Australia’s small business ombudsman is calling for a federal government-backed loan scheme to help SMEs survive the next 12 months as JobKeeper and rent relief come to an end. Non-bank lenders are also offering support with SME resources and products.

The Australian Small Business and Family Enterprise Ombudsman, Kate Carnell, says access to finance in the year ahead could mean the difference between life and death for many small businesses.

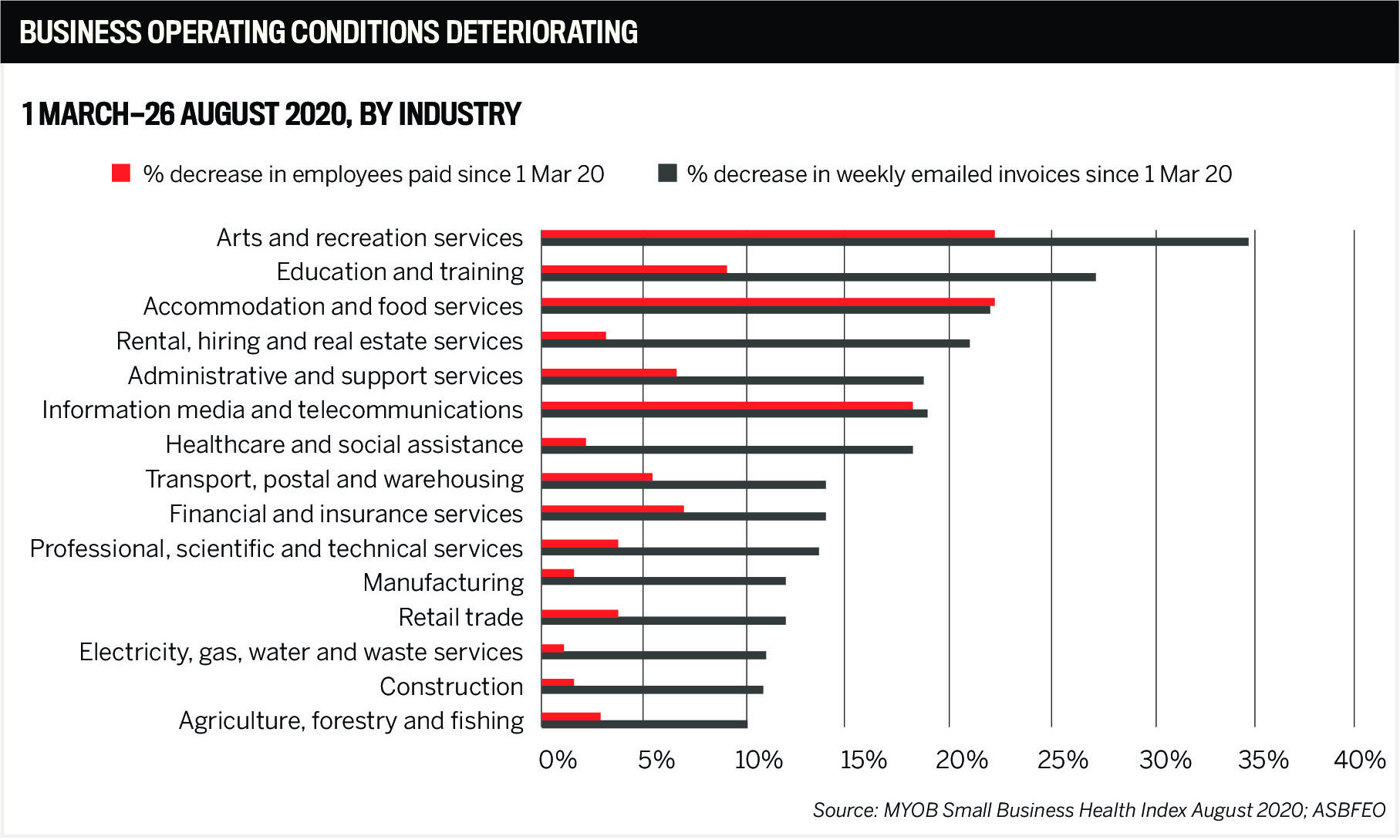

She says SMEs will have to deal with government support measures being withdrawn, rent relief ending, banks continuing their onerous credit assessment processes, and the effects of lockdowns and border closures.

“Unfortunately, it’s a perfect-storm scenario. especially for those small businesses that haven’t been able to fully recover from the COVID crisis,” says Carnell.

“Access to credit will be critical to keeping those otherwise-viable small businesses afloat, particularly over the coming months as support measures are phased out and the bills start flowing in again.”

Carnell is urging the federal government to fund a revenue-contingent loan program for small businesses (similar to HECS), requiring borrowers to repay the loan when their turnover reaches a designated level.

The loan would be capped at a percentage of the business’s annual revenue. Applicants would need to satisfy a viability test conducted by an accredited adviser to be eligible.

“Sudden lockdowns and border closures have heavily impacted small businesses in recent weeks. It’s no wonder they are scared to take on additional bank debt given conditions can deteriorate so rapidly,” Carnell says.

“The fallout of insufficient working capital could be devastating, not only for small business owners and their staff but for the broader economy.”

