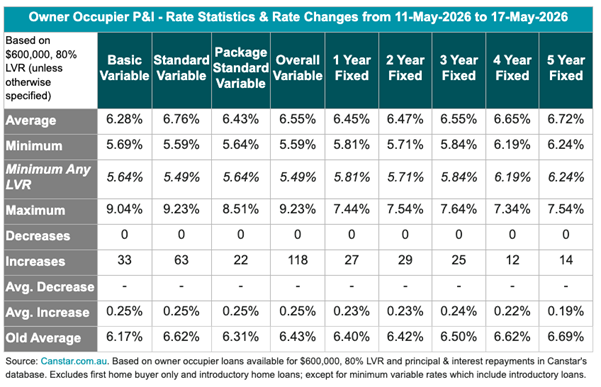

All four major Australian banks were among 41 lenders on the Canstar database to raise variable home loan rates in the week ending May 17, as the average variable rate for owner-occupiers climbed to 6.55%, up from 6.43% the previous week.

According to data published by financial comparison site Canstar, the 41 lenders lifted 406 owner-occupier and investor variable rates by an average of 0.25% during the period. A further 20 lenders increased 331 fixed rates by an average of 0.23%. The only cut recorded came from Bank of China, which reduced its three-year investor fixed rate for interest-only repayments by 0.10%.

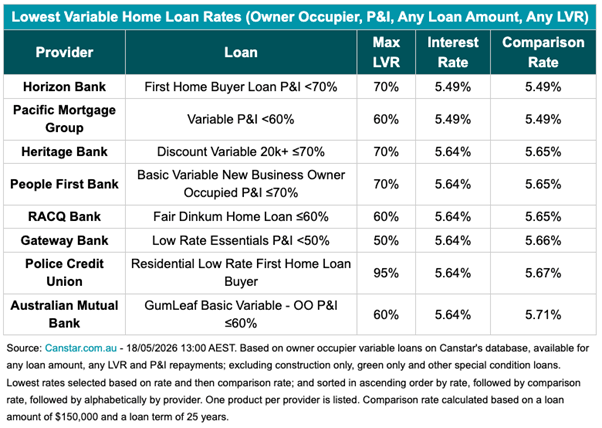

The lowest variable rate on Canstar's database remained at 5.49%, offered by Pacific Mortgage Group and – for first home buyers specifically – by Horizon Bank. The number of rates below 5.75% dropped sharply, falling from 82 to 49 in a single week.

Canstar data insights director Sally Tindall said the scale of the latest round of hikes would be felt immediately by borrowers, even if higher repayments had not yet appeared in their bank statements.

"Forty-one lenders on the Canstar database hiked variable rates in the past week including all four big banks. This means their millions of customers are now being charged more every time their lender calculates the interest they owe on their home loan, something they do every day," Tindall said.

"The extra money, however, takes a lot longer to come out of customers' bank accounts. Many lenders are still yet to increase their customers' monthly repayments as a result of the March hike, let alone the May one."

Tindall flagged that the pipeline of rate pressure showed little sign of easing, pointing to simultaneous movements in both fixed mortgage rates and term deposits as an indicator of where the Reserve Bank of Australia cash rate could be headed. The dynamic mirrors trends Australian Broker has been tracking throughout 2026, with fuel costs and successive rate rises keeping household sentiment near historic lows.

"Looking ahead, there's little sign the cash rate hikes will slow down. In the last seven days, we've had 20 lenders increase their fixed mortgage rates, while at the other end of the scale, 18 banks have hiked term deposits. Not a good omen for future RBA cash rate decisions," she said.

"It's also a difficult pill to swallow for borrowers looking for a rate under 6% to fix. There are just eight lenders still offering a fixed rate that starts with a 5 on our database, and none of these are likely to hang around for long. On the flip side, it is good for anyone looking to lock up their cash, with a small handful of options now above 5.50%."

Tindall also weighed in on the latest Australian Bureau of Statistics lending indicator data, noting that while headline figures pointed to a cooling property market, the broader context told a different story.

"What the ABS data shows is that the property market is slowing on the back of the RBA rate hikes, with a drop in both the total value of new loans committed to and the average new loan size for owner-occupiers," she said.

"But take a step back – just one – that's all that's needed, and the bigger story is clear: because this quarter's drops have edged down from pretty ridiculous peaks. The average new mortgage size? At $735,000 nationally, we're looking at the second-highest figure on record. The surge in buyer activity? Investors, up 25% from the same time a year ago."

Despite the cooling signals, demand for mortgage broker expertise remains robust. Research from early 2026 found that trust in brokers remains high and loyalty stable, with roughly three in four recent clients saying they would use the same broker again – a strong position as borrowers navigate an increasingly complex rate environment.

For brokers, the data reinforces the value of proactive client communication. Mortgage demand rose 13.3% year-on-year in October 2025, driven in part by rate cuts earlier that year – a reminder that shifts in the rate cycle, in either direction, can move borrower behaviour quickly.