the RBA does decide to fire off that next cash rate cut? When it comes to the mortgage, two cuts is typically better than one,” she said.