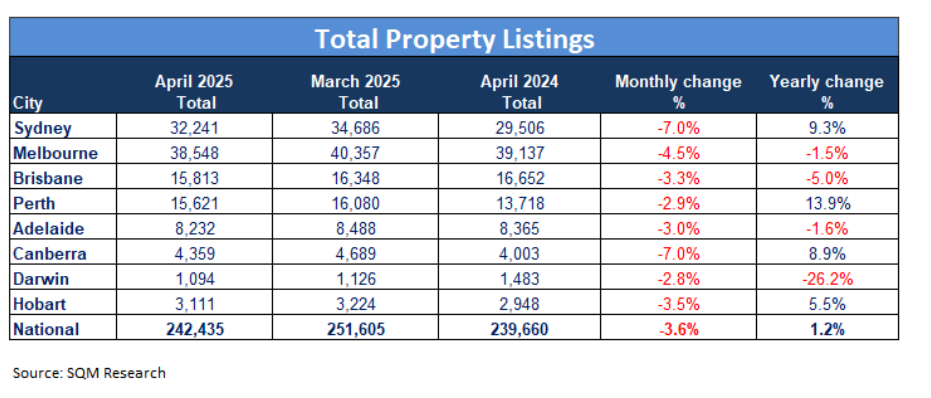

Total residential property listings across Australia fell by 3.6% in April 2025, dropping to 242,435 properties, according to the latest data from SQM Research.

Every major city saw a monthly decline, with Sydney and Canberra both experiencing the sharpest fall at 7%. Melbourne saw a 4.5% month-on-month decrease, with listings dipping to 38,548—down 1.5% compared to April 2024.

Brisbane’s listings declined by 3.3% over the month and 5% annually. Perth’s 2.9% monthly fall left listings at 15,621 dwellings, though this was still 13.9% higher than the same time last year.

Despite the decline in listings, persistently low housing supply and strong population growth continue to fuel demand, keeping upward pressure on prices.

Fresh property listings—defined as properties listed for less than 30 days—fell significantly in April, declining by 11.6% to 66,232 nationwide. Compared to April 2024, this marks a 1% decrease.

SQM Research attributed the dip to external events.

“New listings in April were heavily impacted by the federal election as well as the Easter/Anzac Day holidays, so it’s a little more difficult to read much into April’s results,” said Louis Christopher (pictured), managing director of SQM Research.

City-level data showed sharp declines in new listings: Darwin (–36.7%), Canberra (–25.1%), and Sydney (–23.6%) were hardest hit.

Melbourne dropped 14.7% month-on-month and 4.4% year-on-year. Perth saw an 8.1% decline but remained up 10.9% compared to last year. Adelaide and Brisbane recorded monthly declines of 9% and 6.1% respectively. Hobart dropped 16% in April but posted a 6.6% year-on-year gain.

Older property listings—defined as properties on the market for over 180 days—rose nationally by 1.6% to 76,067 in April, a 10.6% increase over the year.

Sydney saw a 3% monthly rise and a 27.9% year-on-year surge in older listings. Melbourne matched Sydney’s monthly rise at 3.2%, with a 15.6% annual increase. Canberra and Hobart also experienced notable yearly increases at 60.1% and 30.4% respectively.

“The older listings continued to trend up, especially in our largest cities of Sydney and Melbourne,” Christopher said. “This is one indicator that suggests a softer Sydney and Melbourne market where vendors are still struggling to sell if they don’t meet the market.”

In contrast, Darwin was the only city to record a monthly decrease (–1.8%) in older listings, with a 14.1% annual drop.

Distressed property listings declined by 3.5% in April to 4,796 properties nationwide, with year-on-year figures down 8.8%. NSW led the monthly fall with a 9.7% drop, while VIC fell 1.7% but rose 9.3% over the year.

The ACT recorded the most significant monthly drop (–32.4%), though listings remained 4.2% higher than in April 2024. QLD saw a modest 0.3% rise but maintained a 19.6% yearly decline. WA and SA posted respective monthly falls of 1.9% and 0.8%.

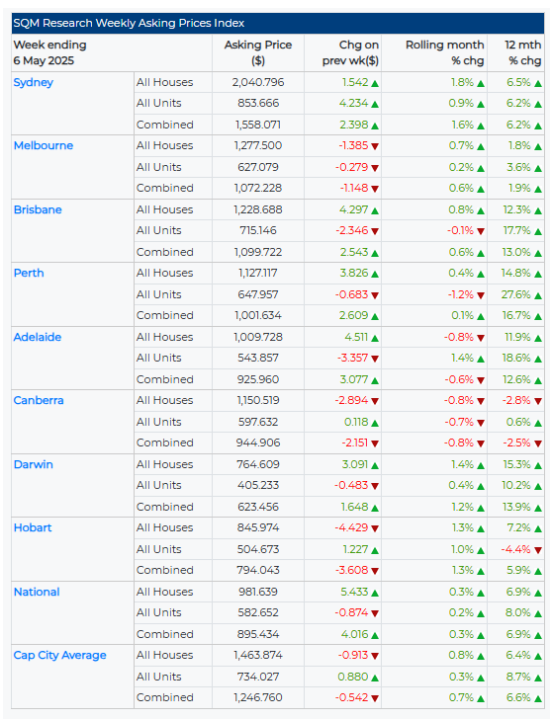

Nationally, asking prices rose by 0.3% in April, with house prices up 0.3% and unit prices up 0.2%. Among the capitals, combined asking prices increased by 0.7%, supported by a 0.8% rise in houses and 0.3% in units.

Sydney led the market with a 1.8% increase in house prices and a 0.9% gain in unit prices, resulting in a combined 1.6% rise. Hobart followed with a 1.3% uptick in both house and unit prices. Darwin saw a combined 1.2% increase, while Melbourne rose by 0.6%.

Brisbane recorded a 0.8% increase in house prices but a 0.1% dip in units, leading to a combined 0.6% gain. Perth posted a modest 0.1% rise, with house prices climbing 0.4% and unit prices falling 1.2%.

In contrast, Canberra experienced a 0.8% decline across both house and unit prices, while Adelaide saw a mixed trend—house prices dipped 0.8%, but unit prices rose 1.4%, resulting in a 0.6% fall overall.

Looking ahead, SQM Research anticipates a surge in listings and market activity following the resolution of political uncertainty.

“Going forward, with the election behind us and a majority government in place, I expect a large uplift in new listings for May as well as a pick-up in auction clearance rates,” Christopher said. “As for prices, we are expecting participant confidence to lift now that we’re past the election period and coming up to another interest rate cut.”