More prevalent discounting by the banks continues to bolster the difference in rates between new and existing borrowers, according to estimates from the Australian Securities and Investments Commission (ASIC).

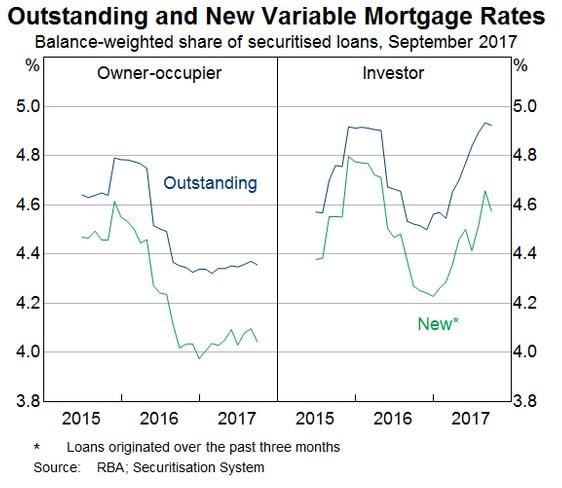

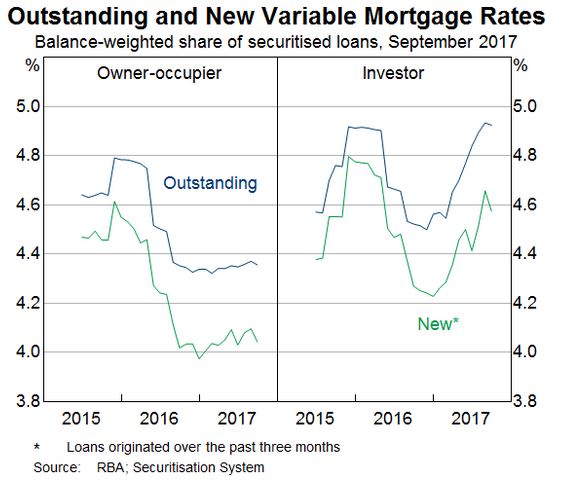

While the average interest rate for new loans has been consistently lower than that of outstanding mortgages for the past few years, the degree of discounting has increased over the past 12 months, Marion Kohler, head of ASIC’s domestic markers department, said at the Australian Securitisation Forum last Monday (20 November).

“The increase in interest rate discounts offered to new borrowers over the past year suggests that competition for customers is stronger for new borrowers than for existing borrowers.”

The Reserve Bank of Australia (RBA) has already noted this apparent difference in its latest submission to the Productivity Commission’s Inquiry into Competition in the Financial System.

“Since 2010 the average discount for all loans from a standard variable interest rate on a principal-and-interest loan for an owner-occupier has increased from around 60 basis points to around 90 basis points,” the RBA submission said.

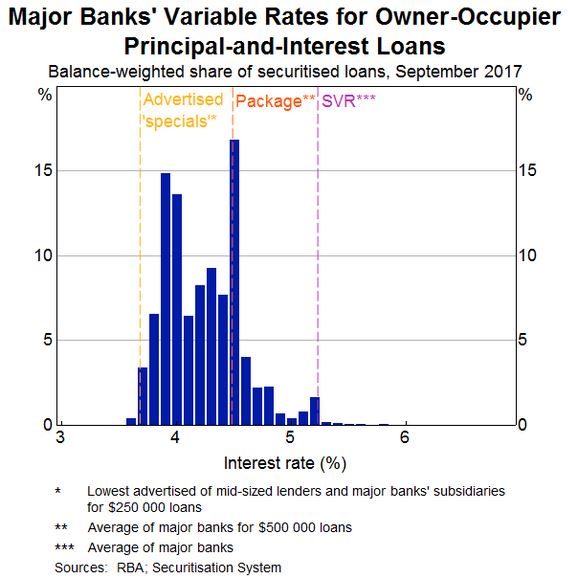

Kohler touched upon the discrepancy between the advertised standard variable rate (SVR) and what borrowers actually pay, saying that “very few” borrowers actually pay the stated SVR. The discounted rate offered is typically the package rate for mortgage products with additional features such as offset accounts or separately advertised ‘specials’ rates.

“Only a small share of loans in the dataset has an interest rate consistent with this lowest advertised rate. This may be because not many borrowers either qualify or seek loans at the advertised specials rate,” she said.

Another reason may be that advertised specials are rates for new loans which attract larger discounts than existing borrowers.

ASIC’s current estimates come from its Securitisation Dataset which examines detailed data of any mortgages underlying residential mortgage-backed securities (RMBS).

Related stories:

Have banks let down the community?

Government floats higher ACL fees

Capital cities boast spectrum of housing costs