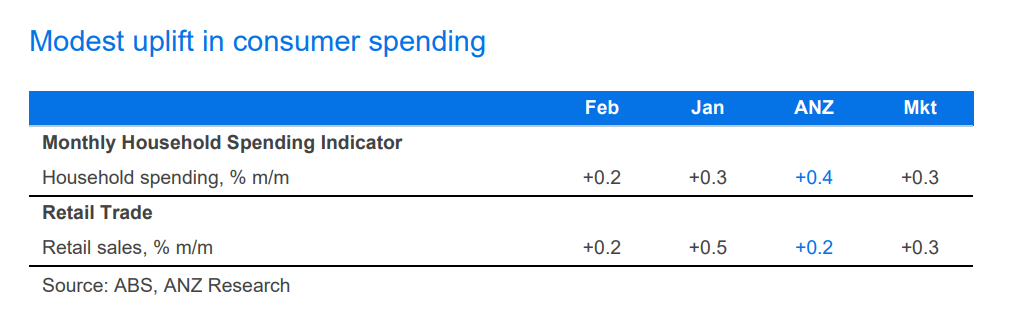

Household spending in Australia increased by 0.2% month-on-month (m/m) in February 2025, following an upwardly revised 0.5% m/m rise in January, marking the fifth consecutive month of growth, amid softening business conditions and declining consumer confidence ahead of the looming federal election.

The latest gains were driven primarily by discretionary spending, which rose 0.3% m/m, supported by a 0.9% m/m rise in recreation, a 0.6% increase in food, and a 0.5% lift in hospitality.

“The positive growth in discretionary spending in February, especially without any significant discounting events, is a welcome sign,” ANZ’s Aaron Luk and Adam Boyton (pictured left to right) said.

While discretionary categories saw growth, non-discretionary (essential) spending declined by 0.1% m/m, mainly due to a drop in health-related expenses.

This marks the first monthly decline in health spending since September, signaling a temporary shift in household priorities.

Goods consumption rose by 0.3% m/m, recovering from a 0.6% decline in January, suggesting renewed momentum in physical product purchases.

Services consumption was flat in February, though it remains elevated on an annual basis at +5.2% year-on-year (y/y), reflecting underlying strength in service-oriented industries.

At the state level, New South Wales and Tasmania posted the strongest growth in household spending, both rising 0.4% m/m in February.

This broad-based regional improvement supports the narrative of a steady national recovery in consumer demand.

Retail sales—a narrower measure of consumer activity—grew by a modest 0.2% m/m in February, following a 0.3% m/m increase in January. However, the result came in slightly below market expectations of a 0.3% m/m rise.

By category, department stores saw the largest monthly gain (+1.5%), followed by food retailing (+0.6%). In contrast, household goods spending fell for the second month in a row (-0.3%), after a strong performance in late 2024.

The “consumption data affirm that consumer spending is gradually recovering, as the RBA has been expecting,” the ANZ economists said.

The continued improvement in spending aligns with the Reserve Bank’s broader expectations, especially in light of the February rate cut, which is expected to further support household finances.

Looking ahead, analysts anticipate that additional RBA rate cuts in May, July, and August will help sustain consumer momentum—although global trade tensions could present risks.

“The rate cut in February will provide additional support to household finances,” the ANZ economists said.

“That said, increased global uncertainty around tariffs could impact domestic consumer confidence, although we now expect rate cuts from the RBA in May, July and August, which should help offset that.”

The Australian Bureau of Statistics (ABS) has confirmed that the Monthly Household Spending Indicator will replace the Retail Trade series as its primary consumer spending measure when the latter ceases publication in July.

“We have previously discussed the key difference between the two series,” the ANZ economists said.

This transition reflects ABS’s broader move toward timelier and more comprehensive consumer data reporting.