A national housing price crash remains unlikely, but the risk of a deeply uneven correction is rising. That is the assessment of Ray White chief economist Nerida Conisbee (pictured), who argues that Australia's housing shortage, population growth, and constrained construction pipeline will prevent a broad-based collapse — but will not protect every segment equally.

The more pressing concern, Conisbee argues in a LinkedIn post, is that "the downturn is likely to be concentrated in the parts of the market where demand was most policy-supported and where buyers have the smallest equity buffers."

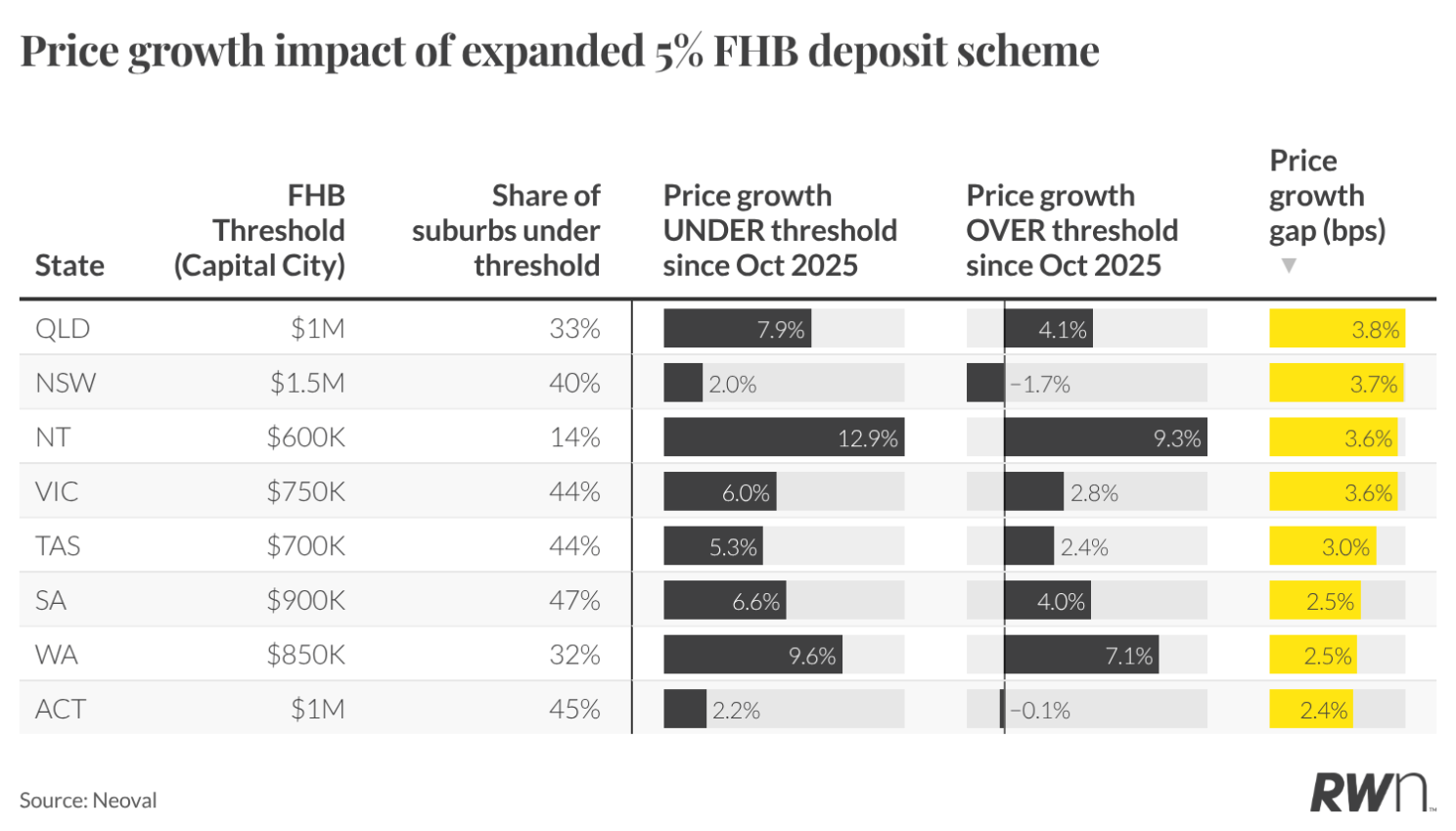

When the federal government removed income caps, lifted property price caps, and made scheme places uncapped from 1 October 2025, demand flooded into cheaper suburbs. The effect on prices was measurable and concentrated.

In NSW, suburbs below the first-home buyer price threshold rose 2% while above-threshold suburbs fell 1.7%. Victoria's under-threshold market rose 6% against 2.8% above, and Queensland's gap was wider still — 7.9% below the threshold against 4.1% above.

That outperformance was not organic. As Conisbee puts it, "first-home buyer markets were not outperforming by accident. They had direct policy support."

Now that same policy architecture is shifting — with budget changes designed to reduce investor activity targeting precisely the cheaper end of the market where first-home buyers and investors overlap. The scale of the investor retreat is already visible in lending data — Westpac reported investor loan applications fell 20% in the weeks following the May budget, with the bank flagging further weakness ahead.

Clients who entered the market through the 5% deposit scheme are now sitting on minimal equity — and the incentive-driven suburbs where they bought are the same ones most exposed to the investor pullback. Even a modest price correction in those markets could move some into negative equity — not necessarily a crisis for borrowers who can service the loan and have no need to sell, but a material risk for those whose circumstances change.

The broader mortgage stress picture adds weight to that concern — Roy Morgan data shows approximately 1,552,000 mortgage holders are now at risk of mortgage stress, with those classified as extremely at risk sitting at 20.4% — well above the long-run average of 16.4%.

Conisbee is direct about the structural dynamic at play: "the lower-priced markets that were pushed up by first-home buyer incentives are now the same markets most exposed to the investor pullback."

With clearance rates softening, confidence weakening, and the federal budget adding further uncertainty, brokers with first-home buyer clients concentrated in sub-threshold suburbs should be monitoring this segment closely.

Get the hottest and freshest property and mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.