ASIC data shows external administrator appointments were up by 23% in December, and economists predict the number of businesses entering voluntary administration to rise this year.

Carnell says a revenue-contingent loan scheme would give small businesses the confidence they need to seek funding so they can survive and employ again.

“It’s essential to Australia’s economic recovery,” she says.

OnDeck CEO Cameron Poolman says the lender support measures are aimed at helping the small business community.

“It’s great to see the ombudsman considering initiatives that make it easier for SMEs to access capital,” Poolman says. “We would be interested in knowing more about how such a scheme would work.”

It’s OnDeck’s view that tailored financial support should remain for those industries heavily reliant on the international sector, such as tourism and education, which continue to be hard hit by the pandemic.

Prospa chief revenue officer Beau Bertoli agrees. He says government support such as JobKeeper was key at the height of the pandemic and has been tapered and managed effectively to help small businesses in need.

“Most of the leading indicators for the economic recovery are now trending positive. We saw GDP growth of 3.3%, businesses are paying bills faster, and economists are reporting the jobs market is looking good, indicating that extending JobKeeper further is no longer a requirement.

“That said, there are certain sectors that continue to be hit really hard, such as tourism and entertainment, and we support more targeted support for those businesses,” Bertoli says.

In the absence of further support, SMEs need to look at ways to adapt where possible, Poolman says.

“OnDeck’s free online COVID Resource Hub has plenty of real-life studies that show how businesses have pivoted into new revenue opportunities or different product lines during the pandemic or used technology to adapt.”

Poolman says OnDeck has taken a very proactive stance during the pandemic, reaching out to customers with practical support.

“When hard lockdowns were first announced in March 2020, we experienced a rise in the number of customers experiencing a cash flow squeeze. However, we maintained constant communication with these businesses and provided bespoke support to each enterprise.

“We are currently back to normal delinquency levels, and in the final quarter of 2020 we saw an increase of almost 90% in loan applications over the previous quarter.”

Bertoli says throughout 2020 Prospa offered relief packages to COVID-impacted customers, including partial and full deferrals, “working with our partners to provide the best support we could”.

“While there are still many small businesses doing it tough, we’re now seeing most small business customers recover faster and more strongly than anticipated,” he says.

“They’ve made it through a recession and likely the toughest trading conditions they’ll ever face, and with the economy rebounding, customers are starting to think about what’s next.”

Poolman says the ombudsman is accurate in saying that “banks are continuing to subject small business borrowers to onerous credit assessment processes”.

“OnDeck’s own research confirms that one in four SMEs get knocked back by the banks for commercial finance.

“Even among those that do get the green light for bank funding, 27% of SMEs have experienced negative impacts from a drawn-out application and approval process.

He says traditional banks are not the only source of finance available to SMEs.

“Small businesses can be reassured that dedicated lenders such as OnDeck are available that take a very different approach to SME finance.”

OnDeck offers short-term unsecured business loans ranging from $10,000 to $250,000.

“Our simple online loan application process, which requires six months of bank statements, is fast and efficient, and we can have funds to the business in as little as 24 hours,” Poolman says.

“Alternatively, SMEs can speak to their broker about an OnDeck loan.”

He says OnDeck also takes a forward-looking, data-driven approach to credit assessment using its proprietary credit-scoring methodology, OnDeck Score® – unlike banks, which make lending decisions based on past results.

Bertoli says whether small businesses need a line of credit to support cash flow or a loan to invest in growth, it can be difficult for them to access capital from banks and other traditional lenders.

“Historically it hasn’t been easy, and COVID has made it even harder. This is why raising awareness about alternative funding solutions is so important. Most small businesses don’t realise there are excellent alternatives to the banks,” he says.

“Prospa is 100% dedicated to small business, so we understand the pain points, the short-notice opportunities, and the need for both speed and service when it comes to customer experience. Our application process takes 10 minutes, and we can provide a response and funding in just 24 hours.”

Banks typically require asset security upfront, says Bertoli, but this often isn’t an option for small business owners.

“At Prospa, we don’t require asset security upfront to access up to $100,000, and that solves a massive obstacle for a lot of small business owners out there.”

Bertoli says Prospa’s line of credit is a great option, offering flexible access to funds.

“It’s a cash flow safety net, and you only pay interest on the funds you use, while you use them.”

What do Prospa and OnDeck think about calls for a nationally consistent approach to Australia’s border closures?

“The more certainty small businesses can get in this environment, the more confidence they will have to invest in themselves, new jobs and the economy,” Bertoli says.

“Different states have different risk appetites and strategies, but this makes it extremely difficult for small businesses to navigate and plan ahead.

“A national policy on hotspot definitions and responses would help boost confidence and empower more small businesses – especially those in tourism – to start investing and hiring for the future.”

Poolman says a nationally agreed approach to border closures would certainly support SMEs, especially in tourism-driven industries.

“That said, governments are all dealing with an evolving situation, which can change overnight.

“By acting on health advice, state governments are at least making rapid decisions. These decisions may not always seem to work in favour of small businesses, but as we have seen overseas, a slow response doesn’t just impact the economy and ultimately businesses, it can also cost lives.”