Mortgage applications rose 5.2% in Q1 2025 compared to the same period in 2024, driven by a surge in refinancing activity after the Reserve Bank’s February rate cut, which renewed borrower confidence and triggered a wave of repricing.

Refinancing accounted for 37% of all mortgage demand in March, with many borrowers anticipating further interest rate cuts—expectations reinforced by forecasts from all four major banks that the Reserve Bank could ease policy again, potentially as early as its May 19-20 meeting.

“The comeback in mortgage demand looks likely to continue, with refinancing accounting for 37% of mortgage demand in March,” said Kevin James (pictured), chief solution officer at Equifax. “Given the process of refinancing can take time, there will be a cohort of consumers who are planning to change their mortgage provider in the coming months.”

While demand surges, repayment stress is intensifying—particularly among borrowers with large loans. The report revealed a +9.2% rise in the total dollar value of 90+ day mortgage arrears, with home loans over $1 million now showing higher arrears rates than any other loan size segment.

“This tells us that people with larger loans are struggling to keep up with payments and falling further behind,” James said. “In fact, for the first time on record, mortgage loans exceeding $1 million are displaying higher arrears rates compared to all other loan size segments.”

Investor refinancing accounted for nearly 80% of total refinance activity in March, more than double the rate of owner-occupiers. This strong investor activity indicates a belief that rate cuts are likely to continue, offering future borrowing advantages.

A significant share of refinancing also originated from loans established during the low-rate periods of 2020–2021, or previously refinanced during the peaks of 2022–2023. This trend suggests borrowers are looking to optimise terms or access home equity after several years of repayments.

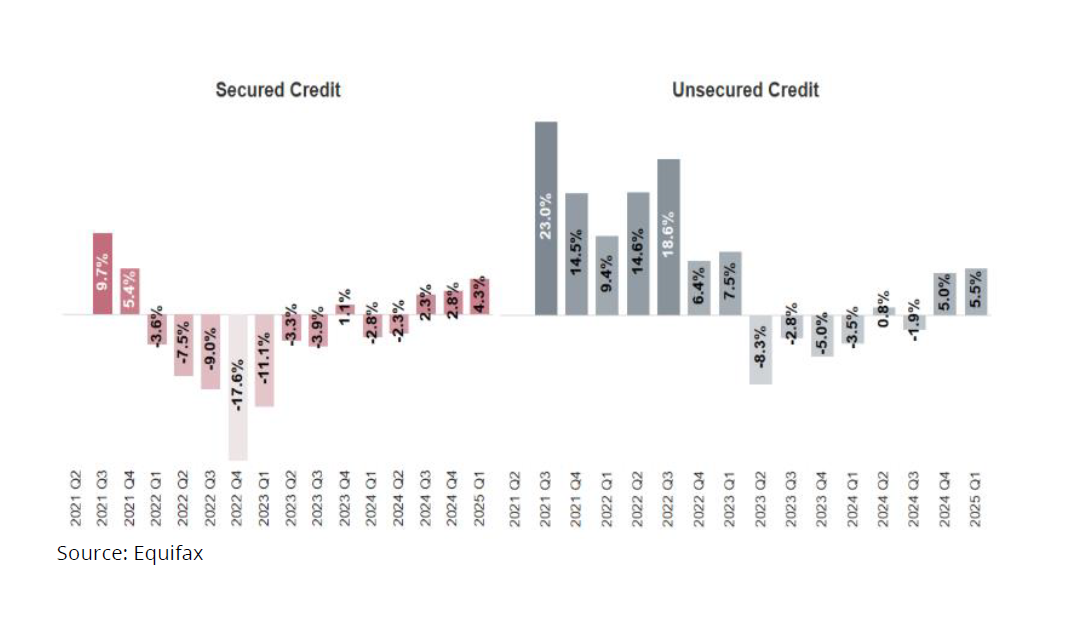

Equifax’s data also highlighted a +5.5% year-on-year rise in unsecured consumer credit demand during Q1 2025, led by:

Secured credit applications also rose 4.3% year-on-year, with mortgage (+5.2%) and auto loan (+0.3%) activity both increasing.

Delinquency rates climbed across all credit types, signalling repayment pressures after seasonal spending. Equifax data shows 90+ day past due balances increased for:

“The increase in the outstanding amounts owed by consumers suggests that holiday spending has caught up with people who may have used credit to live beyond their means over the festive season,” James said.

“Specifically, in Q1 2025, Equifax saw the average amount owed per delinquent credit card increase to $7,100 – a marked difference from $6,900 at the same time last year. This further highlights that consumers are struggling to pay off their debts.”